Publicité

Oil windfall gains: a shot in the arm for the economy

30 septembre 2015, 10:56

Par

Partager cet article

Oil windfall gains: a shot in the arm for the economy

Former Finance minister Rama Sithanen sheds light on the debate on the price of petroleum products. He believes that a timely policy change could create a much needed confidenceboosting climate that would stimulate GDP, employment and investment and lower inflation.

This article has three main objectives (i) First, to explain the huge disconnect between crude oil prices on the one hand and pump and electricity prices on the other. The price of crude oil has fallen nearly 60 % from its peak in August 2014. Yet this sharp decline is not mirrored in gasoline, diesel and electricity prices. Many argue that gasoline, diesel and electricity prices are being kept artificially higher for the benefit of Government, the STC and the Central Electricity Board (CEB) at the expense of the economy and the population. Hence the numerous calls for a decrease in their prices ;

(ii) Second, to propose that we seize this unique opportunity to have a targeted and timely policy change that would lead to a significant and substantial decrease in fuel and energy prices with a view to crea- ting a much needed confidence-boosting climate that would stimulate the economy and lower inflation ;

(iii) Third, to describe how this recommended change in policy would send the right signal and produce a virtuous cycle where the economy, consumers, producers, exporters and government all gain from lower fuel and electricity prices. It could contribute to greater purchasing power, rising investment, higher Gross Domestic Product (GDP) growth, more employment, lower inflation, and even enhanced tax revenues for Government.

I shall focus on gasoline prices by way of analysis and illustration even if the same principles and practice apply to diesel, albeit in a different proportion as the fiscal burden is less cumbersome. The case of electricity is much simpler as the transmission mechanism is straightforward and not hamstrung by many taxes. It is simply a policy choice on how to distribute the windfall gains of the lower costs of fuel oil and coal between the CEB and its end users. Currently the massive dividends are accruing to the CEB only.

Instead of the conventional narrow, micro economic and static approach that usually pits Government, State Trading Corporation (STC) and CEB against the population in a zero sum game where the gains of one are perceived as the losses of others, I am advocating a broad, macroeconomic, dynamic and out-of-the box perspective that considers the forest of the entire economy as opposed to the tree of a specific “us against them” decision.

The simple question is who should benefit from the windfall gains of crude oil prices that have crashed around 60% over the last twelve months and coal prices that have more than halved over four years, hit by a perfect storm of oversupply and waning demand.

Should it be Government, the STC and the CEB or households, firms, the entire population and the national economy or a combination of the two groups and in what proportion? More critically, how much of the oil and coal price windfall gains should government save if national output is below potential, growth is anaemic and inflation is low? Context and circumstances matter significantly in the decision of how to allocate the windfall gains.

We import 100% of our transportation fuel and close to 80% of other energy and as result the external position is improving with positive terms of trade effects. I submit that because Mauritius has a negative output gap, is experiencing lacklustre growth and declining inflation, the government, CEB and STC should not take the overwhelming share of the windfall gains.

Instead they should ensure a high degree of pass-through into retail prices to consumers and producers so that demand is stimulated by the full amount of the oil and coal dividend. If the sharp decline in global prices were to fully pass through to domestic end-users, GDP, employment and investment would rise. For instance, falling oil prices are in part responsible for the recent resurgence of economic growth, high job creation and the rise of manufactured exports in the U.S.

The proposed partial responses

There have been two PNQ’s in a row on the prices of mogas, diesel and electricity. Government has responded by stating that it will review the formulabased pricing that determines the pump costs of mogas and diesel and will consider a reduction of electricity tariff for the vulnerable groups. If we assume there is a correlation between income groups and electricity consumption, there is already a differential pricing structure that protects consumers with low residential electricity use. Of course more can be done for the low income groups but we need to create a deeper and wider impact with significant catalytic ramifications.

