Publicité

Offshore and financial services: How real is the threat of emerging African financial centres to Mauritius…

Par

Partager cet article

Offshore and financial services: How real is the threat of emerging African financial centres to Mauritius…

Kenya is now positioning itself as a financial centre looking to go into fintech. Nairobi’s rise is part of a larger pattern of more African states wanting to position themselves as financial centres on the continent. Is their rise coming at Mauritius’ expense? What is the bigger problem that the focus on Africa tends to ignore?

- The rise of the rest

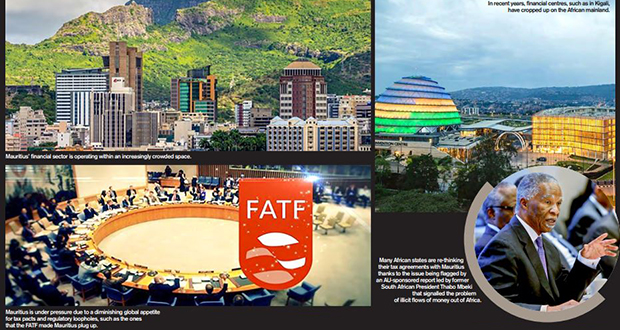

Kenya this month launched its International Financial Centre in Nairobi in a bid to expand the presence of its financial sector into the global tech start-up and fintech market. So far, funds from the UK have expressed interest in setting up in Nairobi. Kenya’s plans are just the latest in the emergence of African states looking to set themselves up as international financial centres. Is Mauritius’ own IFC risking being left in the shade? “This is a problem because they know Africa better than most Mauritian operators,” argues Reza Uteem, a parliamentarian from the opposition MMM Party as well as a lawyer working within Mauritius’ sprawling offshore industry, “having said that, Mauritius still has a lot to offer such as a bilingual workforce, a strong track record since 1992 as a financial centre and a clean bill of health from the Financial Action Task Force (FATF)”.

Just how much of a problem the increasingly crowded financial sector space within Africa is for Mauritius’ own industry depends on the country; “there is nothing new in terms of the ambitions of countries to start new economic pillars, there are now already more than 100 countries in that space,” argues Rama Sithanen, former finance minister who ushered in the financial services sector back in 1992, “it just means more competitors for Mauritius in the medium to long term.” Kenya just joins a much longer list of African states, each with their own specificities. Rwanda has been seen as a potential competitor. “It’s a smaller state, compared to Kenya, so can be much more agile in innovating. Kenya has to deal with a bigger bureaucracy in bringing in laws to become a financial centre,” argues Marc Hein, chairman of Jurisconsult, who also chaired Mauritius’ Financial Services Commission (FSC) until 2014, “while Casablanca is attracting business from France; we need to do more to attract francophone business flowing towards Africa.”. While Johannes- burg has traditionally looked inwards towards the South African economy. Given the diversity of focus within these budding financial centres on the African mainland, Hein argues, “we can be optimists and see these centres as complimentary to one another”. The implication being that each would serve a particular niche of capital flowing into the continent.

- The treaty network in trouble

The emergence of these centres also comes in a particularly difficult context for the Mauritian financial services industry that counts for 8 per cent of its GDP and rakes in 8 per cent of its taxes. “For a long time, Mauritius has been the only recognized IFC in Africa.” says Milan Meetarbhan, who worked as the FSC’s Chief Executive between 2005 and 2010, “even then in the early days you had development finance institutions structuring their investments into Africa via Mauritius because they thought it was a good idea to domicile their funds in an African state.” Mauritius has since looked to build up on its pull within the continent by signing a series of double taxation avoidance agreements (DTAAs) with African states. The problem is that in recent years, these treaties have either been torn up by some of these states or renegotiated by others. Just in 2020, Senegal and Zambia scrapped their tax treaties with Mauritius, claiming they were unfair towards them and deprived them of tax revenue. –

In 2019, Kenya’s treaty with Mauritius was broken down by its High Court which argued that the treaty had not been properly ratified. Rwanda renegotiated the treaty it signed with Mauritius in 2001 and signed a new one in 2014. While South Africa had already reworked its 1997 treaty with Mauritius. Other states such as Namibia, Lesotho and the Republic of Congo are threatening to go the same way. “The problem in Africa is that Mauritius now has the image that it is taking away the taxation rights of poorer countries” argues Uteem.

