Publicité

Unconventional Monetary Policy: The Darker Side

Par

Partager cet article

Unconventional Monetary Policy: The Darker Side

While the world economy is recovering slowly but surely, that of Mauritius is struggling. According to the author, the impact of printing money in itself may not bankrupt a State but it can certainly bankrupt everyone else, especially the poor and the middle class.

There has been a lot of confusion about whether the Bank of Mauritius (BoM) is engaging in quantitative easing (QE) like many other central banks are currently doing, taking money from our “reserves”; issuing BoM instruments to the market in order to finance the “exceptional” one-off grant; about the sustainability of Government debt; and finally about whether all these measures have been able to turn around the economy so far. To be clear, Mauritius had no choice but to go the unconventional route, but there is no such thing as a free lunch.

The sheer scale of these unconventional measures, the lack of a clearly formulated and sustainable debt path and tax policy, the design of these unconventional policies themselves, the lack of accompanying meaningful productivity enhancing structural reforms, when coupled with exogenous factors, will not only have significant longer term consequences on the balance sheet of the central bank and on its ability to contain a higher inflation regime, but defending an already weakening rupee, on protecting purchasing power and on protecting against rising income inequality.

Quantitative easing non Japanese-style means that a central bank purchases Government or other bonds in the secondary bond market and, in return, injects digitally created money into the system. From a public debt accounting standpoint, this is still treated as a liability for the Government and is reflected in debt numbers and is an asset typically held at amortized cost on the balance sheet of the central bank.