True it is that the prices of mogas and diesel could be impacted, as has been done in the past, by tweaking the formula used to determine fuel prices, even if it could be a double-edged weapon. For instance, one could revise the band within which there are no price changes (currently at 4 % on either side with a ceiling/floor of 10%), review the volume factor retained in the calculus (difference between notional monthly quantity and actual amount carried by one or two vessels), alter the exchange rate used (between an estimated one and the actual one paid by the STC 60 days from the bill of lading ), revisit the basis of the reference price (monthly figure or six monthly average of Platts), relook at the periodicity of the price-fixing exercise (monthly or quarterly) and reconsider the use of the price stabilisation account.

These could bring some limited relief to consumers but it may come to haunt them later. Also these changes would not be significant as to positively impact key macroeconomic indicators.

Why have gasoline and electricity prices not fallen?

The simple answer is that the transmission mechanism for mogas is hamstrung by a combination of exchange rate and taxation policies. And in the case of electricity, there is a policy decision for the CEB not to share the windfall gains with its end users.

Barring the formula-driven adjustments referred to above, there are seven major reasons for a disconnect between the cost of crude oil and the prices of gasoline, diesel and electricity.

First, the prices of crude oil and refined products are set in different international markets that are governed by their own laws of supply and demand. As this is a highly technical subject, I shall assume that we have little control on this variable. I equally surmise that we are reasonably good at sourcing refined products at best prices and that the freight, insurance and premiums paid to suppliers are competitive.

I therefore take as given the cost, in- surance and freight (CIF) value of one litre of mogas and diesel as published by the STC. If these could be improved, so much the better for our country.

Second, the costs of refined products are denominated in U.S. dollars whereas the prices of mogas, diesel and electricity are expressed in rupees. Exchange rate fluctuations have an impact on the final prices paid by the population. The rupee has depreciated against the dollar between the two latest reference dates used by the STC. On December 5th, 2014 when prices were changed, the US$ exchanged at Rs 31.80 while on September 4th, 2015 when the price of only diesel was brought down, the STC assigned a value of Rs 35.25 to the greenback. It represents a depreciation of more than 10% of the rupee and works against a fall in product prices.

Third, the prices of gasoline and diesel at the pump include various taxes (less so for fuel oil used by the CEB). They can be high in countries such as France, Germany and the United Kingdom and lower in the United States. Very few motorists have a good idea of how much taxes they pay when they pull up to the pump. For instance the UK has one of lowest petrol prices in Europe before tax but among the highest after all taxes are added. Mauritius levies various taxes on petroleum products and their total can represent a high share of the prices;

Fourth, the basis on which taxes are levied can also determine the level of stickiness in the prices of petroleum products. Many of the fuel taxes are specific duties or fixed contributions and are not influenced by oil price fluctuations. If taxes are advalorem (based on the value of the product as Value-added tax - VAT), the pass through will be better from crude to pump. However it works both for a rise and a fall in prices.

Fifth, there is an element of double taxation embedded in the price structure of mogas and diesel. Essentially it is a tax on a tax. Initially there are many taxes and contributions that are levied on these products; then VAT applies not only on the CIF value of the products but also on the taxes already charged.

Sixth, Government has increased taxation on mogas and diesel to prevent a fall in retail prices. The contribution to Build Mauritius Fund was raised by 300% from Rs 1 to Rs 4 per litre in January 2015 to thwart a pass through to end users.

Seventh, in the case of the CEB, it is a simple policy decision not to share the windfall gains with its end users. This is reflected in the significantly improved financial performance of the utility company. Of course one could argue that the CEB has absorbed cost increases in the past without passthrough and has to invest to ensure future power security. However this is an altogether different debate.

Can the price of mogas fall by at least Rs 10 per litre? A contingent yes!

