Publicité

The 2018/19 Budget: More social largesse

Par

Partager cet article

The 2018/19 Budget: More social largesse

The policies of the 2018/19 budget focus more on extending social largesse, and less on rectifying the economy’s structural imbalances, says Sushil Khushiram.

Fiscal operations comprise revenues and expenditures of the Government Budget as well as of special funds. Off-budget transactions of special funds are therefore consolidated with the Budget. The Build Mauritius Fund has been closed and an amount of Rs4.8 bn transferred to the budget as revenue. Two other funds, namely the National Resilience Fund and a new National Environment Fund still exist, along with a Lotto Fund, incurring expenditures and making transfers which need to be integrated with the budget.

Budget trends

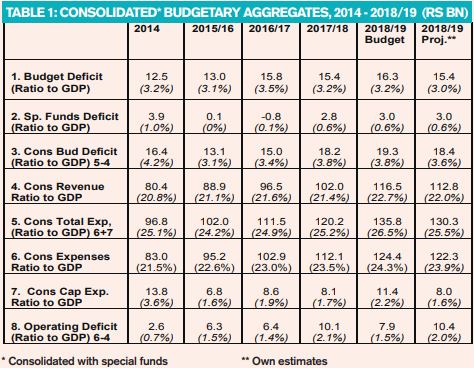

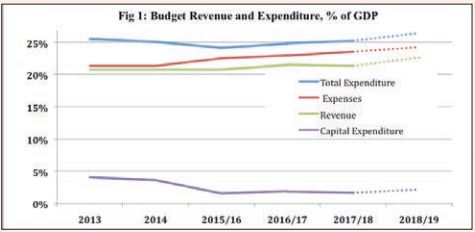

As shown in Table 1, expenses are budgeted to rise to 24.3% of GDP in 2018/19, or an increase of almost 3 percentage points compared to 2014. Expenses are growing too fast, by over 10% annually on average since 2015/16, com- pared to an increase of 6.7% yearly between 2011 and 2014.

Social spending is propelling the growth in expenses, arising mainly from higher social benefits, employee compensation, as well as grants to parastatal bodies and local authorities. Social benefits will overtake employee compensation in 2018/19 as the single most important component of expenses. Social benefits and employee compensation alone represent just over half of expenses.

To contain total expenditures and public debt, as seen in Fig 1, budgetary capital spending has been slashed from 3.6% of GDP in 2014 to 1.7% of GDP in 2017-18, and is budgeted to increase only slightly to 2.2% of GDP in 2018/19. The crowding out of Government investments by high social spending characterizes recent budget performance, and will persist in 2018/19.

Total budgetary expenditure, including downsized capital spending, has been stabilized at around 25% of GDP over the last few years, but is budgeted to rise to a record high of 26.5% of GDP in 2018/19,

Revenue has stayed broadly around 21% of GDP, but is budgeted to go up in 2018/19 to 22.7% of GDP, owing mainly to forecast substantial Indian grants of Rs6.6 bn. The operating deficit, i.e, the difference between revenue and expenses, has widened considerably to over 2% of GDP in 2017-18, and is budgeted to drop to 1.5% of GDP in 2018/19.

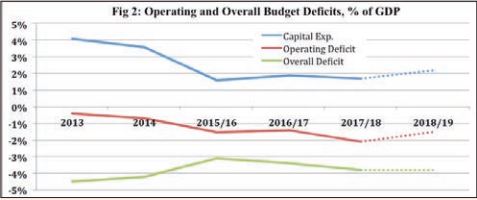

The sizeable imbalance on the Government’s operating account has not led to a serious deterioration in the overall budget deficit, because of strong checks on capital spending. As shown in Fig 2, the consolidated budget deficit was thus initially brought down from over 4% of GDP to 3.1% in 2015/16, but has since risen, with growing expenses, to 3.4% in 2016/17, and further to 3.8% in 2017/18. It is expected to remain at this high level in 2018/19.

In line with the experience of past budgets, shortfalls in both expenditures and revenues are likely in 2018/19. Assuming a shortfall of 30%, capital spending is estimated at Rs8 bn, or 1.6% of GDP. A slightly lower estimate of expenses of 23.9% of GDP is also expected. Total expenditure would thus be limited to 25.5% of GDP.