The reason for this slew of problems is that the types of treaties that Mauritius signed with these states are fast falling out of favour. Put broadly, such tax treaties followed one of two models: one developed by the United Nations (UN) that upheld the taxation rights of countries being invested in; and one by the Organization for Economic Co-operation and Development (OECD) that tended to favour the taxation rights of states where the investments were coming from. The treaties signed by Mauritius were patterned on the OECD one. “A DTAA is essentially an agreement on how to share taxation rights; the OECD model favoured investors because the OECD was made up of investor countries,” argues Sithanen, “so taxation rights for things like capital gains, royalties, dividends, technical fees and so on were skewed towards states where the investments came from. The trend now is a shift to a more balanced model and away from these treaties, which were seen as too favourable to Mauritius, and which are now being renegotiated.”

Just why these treaties are falling out of favour rests on two arguments that Sithanen outlines: the first is that going through Mauritius is simply an expensive diversion of investments that would have come anyway. “Of course, one can invest directly, but you may face problems like discrimination against foreign companies, problems taking our foreign currency or problems with the government with their investments threatened. Big countries like China can go directly in because they can just thump the table, but smaller countries and companies cannot, so they would want to secure their investments by going through a country like Mauritius,” says Sithanen.

The second argument is that such treaties deprive poor, African states of much-needed tax revenue. Put sim ply, companies wanting to invest in Africa would simply - open an office in Mauritius and pay much lower taxes to Port-Louis than in the country they were investing in. “Indeed, there were clients using Mauritius for tax incentive reasons, and we need to keep working on what we have and can offer to stay competitive,” says Hein. The answer to this argument, Sithanen says, is that “zero times zero is still zero; if the investors don’t come, neither does the tax revenue. Many states offer attractive tax rates; in Mauritius itself many companies in the EPZ sector and smart cities effectively pay no tax; the argument here is that you forego some tax revenue in exchange for economic growth, development and jobs. And taxes are somewhat made up by increases in income and consumption taxes that result”.

But this has become a harder sell to African states that are heavily reliant on money from taxing corporates and extractive industries. Senegal and Zambia, for instance, ripped up their own treaties just as the latter is looking to expand its oil and the latter its mining industries. “Most of the reworked treaties and states now make the distinction between natural resources under the soil and above-ground investments,” says Sithanen.

Other pressures

What also has not helped is a number of self-inflicted PR disasters such as the hosting of Angolan billionaire Alvaro Sobrinho accused of embezzling money from Angolan banks; or Mauritius playing host to funds run by the family of former Angolan president Eduardo Dos Santos, which became a major issue for relations between Luanda and Port-Louis back in 2018. All this has brought grist to the mill of organizations such as the International Consortium of Investigative Journalists, which periodically published leaks – including the ‘Mauritius Leaks’ in 2019 – outlining in detail how foreign businesses and celebrities avoided paying higher taxes in Africa by shifting their funds through Mauritius. “We have to be aware of the political circumstances in the continent, where NGOs play a strong advocacy role, and their messaging has been that African states have lost a lot of money,” says Meetarbhan.

It has not just been NGOs. A lot of African anger also stems from findings such as from the AU and UN-sponsored report of the High-level panel on illicit financial flows (IFFs) from Africa, estimated to be to the tune of $50 billion a year, which concluded that “one driver of overall exposure in relation to IFFs is the high exposure of individual African countries, most notably Mauritius. Its operation as a relatively financially secretive conduit results both in high exposure for itself, but also for other countries across the region”. This is coupled with pressure from developed states themselves to harmo nize global tax regimes to crack down what they see as tax - havens. Examples include the OECD’s Base Erosion and Profit Shifting Action plan to crack down on tax-dodging international businesses, the G7’s proposals of a global minimum tax rate of 15 per cent and of course the Financial - Action Task Force (FATF) founded by the G7 states, which placed Mauritius on its grey list between February 2020 and October 2021, forcing Port-Louis to make key changes to plug up loopholes in its financial regulatory regime.