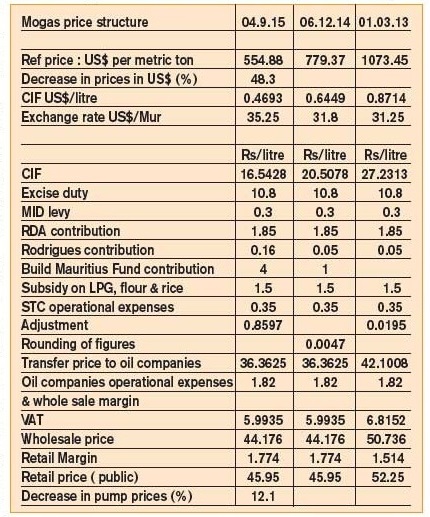

To show how this is feasible, I shall consider the price structure of mogas as given by the STC for three reference periods: March 1st 2013, December 6th 2014 and September 4th 2015. The following is clear from the price structure

(i) There are seven taxes/contributions levied on gasoline. These are excise duty, MID levy, VAT, contribu- tion for Rodrigues, Road Development Authority, Build Mauritius Fund and subsidy on LPG, rice and flour;

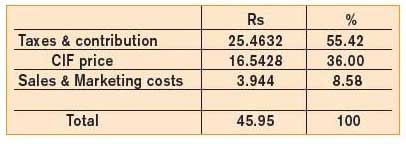

(ii) There are three major cost components in the price structure: the CIF value, taxes/ contributions and marketing, sales and distribution expenses. The share of each component in the current price is as follows:

(iii) Taxes/contributions stand at 154% of the CIF of the product. They also account for more than half of the price of a litre of mogas. The seven taxes represent 55% of the pump price as from September 4th 2015 while CIF contributes to 36%; sales, and marketing expenses are at 9 % of the price.

(iv) In view of the nature of the taxes levied, the share of taxes rises as the CIF decreases and falls as it increases. In a declining market, this basis of taxation hinders the functioning of the transmission mechanism from CIF value to retail prices;

(v) Six out of the seven taxes/ contributions are insensitive to the change in the CIF value of mogas. The excise duty is constant at Rs 10.8 per litre irrespective of whether the CIF value is Rs 27.23, Rs 20.50 or Rs 16.54 per litre. This method of taxing energy products penalises consumers in a period of falling prices. VAT which is an advalorem tax varies directly with the pro- duct cost at the rate of 15%;

(vi) Since CIF represents only 36% of the final price and many taxes/contributions are specific, it is plain that a 50 % slump in the cost of refined product will produce a much smaller decline in pump prices. And if one takes into account the depreciation of the rupee, it is clear why a 48.3% drop in the US$ CIF value of mogas between March 2013 and September 2015 led to a fall of only 12.1% in retail price;

(vii) It should be pointed out that VAT is applied not only to the cost of the refined product and other expenses but also to the other taxes.

It is a tax on another tax. For instance the excise duty of Rs 10.80 per litre also attracts a 15% VAT. The effect is a rise of Rs 12.42 in the final litre price instead of Rs 10.80 only. Equally the newly higher contribution of Rs 4 per litre to the Build Mauritius Fund increases the final price by Rs 4.60 as there is VAT of 15% on the tax. It is abundantly clear that simply tinkering with the mathematical formula that drives the prices of energy will not materially affect the prices of mogas and diesel. It will also not create the impact necessary to generate a virtuous cycle of confidence building, greater disposable income, rising investment, higher growth, more employment and lower inflation.

Besides a stable exchange rate policy, there are five avenues to reach a balanced outcome between the interests of motorists and end users of electricity and those of Government, the STC and the CEB. Especially in a very challenging context when private and public sector investments are falling as a share of GDP, exports are facing huge challenges and Government has no fiscal space to pump prime the economy. The right policy mix could unlock incremental economic growth by boosting consumption and output and make production more efficient.

i) The excise duty on mogas used to be an advalorem tax similar to VAT. However as the costs of refined products went up, it was deemed unfair to maintain a proportionate levy as it doubly penalised users. The tax would rise whenever the cost of the product went up. To protect consumers, the advalorem tax was transformed into a specific tax of Rs 10.8 per litre. This worked well in a period of rising prices but is detrimental to end users when prices decline.