In the event of a 50% shortfall in Indian grants, as in the previous year, revenue will amount to 22% of GDP. Since the shortfall in revenues and expenditures would almost be matching, the estimated overall deficit in 2018/19 would be only slightly lower than budgeted, at 3.6% of GDP, as shown in the last column of Table 1.

Off budget expenditures

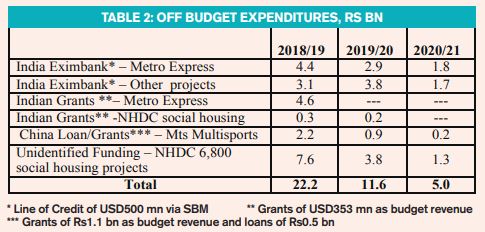

The fiscal deficit is appreciably underestima- ted by off budget capital project expenditures incurred in state-owned SPVs and companies, and other public entities, such as Metro Express Ltd, totaling more than Rs20 bn in 2018/19, as shown in Table 2. There is nothing objectionable per se in the setting up of special funds and public entities for justifiable purposes, as long as their transactions are consolidated with the budget for a proper recording and evaluation of the fiscal deficit and of public debt.

However, the motivation behind the channelling of capital expenditures in public entities is questionable. First, an India Eximbank line of credit is routed via SBM to finance off budget projects in public entities, which include Metro Express, Landscope, NHDC, National Water Development Co., CEB Green Energy, and SIC Dev Co for a total of about Rs7.5 bn in 2018/19, as shown in Table 2. This Govt-guaranteed debt financing is disguised as equity, namely as redeemable preference shares, to avoid inclusion in public debt.

An amount of Rs7.6 bn has been earmarked in 2018/19 as expenditure for the phased construction of 6,800 social housing units by the NHDC. No provision has been made in the budget for financing this programme. A nonbudgetary source of financing, probably from China, remains to be identified, similar to the India Eximbank/SBM credit, to circumvent inclusion in public debt.

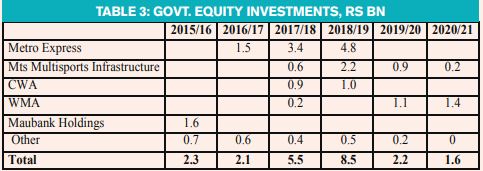

Secondly, Indian and Chinese grants received in budget revenue are also channelled into public entities for financing off-budget project expenditures, namely, in Metro Express Ltd and Mauritius Multisports Infrastructure Ltd, (MMIL), by way of Government equity investments. Equity participation by Govt is not considered as expenditure for the derivation of the budget deficit. Grant resources, which would normally be passed on by Govt to projects as grant expenditure items, are thus cloaked as equity financing to avoid inclusion in the budget deficit.

Govt equity investments, as shown in Table 3, will reach a total of Rs9.7 bn in Metro Express and Rs2.8 bn in MMIL by 2018/19. But, equity returns on the metro express and multisports projects are largely illusory. In 2018/19, off budget project expenditures from Indian grants via these Government equity investments would amount to Rs4.9 bn, and Rs1.1 bn from Chinese grants, or a total of Rs6 bn.

Deceptive accounting to finance off budget expenditures undermines the integrity of our fiscal and debt management. This practice is not altogether new. A glaring example is the long standing utilization of another public entity, namely the State Trading Corporation, to hide away from the budget a substantial amount of petroleum taxation as well the cross subsidies on some basic household consumption items.

For a correct estimation of the budget defi- cit, Metro Express, MMIL, and other off budget project expenditures should be consolidated with the budget, as with special funds. Even if only half of off budget project expenditures are realized in 2018/19, this would represent an amount of Rs10 bn, or about 2% of GDP. Including off budget project expenditures, capital spending, would not exceed 4% of GDP, but the consolidated budget deficit would be well over 5% of GDP in 2018/19.

The year 2018/19 will reflect a sharp bunching of capital spending, owing to the Metro Express project. But, the planned off budget expenditures in successive years are also sizeable, adding 1 to 2% of GDP annually to the budget deficit. Public indebtedness is already high, and heavy fiscal deficits are not conducive to debt correction and the aim of long term debt sustainability.