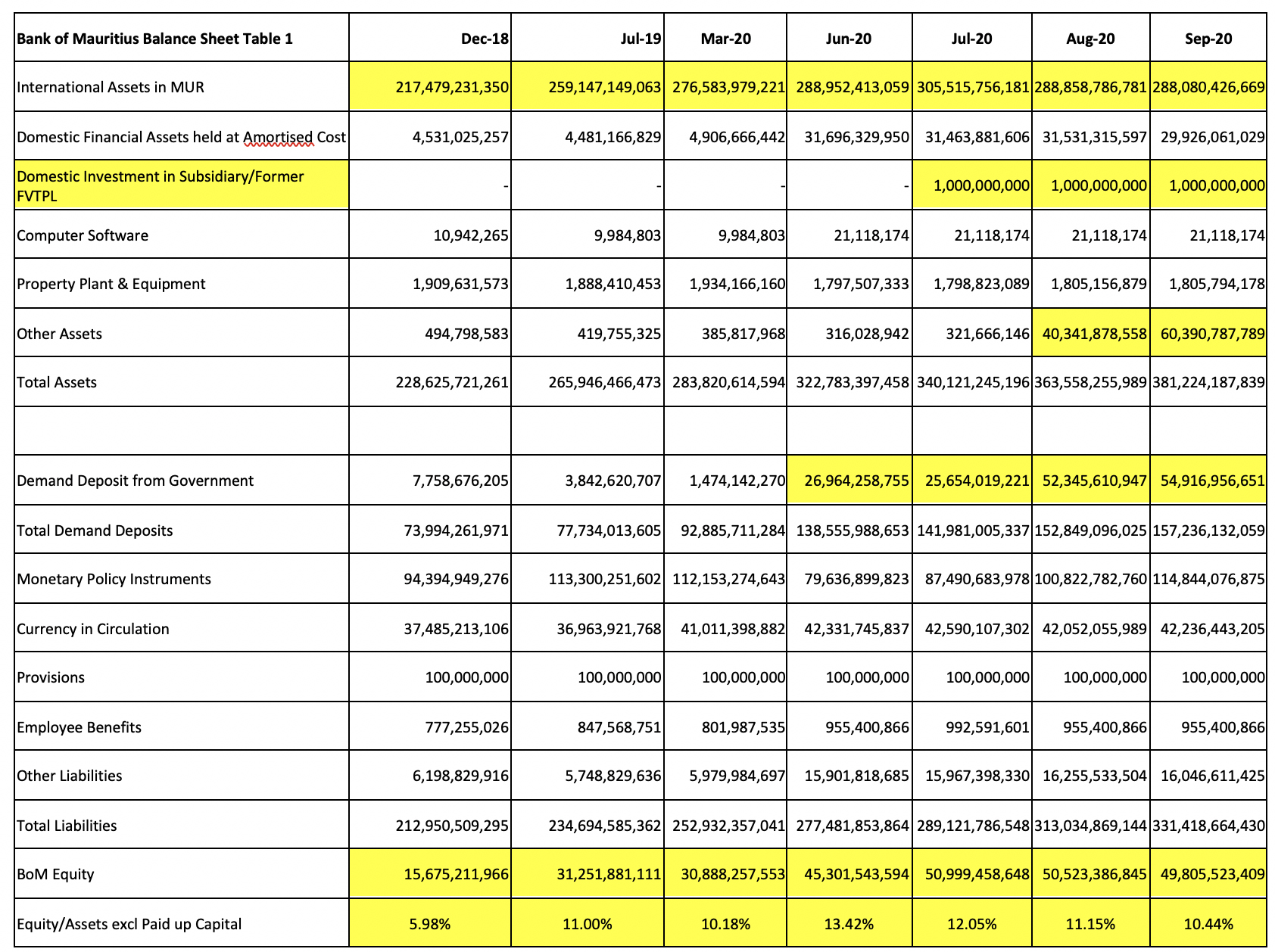

On the other hand, the monetization of fiscal deficits occurs when the central bank simply creates money by a simple entry on the asset side of its balance sheet and credits the money in the Government’s account. The financing of the “exceptional” Government grant has largely been financed by the latter so far rather than the former. If we simply look at the evolution of the summarized balance sheet of the BoM as showcased in Table 1, we see that from March 2020 to June 2020, domestic assets held at amortized cost, which include other advances from the BoM, increases significantly from Rs 5Bn to almost Rs 32Bn.

We also see in Liabilities that Government demand deposits in the system also mirrors this increase and increases from a mere Rs 1.5Bn in March to Rs 27Bn in June. While part of this increase in Government cash balances can also be attributable to other factors such as the conversion of obtained foreign loans, there is a clear link. It is not known whether the increase in assets held at amortized cost is driven by secondary bond market purchases which would be QE or via a zero cost perpetual paper bond which would not be QE but what is clearer is what happens in August and September 2020 when the BoM changes strategy.

Table 1

Note that the Other Assets category of the BoM increases from a tiny Rs 321M in July 2020 to a whopping Rs 60Bn in September. At the same time, Government demand deposits increase from the already inflated Rs 26Bn to nearly Rs 55Bn. Of course, the Government is also spending some of the cash at the same time, so numbers will not add up perfectly. Now there have been reports that the BoM would be financing the exceptional grant by issuing monetary policy instruments and hence remove existing excess liquidity from the market and while this may have partly been the case in September, it should be obvious that since March, the outstanding value of monetary policy instruments has been largely flat and does not mirror changes in the Government cash balances as these other explanations do. Regardless, the BoM has created money like there is no tomorrow and injected it into the system.