Using March 2013 as a base, the specific tax of Rs 10.8 on a CIF of Rs 27.2313 is the equivalent of an advalorem levy of around 40%. If we applied the same percentage tax to the September 2015 price of Rs 16.5428, the excise duty would be Rs 6.56 per litre instead of Rs 10.8 with a specific tax. This alone represents a difference of around Rs 4.25 per litre of mogas ;

ii) In the current context, one could consider not levying a tax on an existing tax. There are seven taxes imposed on the price of gasoline. Six are specific taxes while the VAT is an advalorem duty. The build up in the price computation is such that VAT is charged on the other six taxes too. This constitutes an additional tax of around Rs 2.75 per litre ;

iii) there is a case to review the recent massive increase in contribution from Rs 1 to Rs 4 per litre to the Build Mauritius Fund. This was sim- ply an additional tax of Rs 3 per litre levied to prevent retail prices from fal- ling. If it went back to its former level, there would be an additional saving of Rs 3 per litre;

iv) there is a case for rationalising the six taxes, other than VAT, as many of them serve the same purpose of raising revenue to allow Government to finance some expenditures. For instance, should the subsidy on cooking gas, rice and flour stay at Rs 1.50 when the prices of these commodities are falling? Is there not a case to simplify all these taxes into two taxes only? Especially as money is fungible;

v) the CEB could be called upon to share some of the windfall gains in the prices of fuel oil and coal with its customers.

If one were to convert the current specific excise duty into an advalorem one, avoid imposing VAT on existing taxes, rationalise the six taxes other than VAT, restore the Build Mauritius tax to its former rate and tweak the existing mathematical formula, there would be a decline in mogas prices at the pump of at least Rs 10 per litre, if not more. This pass-through would be substantial and would act as a powerful lever to stimulate the economy.

The price of diesel would come down by a lower amount than Rs 10 per litre for at least two main reasons. First it has already dropped by 20 % compared to a decrease of 12 % only for mogas since March 2013. Second the excise duty is lower at Rs 3 per litre compared to Rs 10.8 per litre for mogas. Both make it more difficult to have as substantial a price fall as in the case of mogas. Based on the same principle as for mogas, it could drop by around Rs 6 per litre.

The case of electricity is easier as there are not many taxes. It is a simple pass-through where the windfall gains of CEB are shared with energy users in a fair manner. A policy decision is required for the CEB to distribute some of the oil and coal dividends with its industrial, commercial and residential customers.

The exact amount depends on many factors including its future investment requirements. However given the size and significance of the oil and coal deflation enjoyed by the CEB, it should not be hard to decrease electricity prices across the board by a double digit percentage.

The virtuous cycle of higher GDP growth, more employment and lower inflation

With continued excess supply, subdued demand and the strategy of oil-producing countries not to cut output, the costs of petroleum pro- ducts are likely to remain low for the foreseeable future. At the same time, three cylinders of our growth equation – investment, government expenditures and exports – are showing sign of weaknesses.

We must boost consumption by putting more money into the pockets of the population and support economic activities by lowering the cost of fuel and energy. Some may argue that this would represent a shortfall in tax receipts.

However a dynamic and comprehensive analysis of the potential eco- nomic impact of a major fall in the prices of fuel and electricity would point to a different outcome. It could work exactly as in the case of lower taxes. New opportunities are unlocked that deliver a win-win scenario for all stakeholders. Besides motorists and all end users of power, another great beneficiary would be the economy with enhanced spending, rising investment, greater output, higher growth and more employment.

There are broadly speaking four engines of growth in an economy and three are currently faring poorly. Investment as a share of GDP is at its lowest historical level, exports are facing significant headwinds while the rising budget deficit and the mounting public debt prevent government from fiscally stimulating the economy. In that context, consumption and some output increase due to higher spending power and lower input costs could play a catalytic role to support activity and act as an “automatic stabiliser”

Tumbling oil prices have been one of the most important macro-econo- mic events recently. Well utilised and smartly managed, it can be positive for Mauritius as we are a net oil and energy importing country. Transfering the significant fall in oil and coal prices to the economy in terms of lower fuel and electricity prices would have a largely beneficial impact on the economy.