Fiscal adjustment

The current expansionary budgetary stance is not sustainable. Crucially, the growth in non-capital expenses must be reined in more strongly to allow greater room for public investment. While off budget capital expenditures provide an extra investment stimulus to the economy, the high level of public debt limits the scope of such spending, A sound option is to restructure the operating budget imbalance, by restraining the growth in expenses, and raising the tax revenue effort.

The official objective of fiscal strategy is geared towards “greater fiscal discipline and putting public sector debt on a downward path”. But, as in previous years, fiscal discipline is always deferred three years into the future, and meant principally for the consumption of the IMF and credit rating agencies.

The fiscal plan presented in the 2015/16 budget projected the reduction of public sector debt to the then statutory target of 50% of GDP at end 2018, through fiscal consolidation to lower the budget deficit to 1.6% of GDP in 2017/18. The actual deficit is twice as large. Government’s fiscal plan is now to meet the public sector debt target of 60% of GDP at June 2021 by eliminating the operating deficit, and reducing the overall deficit by 1.2% of GDP, between 2018/19 and 2020/21.

This fiscal consolidation in the coming years will purportedly be achieved almost entirely by a deep cut of 2.5% of GDP in expenses, and an unchanged capital spending ratio to GDP. The required adjustment in expenses, after accounting for special funds and off budget expenditures, would be even more painful. The illusion that current government spending growth can be sustained will eventually be shattered.

Public debt

Public Sector Debt (PSD), comprising the debt of General Govt and of Public Enterprises, has emerged as a source of concern in recent years. The latest 2018 Moody’s Report noted that “Mauritius Government’s debt is elevated and above the Baa-rated median”, but also recognized that, despite ‘a relatively high government debt level”, a risk mitigating factor of the country’s public indebtedness is the major preponderance of domestic debt.

Moody’s expect that ongoing challenges will be addressed by economic policies, and that Government debt will stabilize, albeit at an elevated level. Moody’s public debt analysis focuses only on General Government, and does not cover public enterprises.

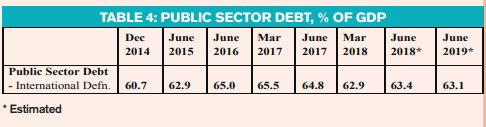

PSD, on the international definition, went up to 65.5% of GDP at March 2017 as against 60.7% at end Dec 2014. However, the PSD ratio dipped to 62.9% of GDP in Mar 2018. Transfers of Rs4.8 bn from special funds to the Consolidated Fund, representing 1% of GDP, contributed largely to this improvement in the PSD ratio.

The 2018/19 budget estimates that the PSD ratio will climb again from its March 2018 level to 63.4% at June 2018, and then decline marginally to 63.1% at June 2019, assuming a similar budget deficit outcome as in the previous year. However, the deficit will actually be much higher on account of off budget expenditures, and official debt is itself underestimated.

A statutory debt target of 50% of GDP un- der the Public Debt Management Act 2008, based on a local definition, was missed in 2013, and a first amendment to the PDM Act postponed the debt deadline to Dec 2018. In a further amendment last year, the local definition of public sector debt was replaced by an “international” definition, and the debt target was changed to 60% of GDP while the deadline was further postponed to end June 2021. Provision was also made to facilitate further adjustment of this deadline by simple date changes to a schedule under the Act.

The “international” definition as applied in the official reporting of PSD data is a narrow one that includes, besides General Government debt, the debt of only a select number of public enterprises. Currently, the official figure of General Government debt is around 55% of GDP, and public enterprise debt about 6% of GDP. The recommended IMF definition of PSD is broader, and comprises financial and non-financial public corporations. Non-commercial public enterprises such as CEB, MWA, CWA, are covered in our official public sector debt data, but some important state owned public enterprises, namely, SBM, Mauritius Telecom, Sicom or Maubank, do not appear to be included.

Government is taking advantage of these exclusions, to channel foreign borrowings to SBM and MT, and thus avoid any recording in public sector debt data. An India Eximbank line of credit of USD500 mn, or over 3% of GDP, is being routed via SBM, for the Metro Express and other projects, and a China Eximbank line of credit is being extended to Mauritius Telecom, for the safe city project. Government is contracting the safe city project to MT on a leasing arrangement, so that the desired investments are undertaken by MT from China Eximbank funds.