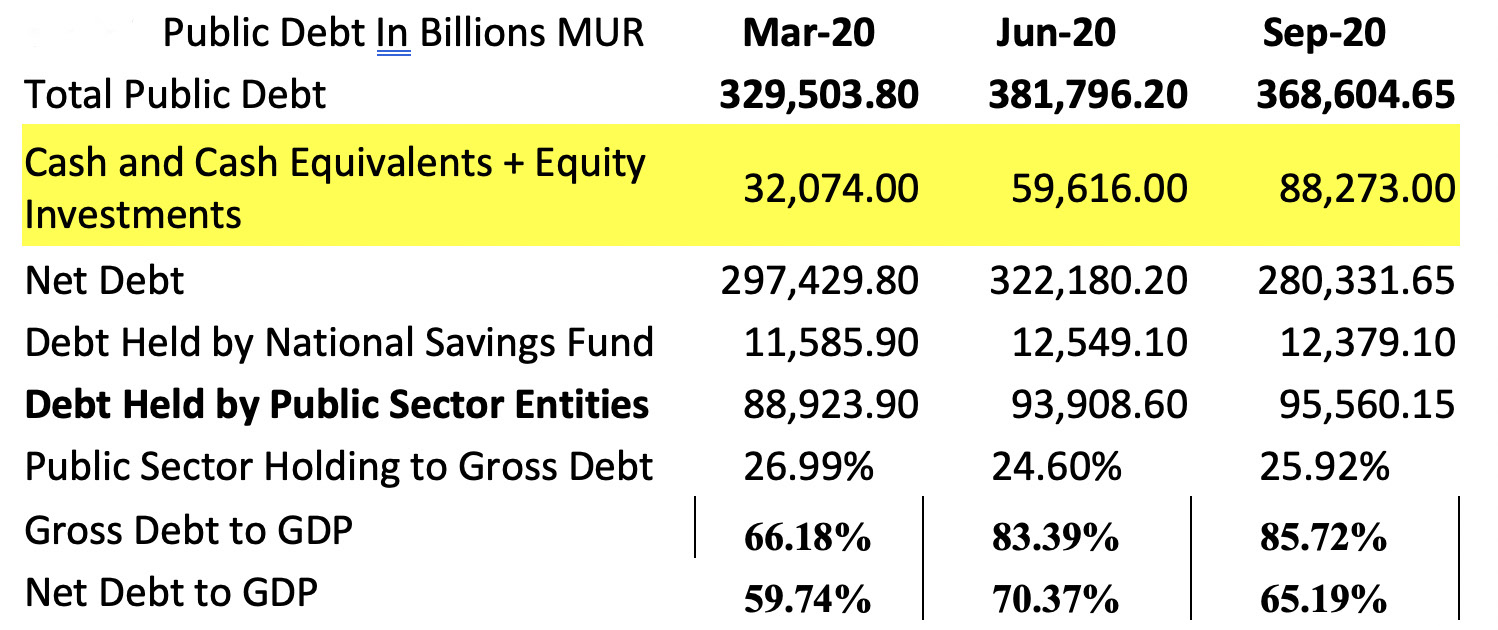

Now let us look at Table 2 which shows the fortunes of the central Government and note the change in cash and cash equivalents since March 2020 and why the Finance Minister talks about net debt rather than gross debt. The Government began to include the estimated value of its equity investments plus the cash since at least March 2020 but note the increase of nearly Rs 56Bn (mirroring the Rs 53Bn increase in demand deposits during the same period) in this category and more importantly note what happens to net debt when compared to gross debt. This is the result of money creation and transfers on the debt by the central bank at work. It is full coordination between fiscal and monetary agents acting as one. At the same time, public owned entities and funds such as the National Pension Fund also help keep demand for Government bonds at high levels in order to keep rates low by increasing their holding of Government debt in nominal terms.