In a stylised version, the main effects would be felt as follows:

(i) On the supply side, lower oil prices lead to a decline in the cost of production of final goods and services, especially in sectors that are fuel or energy intensive. The lower input costs will boost production, expand output and enhance overall economic activity at a time when it is much needed ;

(ii) On the demand side, reducing fuel and energy bills will inject more disposable income in the hands of the population. It will provide a positive shock, bolster consumer spending and boost the economy. Consumers would spend more on almost everything from food to clothing to other goods and services;

(iii) Such declining prices will dampen inflation both directly when the prices of oil-related products fall and indirectly when production costs for other goods decline;

(iv) The increased productivity and profitability among operators that benefit from the fall in prices of these three products will increase demand for labour and capital;

(v) As a result of stimulative economic activites, GDP will grow faster and employment will rise. The lower input costs will induce employment creation by firms;

(vi) Lower fuel and energy prices will generate additional investment and spending in some specific sectors as the cost of doing business decreases ;

(vii) Government revenue would increase as proceeds from corporate, personal, VAT and other taxes rises with higher activities. There would also be the indirect,induced and spill over effects.

Other countries are using this dividend to compensate the deficiency in the other drivers of growth. The US is clearly benefitting from higher growth and exports, more employment and lower inflation.

The impact of such shocks on the economy are analysed through both the production and consumption channels. Estimates of the windfall effects of oil prices show countries like Singapore, Taiwan, Thailand, South Korea, and Hong Kong will profit substantially in terms of incremental GDP growth of 1.5% to 2% over a two year period.

A recent report found that a 10% decline in oil prices could push up GDP growth by 0.3% in India while another one concluded that a 20% drop in oil prices will increase GDP growth by 0.5% in China. The slump in oil prices has been higher than 50%. Further, that initial boost could be amplified if it led to a subsequent lift in confidence, encouraging companies to invest and spend. The big winners are countries that are simultaneously heavy users of energy and largely dependent on oil imports. Mauritius relies greatly on imported energy products and is not as fuel and energy efficient as advanced economies. So the gains could be significant.

It also spurs job creation in sectors such as construction, chemicals, paints, manufacturing, airlines, cruise ship operators, retail, whole- sale, leisure, hospitality and transportation companies. There is also a psychological effect as lower fuel and energy prices could boost consumer sentiment so that they feel more optimistic than the extra cash in their wallet seems to suggest. Lower fuel and electricity prices also act as a check on inflation, thus creating more scope and space for monetary easing that allows central banks to lift economic growth. This space has already been used by India, China and South Korea which have lowered interest rates to boost activity

Concluding note

Global oil prices have plunged over the last 12 months. It is a significant macroeconomic event in terms of its sizeable decline and have reached levels not seen in several years. Most analysts believe that oil prices will remain low for longer as oversupply and subdued demand will continue in 2016.

It offers a unique opportunity as it provides much-needed breathing space for Mauritius to use these windfall gains to stimulate the economy, especially at this critical juncture when investment is declining and employment creation is a challenge.

When lower oil prices are passed on to end-users, their effects filter through the entire economy with production costs declining and disposable income rising with knock on effects on output and consumption.

It translates into spending power, investment, higher output, employment and tax revenue and lower inflation. It is the equivalent of a tax cut or a bonus for households, a raise in wages for employees and a reduction in costs for economic operators.

In brief, passing on the sharp and sustained oil price deflation could be a blessing for the Mauritian economy as consumers, businesses, producers, exporters and Government all win in a virtuous cycle.

It could be a transformational event and, if well supported by other policies, it has the potential to rekindle the engine of growth. At a time when the economy is flagging and needs a shot in the arm, this could be a silver bullet, a welcome tailwind and a boon for the country.

Publicité

Publicité

Les plus récents

Égalité des genres

«Pena tansion» et «koz manti» : La ministre et sa junior s’affrontent

«Finance Bill»

Haniff Peerun demande au président de bloquer le texte de loi

Natation – 13ᵉ Jeux de la CJSOI – Épreuves du 4 au 7 août - 1ᵉ journée

Maurice débute avec 4 médailles : 1 d’argent et 3 de bronze

Opération coup de poing de la FCC

Voitures de luxe, motos et drogue saisies

Première édition de «Sport Contre la Drogue»

Djahmel Félicité redonne vie à son quartier à Saint-Pierre