Publicité

Chairman of the MIC - An Open Letter to Lord Meghnad Desai: About LUX* Island Resorts convertible bond

Par

Partager cet article

Chairman of the MIC - An Open Letter to Lord Meghnad Desai: About LUX* Island Resorts convertible bond

Dear Lord Desai,

As a citizen of Mauritius, I am writing to you in an open forum because I have no other means of contacting you and secondly because I do believe that the Mauritius Investment Corporation (MIC), with an expected assets under management of MUR 80 Billion, merits a certain degree of transparency, a minimum level of relevant expertise and accountability to the people of Mauritius.

In addition, I do believe that constructive criticism and feedback should be discussed more openly and dispassionately in the public domain, given the strategic importance of the MIC for the economic recovery of Mauritius. The MIC was also set up to transfer wealth to future generations of Mauritians.

I am sure you share the same views that distressed investing, the pricing and structuring of convertible bonds are very specialized sectors within the equity capital markets.

I also invite you to share this letter with investment banking, convertible arbitrage, focused hedge fund managers and capital markets specialists based in London, which is still the center of excellence for convertible bond origination, sales and trading. Many of the most sophisticated convertible bond investors are still based in London despite Brexit. I am quite confident that my logic and the math behind it will be in line with these convertibles bond specialists’ views.

As a preamble, I am not a politician and I have no skin in the game. My letter has nothing to do with being pro or anti-government. Very often in Mauritius, this thinking is used to dismiss arguments outright. I am writing to you as a concerned citizen and professional in my individual capacity and as a former investment manager and senior officer of the BoM international reserves management team. I have a lot of respect for the people who work at the Bank of Mauritius, a respected official institution made up of many brilliant professionals when given the chance to shine.

However, I also know that distressed, special situation investing and convertible bond pricing is not their area of expertise. This is not the area of expertise found in any central bank.

While my letter will focus on my concerns about how LUX* Island Resorts convertible bond issue was priced based on the public communiqué, I have nothing against the issuer. In fact, I think that the company is perhaps one of the most well managed in Mauritius. We should not allow a liquidity problem to turn into a solvency crisis for these large companies which employ thousands in the country.

However, the last Great Financial Crisis bailouts and unconventional monetary policies which were implemented in response in the advanced economies, taught us that striking the right balance between supporting systematically important companies and supporting struggling citizens is critically important.

If the citizens who own the central bank are to bail out struggling and large companies, they need to get a fair deal in terms of an appropriate level of risk adjusted return as compensation which hopefully in the long term can be distributed back to the state as dividends.

The MIC itself is too big to fail and the coming decade will be very difficult for Mauritius. Policy makers cannot afford to make many mistakes anymore and nor will the current populist movement forgive policy makers for making such mistakes.

Convertible bonds are hybrid instruments which have bond and equity characteristics and can be broken down into two main components, a plain vanilla bond with a low coupon and an embedded option which allows the bond holder to convert the bond into equity any time during the life of the instrument.

The coupon rate is typically set at below the cost of debt of the company which is why it considers it in the first place but in compensation for the risk, the investor gets an option on the equity of the firm subject to some call provisions.

The embedded option to convert the bond into common stock has value and is a key component of the convertible bond valuation. Some convertibles specialists even measure the richness and cheapness of the bond by using the implied volatility of the conversion option. Some equity focused investors also buy the convertible and strip out the bond part. The value of the option matters!

Given the “rapport de force”, which the investor has over the bond issuer, it is standard for this option to be exercisable at any time from the time the bond is issued. It is called an American-style conversion option. Of course an investor will only exercise the conversion right if the option is in the money, that is if the price of the common stock has gone above a pre-determined conversion price which in the case of LUX* is the average price of the stock between January and June 2020 (average VWAP of MUR 35 vs current price of MUR 26.20 or a significant discount to strike price).

It is however much more common that the conversion price or strike price be set at around issue date with the reference price set as the VWAP of the past 1-2 days.

In the case of Lux, a public company listed on the SEM, the conversion price was set during a period of six months and more than 3 months prior to the planned issue date – this feature deviates from global best practice and disproportionately favours the issuer rather than the investor, the MIC. The conversion price would have been lower and LUX* would have to issue more shares, if the bonds were converted based on common market terms. This in itself has a large impact on the option value.

This ability to convert at any time until maturity which is standard in markets globally is also known as an American-style conversion option. In the case of the LUX* deal, the MIC will only be able to exercise this option at maturity after 9 years, i.e this is a European-style option, which is atypical for this structure and very disadvantageous to the MIC which begs the question, why European style vs American style?

On the other hand, the issuer will be allowed to exercise its right to buy back part of or the entire issue at any time after issuance, which is also atypical for such a deal, even more so given the context where the negotiating power should rest with the MIC.

Convertible bonds are almost always callable by the issuer only after a certain period e.g 3 years for 5 years maturity or even 5 years for longer dated structures. The investors have some protection during that period. In addition, the bonds usually have a soft call provisions as well, which is triggered if the share price is trading above 125- 130% of the conversion price. This feature will force the bond holders to convert into equity during that period.

The issuer of the bond will only exercise its right to call back the bond when the price of the stock has rallied above the strike (when MIC will start to make decent returns) especially when it is less dilutive and cheaper for the issuer to do so. In addition, the issuer could also call the bonds at PAR if rates fall further. This is a great deal for LUX* but a terrible deal for the MIC.

The current Hard Call feature of LUX* (anytime after issuance) erodes the equity sensitivity of the convertible bond. The Hard Call provision has a lot of value for the issuer, not the MIC and I would like to know if the MIC is being compensated for that?