Table 2

Table 3

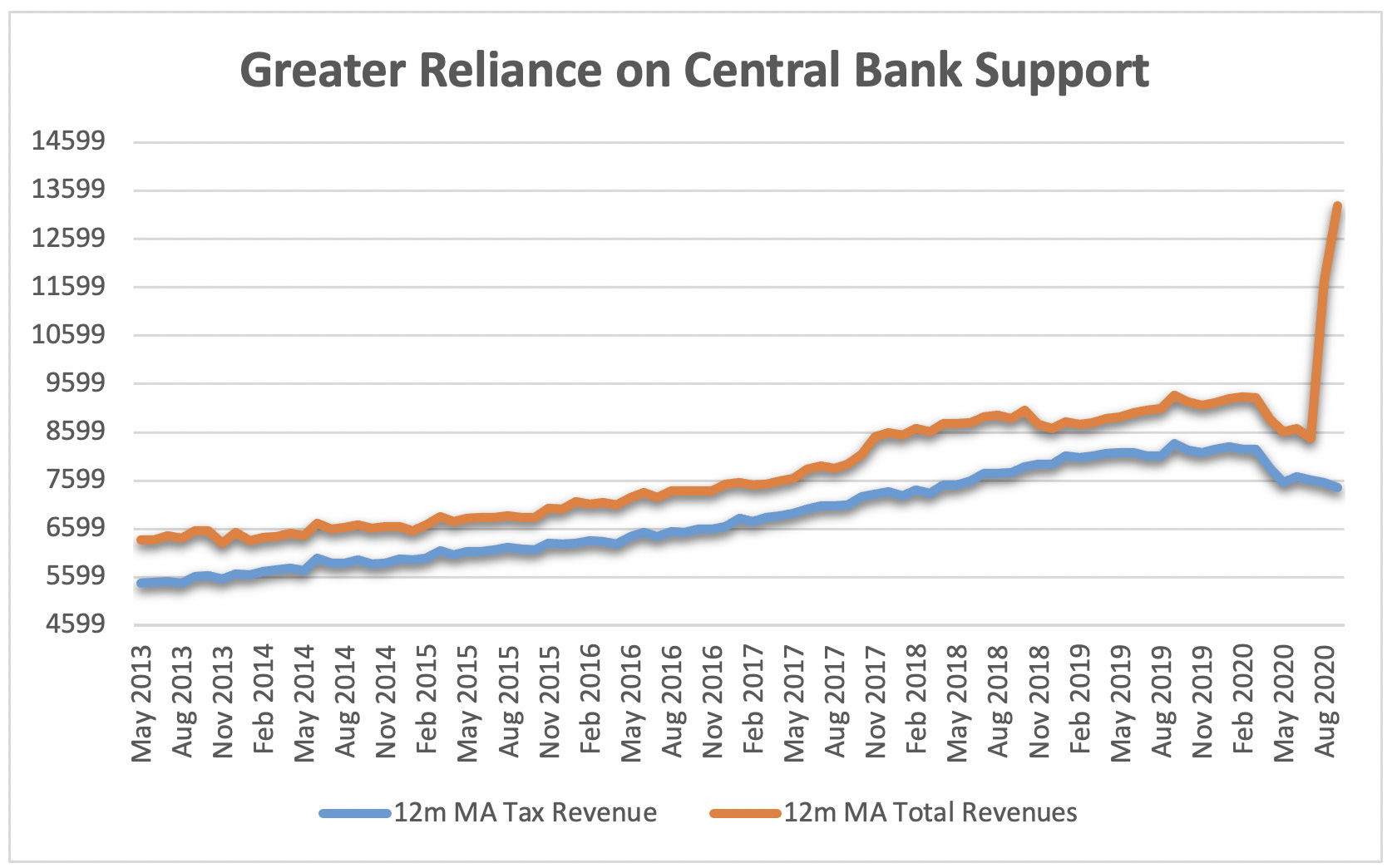

This analysis is further enlightened by the Chart which shows the rolling 12 month moving average of Government tax revenues which diverge significantly from total central Government revenues which are bloated in August onwards (the real spending gains momentum) from what it categorizes as Other Income (you can guess from whom). What is interesting about the chart is that tax driven Government revenues, which are a good higher frequency indicator of the health of the real economy, are still weakening which showcases the common sense fact that printing money is one thing, creating real growth out of money printing and loans is another. There is no Vshaped or U-shaped recovery for Mauritius yet. We are still struggling while the rest of the world is recovering slowly but surely.

But this is not all. Take a look at Table 1 again focusing on December 2018. The rupee value of international reserves stood at Rs 217Bn and the level of equity as a percentage of total assets of the BoM was a mere 6%. Now come to September 2020 and notice that the significant depreciation of the rupee against major global currencies and foreign loans have helped to bloat the rupee value of international reserves (its rupee value is actually meaningless to the outside world) to Rs 288 Bn. This has been a key driver of the increase in the economic capital of the central bank to 10.44%.

To be clear, since the value at risk of major global currencies against the rupee such as the USD and EUR are themselves higher than this level of economic capital, it should not be too complicated to realize that a weaker rupee or at worst a stable rupee from current levels is what the central bank would not mind and prefer. An appreciating rupee, for example, would have a greater than one-to-one impact on its balance sheet and level of economic capital which in any event is mostly on paper. At the same time, the BoM is also supposed to sell international reserves in order to fund dollar demand in the domestic market and then take the earned rupees and rather than making them disappear, inject them into the Mauritius Investment Corporation to bail out distressed companies.

As I have previously written, any mis-pricing of any so called “quasi equity” bonds which have nearly zero equity sensitivity given their structuring if valued as they would and should be in the US or Europe could lead to a nasty surprise for the BoM. Curiously, in June 2020, the BoM introduced the classification of Fair Value Through P&L under domestic asset but replaced this classification merely three months later with the updated classification Investment in Subsidiary, why?