- The India angle

IF this sounds familiar, it is. In effect, Mauritius patterned its initial tax treaties on African states on its 1981 DTAA with India. When Mauritius officially embarked on plans to develop its financial sector in 1992, although some businesses wanted to go into Africa, such as an oil company that wanted to set up an operation in Mauritius to attract Western investors to go into West African oil, the bulk of the business was done with India that was just beginning to open up its economy to foreign capital. The influx was enormous: between 1994 and 2017, 37 per cent of foreign direct investment coming into India was coming through Mauritius and 27 per cent of all foreign portfolio investment between 2001 and 2016.

However, starting from the late 1990s, Mauritius’ image began changing in the Indian mind. A joint parliamentary probe into a 2001 stock market scam – where a broker Ketan Parekh was accused of circular trading to artificially pump up the price of stocks of 10 companies, and then cause a subsequent stock market crash – found that the scam involved shifting money to companies registered in Mauritius. Starting in 2004, the Indian government began pressuring to amend the DTAA with Mauritius. In the meantime, Port-Louis started figuring in a series of scandals such as 2G spectrum allocations or the procurement of Augusta Westland helicopters. Finally, in 2016, India succeeded in convincing Mauritius to amend the DTAA. “With India we had strong ties; so we could negotiate, reassure them and work to contain that,” says Uteem, “but with a lot of African states, we just don’t have the same relationship. And Mauritius does not seem to have much of a strategy to stitch up these DTAAs with African states. What is clear is that we cannot just use the same model that we did with India.”

The amendment of the DTAA with India is what lent urgency for Mauritius to take a good, hard look at Africa as an alternative. “Before that the major players were just looking at India and China and largely ignoring Africa,” argues Meetarbhan. So how successful has this push to diversify into Africa really been? “We have made progress, the share of funds looking towards Africa has increased and 50 per cent of DFIs going into Africa go through Mauritius,” Sithanen argues, “but in terms of value addition, India is still the most important segment, most of the big funds are still India-focused, this is because India is just one country with a single regulatory framework, whereas Africa is 55 countries; so leaving aside the DFIs, these tend to be much smaller.”

According to the Bank of Mauritius in December 2021, 69 per cent of funds in Mauritius’ global business sector were still going to India, compared to just 19 per cent to Africa. The continuing outsized importance of India to the Mauritian IFC indicates although the emergence of other African financial centres is worrying, in reality, the greatest vulnerability for the Mauritian IFC is the emergence of GIFT City in the Indian state of Gujarat in 2015 as India’s first IFC. “India is now trying to create that same ecosystem that Mauritius provided, this is nothing controversial as even Mauritius would want to keep as much value addition within its country as possible,” insists Sithanen, “but the political class in India can pressure its own, and outside businesses to route their funds via GIFT rather than Mauritius. But how successful this will depend on how GIFT interacts with the rest of the Indian regulatory system it has been carved out of.” This is a serious issue for the wider Mauritian economy as its IFC is not just a source of ready foreign exchange but money out of its global business sector makes up a third of deposits in the Mauritian banking system.

- The way forward

So where does Mauritius’ financial services sector go from here? “We need to become more competitive, and need a paradigm shift because right now we are essentially at the same place we were back in 1992,” Sithanen laments. This does not just mean the focus on India of the financial services sector, but also the type of services it offers. Structuring cross-border investments still accounts for 60 per cent of the Mauritius IFC’s business and 88 per cent of the taxes coming from it. The relatively slow pace of change is partly explained by fears over the Indian DTAA revisions and partly by the concentrated nature of this segment. Just 10 management companies run nearly half of this segment. With 32 per cent of the financial services sector made up of cross-border corporate banking bring approximately $480 million to Mauritian banks yearly.

The Ministry of Financial Services and the FSC commissioned the global firm McKinsey to conduct a study in 2018 about where the sector should head next. Aside from deepening and diversifying the investment and banking side of the business, the report also urged Mauritius to plunge into private banking and wealth management – currently less than 5 per cent of financial services netting the sector $94 million – as well position itself as a regional specialist for Africa and India, as well as specialize in certain service lines just as Dublin is for hedge funds or the Cayman Islands is for insurance. This it said, could only be done if it hired more expats. “What is now affecting Mauritius is the high rate of tax which expats are paying, with the solidarity levy being paid at 25 per cent. We are no longer being considered as competitive for those setting up business or working here. We have to address our minds to this issue rapidly,” insists Hein. Only then could Mauritius realize its plans to double the size of its IFC by 2030 and stand out amongst other IFCs in Africa and elsewhere.

Publicité

Publicité

Les plus récents