It is feared that substantial foreign financing for the construction of 6,800 social housing units, valued at USD 350 mn, or over 2% of GDP, may be similarly directed to NHDC, without being included in official PSD.

By the full inclusion of debt by public entities, PSD could possibly even reach 70% of GDP. With proper accounting, it is most improbable that the 60% debt target will be reached by 2021 without major fiscal adjustments. More importantly, an adverse shock to the economy, especially stemming from external sources, would make a high debt burden unaffordable, and lead to unavoidable fiscal correction.

Fiscal transparency

While concerns on high fiscal deficits and debt are legitimate, it is equally important not to succumb to deficit or debt phobia. The authorities should abandon the dubious subterfuges adopted to fiddle with the recording of capital expenditures and public debt. In accordance with good fiscal governance practices, the reporting issues on public enterprise debt should be clarified, the expenditures of the relevant public entities consolidated with the budget, and their borrowings included in public sector debt.

High deficits can be addressed by appropriate fiscal consolidation measures, starting with the recognition that a policy of benevolent social spending cannot be sustained for long without adjustment. It is simply astounding to note the dissolution of the committee on pension reforms and the abandonment of the proposed measure to eliminate the double payment of both emoluments and basic retirement pensions to public employees still in service until the age of 65. The absence of any meaningful reforms in public utilities and the delivery of public services does not bode well for enhancing the economy’s productivity and growth potential.

Even off budget capital spending has its limits imposed by debt considerations and would be insufficient to impart a sufficiently strong stimulus to the economy. Projects contracted loosely to public entities carry heavy risks of improper project evaluation, as for Heritage City, associated with sizeable wastage and potential cost overruns, and offer greater scope for corruption. Sound PPP or BOT projects are worthy of greater consideration for boosting investments. Doing away with programme based budgeting, and the return to outdated line item budgeting and the recurrent/capital classification, was a most retrograde decision for ensuring modern and rigorous public investment management.

An open and transparent accounting of PSD can be viewed with less difficulty in the light of a credible fiscal restructuring plan. A key debt mitigating element is the low share of external debt, accounting for less than a quarter of total debt. Moreover, the Eximbank loans from India and China are sizeable, but have a significant grant element, due to relatively long maturity and grace periods.

Conclusion

The consolidated budget deficit has climbed to almost 4% of GDP in 2017/18, and could be well in excess of 5% of GDP in 2018/19, after including off-budget expenditures. Driven by social spending and employee compensation, noncapital expenses show continued growth to reach around 24% of GDP in 2018/19, well above the stable level of non-grant revenue at 21% of GDP. A significant effort at fiscal discipline is required to rebalance expenses against revenue.

The need to contain the mounting deficit and public debt levels has been at the expense of a downsizing in capital spending, Unless the budget is restructured, public capital spending cannot be expanded significantly to meet the infrastructure upgrading needed for more vigorous growth. Even with an exceptional buttressing of revenue by Indian and Chinese Grants, the deficit remains too high for the required correction in the relatively high public debt burden.

Painful fiscal adjustments to curb social spending growth will become unavoidable in the coming years. Government’s fiscal strategy already plans for a much slower growth of expenses by 2020/21. The integrity of fiscal management and the attainment of the 60% PSD target will encounter serious doubts, without better transparency and openness in the reporting of public expenditures and indebtedness. Despite mitigating factors, an unanticipated adverse external shock could still put the country’s international credit rating at risk, by reducing Government’s ability to carry a relatively high debt burden.

Finally, budgetary policies that promote consumption at the expense of capital spending will not generate durably higher growth, but aggravate the current account deficit and heighten the exposure of the economy to external shocks. The relatively high external current account deficit reflects high consumption, or depressed savings, exacerbated by poor export competitiveness and performance, and reveals a crucial vulnerability of the economy to global financial turmoil.

Global Business Companies play a critical role in financing our balance of payments, but face growing uncertainties. Capital flows are currently flowing out of emerging markets as monetary policy tightens in the U.S., and the U.S. dollar shortage worsens. Adverse external sector developments could pose serious risks to our economic prospects.

The policies of the 2018/19 budget are focused more on extending social largesse, and less on rectifying the economy’s structural economic imbalances and addressing current challenges, to improve its resilience, productivity and competitiveness.

Publicité

Publicité

Les plus récents