As I will attempt to showcase soon, the MIC is paying MUR 1 Billion for convertible bonds which are not really convertible bonds given the worthless out-of-the-money and mispriced European style conversion option. The MIC is paying 1 Billion for a bond worth significantly less than this. There is nothing “quasi equity like” about this issue which ends up as a cheap plain vanilla low-ranked bond because the structuring is all wrong.

To determine the value of a convertible bond, the plain vanilla bond component is quite straight forward to value. While the coupon rate of the deal is not yet public, we can safely assume that it stands at between 3% and 5% as it would defeat the purpose of offering liquidity support and cheaper debt otherwise.

We for example know what the conversion price is vs. the current stock price which makes the embedded European equity option “masked” by the Hard Call provision of the bond. Based on simulations, it appears that the European option held by the MIC would have a near zero likelihood of being exercised, which explains its value, because of its high-time value (9 years) while the Hard Call of issuer is exercisable anytime after issue (zero time value)

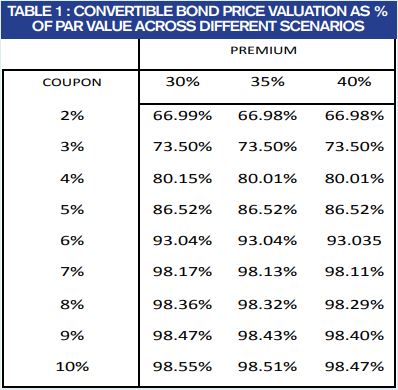

I have modelled the LUX* convertible in a very simple Black Scholes pricer – The inputs are: the maturity, Hard Call provisions of the issuer, flat volatility of LUX* stock, a range of estimates of the credit spread of LUX*, yield curve of Mauritius, future dividend streams, and the stock borrow – the cost MIC will forgo from disinvesting from the FX reserves which is a proxy. There are more advanced multi-factor models which use the volatility surface of the stocks, and the parametric model of yield curve and credit spreads. The table clearly showcases that the bond is intrinsically worth much less than PAR (price paid)! (See table 1)

While many assumptions may be tricky requiring scenario analysis which is why I showcase a range of pricing in the table below, it is very clear that the Conversion option is not worth anything because of the value of Hard Call structure.

Even giving more benefit of the doubt to the MIC deal makers won’t help them much in terms of the assumptions because of the Hard Call feature. In order to have a price that is at par in fact, holding the terms constant, you would need a coupon in excess of high single digits which would defeat the purpose of helping out the company and again this would not be a convertible bond but a subordinated bond having a floating charge ranked after all other charges which means what it means.

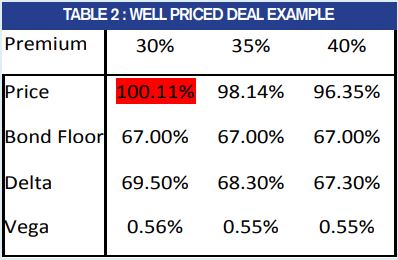

The deal is now done and dusted and the company should be supported. However, the deal should have been structured by extending the Hard Call protection (to benefit the investor) from zero to 4 years. Then after 4 years, a Soft C all with a 130% trigger should have been included. The coupon could be kept below 4% without sacrificing the long term return potential.

Finally the conversion period should have started from day 1 until maturity (No European but American style). These features would have made the convertible bond more equity-like vs bond-like, and it would be in line with the current mandate of the MIC. Let me be clear, the MIC and the BoM are taking on a lot more risks with capped upside returns in this deal and in other deals to come if it is not careful. (See table 2)

What needs fixing with the MIC? Obviously the governance structure needs to be reviewed. Ideally the MIC should have been created as an off balance sheet bankruptcy remote special purpose vehicle rather than being on the balance sheet of the regulator. The BoM should have financed the SPV with debt issuance while the government would have been an equity investor in the MIC. The leverage would have allowed the MIC to optimize its own capital structure and be in a better position to not only partner with firms it will support but to optimize returns to the citizens of the country as well. Holding such instruments directly on the balance sheet of a central bank especially when dealing with distressed/special situations will be complicated and may require the bifurcation of the bond under IFRS9.

Some leeway in pricing per deal can be negotiated based on other factors such as protecting jobs but not like this. The MIC should hire investment professionals with relevant experience in distressed investing, special situations investing and who have experience in pricing and dealing with convertible bonds or appoint a global fund manager with relevant experience and track record.

In the scenario of internal hires, the MIC Board should appoint external advisers who will not only act as a check and balance but also help the MIC in conducting the pre deal on-site and offsite due diligence, the negotiation and also in properly pricing these securities on a deal by deal basis. We should also be careful about conflicts of interest. This field has little to do with central banking or corporate banking and the hiring should reflect this reality. As can be seen with just one deal which rings like the mother of all deals for the issuer, being penny-wise on costs can be quite pound-foolish in the end. With another Rs 79 Billion to go, it can be disastrous for the BoM and the country. I am convinced that this was not what the government, the Governor and you intended and wish to see happen. As a reputable person and independent chairman, I implore you to ensure that MIC succeeds in its mission.

Bio

<p>Sameer Sharma holds an MSc in financial engineering from the University of Quebec in Montreal, is a Chartered Alternative Investment Analyst and a Certified Financial Risk Manager with more than 14 years of quantitative analysis, multi asset investing and AI modeling experience. He is a former central banker, international reserves portfolio manager and is currently based in the United States where he is a senior AI consultant within the financial services sector.</p>

Publicité

Publicité

Les plus récents