Imagine tomorrow, we get more inflation, be it from an exogenous regime change or from all this money creation, the BoM will in theory need to raise interest rates and also require it to remove all these injected rupees from the system. Higher rates would also hurt distressed companies, which still have floating rate bank loans and impact the balance sheet of the Rs 80Bn subordinated debt holder, the BoM.

Rising rates and liquidity sterilization will quickly inflate its liabilities and eat away at its economic capital. Unless the rupee depreciates or is depreciated, one can see that there can be many scenarios where the BoM’s credibility in fighting inflation or in defending the rupee may be questioned by the market. The BoM has not announced any framework for an exit strategy.

Post-2024, unless the Government raises taxes and expands the contributory base further, the former NPF assets will start getting depleted, which means lower demand for Government bonds which may push up debt service costs. To avoid this, the BoM itself may be forced to intervene and bloat up assets held at amortized cost via secondary market bond purchases or further monetization. Once you scale unconventional measures to such an extent and once the Government becomes addicted to free money, it becomes very hard to find an exit strategy.

Printing money may not be able to bankrupt a State which still has a relatively manageable level of external debt and a majority of “monetizable” local debt but make no mistake, its impact on the currency and eventually on inflation can certainly bankrupt everyone else, especially the poor and the middle class. This is why it remains important for policy makers to bite the bullet and now begin to engage in meaningful productivity enhancing structural reforms, and for the private sector to do some overdue introspection about their historically skewed debt heavy capital structures and think of new business models, and be more open to other private market investors or/ and the equity markets as a source of capital.

On the public side, the Government will have no choice but to contain spending, depoliticise and de-centralize power so institutions can run without being remote controlled, raise taxes on the rentier economy via property or land value taxes post-2021, deepening the capital markets, reforming and bringing much needed efficiency to public owned companies, rationalizing the state’s role and participation in poorly managed corporations, temporarily constrain Government employees’ wage growth rather than printing money, more openness to public private partnerships, freeing up resources in order to make meaningful investments into new and emerging sectors of the economy, building the data architecture which will allow AI to eventually develop, investing more and demanding more from a failing education system where only the children of the elites can make it, investing much more in re-skilling and in creating a more fluid workforce, being much more open to immigration and to a younger generation of foreign entrepreneurs, developing an alternative funding ecosystem to banks for start ups and mid caps, establishing an independent budget office which will critically assess the spending plans and electoral promises of politicians, enhancing the powers of the competition commission and the efficiency of the courts in judging business related cases. Last but not least, pension reforms are overdue in Mauritius especially given the unfavourable demographics and low for longer nominal bond yields which push up the present value of liabilities. Beyond making changes to the way we manage pension money, the contributory base will need to widened and include all employees public and private and contributory rates will need to be reassessed by actuaries.

Relying on unconventional monetary policy to such an extent for much longer is a recipe for the implosion of the currency. Firstly, deglobalization and the associated balkanization of supply chains will be accelerated by the post- Covid-19 desire by many major economies to achieve greater domestic resilience against a range of potential shocks. This means reduced global specialization and higher costs. Less “offshoring” could mean that domestic workers will have more bargaining power in the West, pushing inflation higher. Second, major central banks are evolving their policy frameworks and explicitly intend to let inflation overshoot their targets.

Third, in the case of Mauritius in particular, given balance sheet realities for the BoM, I see a high risk of the BoM losing grip of inflation expectations relative to recent levels, given the amount of rupees which have been printed, given the lack of proper policy guardrails against full on coordination, central bank independence concerns, the lack of any quantifiable flexible inflation target for which the BoM is made accountable for and a viable exit strategy from current stimulus measures. The combination of external factors and domestic structural weaknesses does not bode well for the 12-24 month ahead inflation outlook and purchasing power as global economic slack gradually recedes.

Once higher inflation appears, it’s likely going to be too late for the majority of Mauritians to react – markets would have already moved to price in higher inflation expectations via a much weaker rupee. The Mauritian elites who have all been slowly but surely pulling out an accumulated one trillion rupees out of Mauritius overseas over decades as per the MRA, despite our “top 20 top places to do business ranking” will survive but how about the rest? It is the depressing answer to this very question which we must aim to avoid.

Publicité

Publicité

Les plus récents