Publicité

A 9 % growth is NOT realistic !

Par

Partager cet article

A 9 % growth is NOT realistic !

Fatal fault lines in macro-economic management – short and long term – crisscrossing each other have emerged in the recent past. With an economy that has shifted from ‘aided’ expansion to ‘deadened’ performance, cooperation between the Government and the rest has turned into contestation. Economic statistics put out in recent times are failing litmus tests. Growing distrusts and a lack of faith in our official statistics go against the grain of economic governance. A popular perception that some of the key macro-economic indicators are a fudge rushed out to win plaudits is regularly cast on the table. The discontents about the lack of a convincing official response based on solid economic reasoning seem to be leaving observers deeply concerned. A few economic commentators and business persons have suggested that I should give my views of the country’s performance in terms of inflation rates, GDP growth rates etc. Hereunder are a few thoughts not intended to put our Statistics Office in a bad light but to highlight a few concerns that could help formulate educated opinions and decisions. I have, as far as possible, tried not to burden the laypersons with technical terms in this short exposé.

A convenient approach would be to start with the rate of inflation that, as is well known, is a measure of the rate of increase in the weighted prices of a basket of goods and services that is representative of an average household in the country. For the purpose of some points that will be made later, it is pertinent to underline that this basket (referred to as the CPI basket) does not include a wide variety of goods and services (all intermediate and capital goods and other inputs) that go into the production of goods and services in the economy. While on the consumption side the CPI indicates the evolution of prices of consumer goods and services, on the production side the GDP deflator indicates the evolution of prices of inputs that go into productions in the economy. For the layperson, the distinction between the CPI and the GDP deflator may be best stated as follows: the CPI is an index for the cost of living while the GDP deflator is an index for the cost of production. The latter is used to calculate the size of GDP, adjusted for price increases during a specified period of time, usually a financial year or calendar year.

We are overwhelmingly dependent on imports and exports. As such the exchange rate of the rupee is pre-eminently a dominant variable in price formation in the economy. A time-series analysis of the indices of an appropriately trade-weighted exchange rate of the rupee bears out a very close relationship with the CPI and the GDP deflator as well. Past BoM studies have shown that the impact of a depreciation of the rupee on the rate of inflation is heaviest in the short-term (3-6 months). In the forecasting technique adopted by the BoM in the past, the ARIMA model (Auto Regressive Integrated Moving Average), two regular shocks to inflation rate in Mauritius used to stand out: upward revisions in the domestic price of petroleum products and depreciation of the rupee. Given the specificities of the Mauritian economy, these characteristics have remained unchanged.

On a trade-weighted basis, the rupee depreciated by not less than 13 per cent in 2020. Freight cost had shot up. These were the cost-push forces that were not and could not be nullified. Repeated buying sprees during lockdowns had caused prices of consumer goods to shoot up. These were demand-push forces. Concurrently, the economy suffered strong supply shocks that caused shortages. By and large, these were a strong cocktail for out-of-control price inflation. One would have rightly expected the rate of inflation and the GDP deflator to be exceptionally high for 2020. True, it could also be argued that there was an overall demand contraction during 2020 as a result of which the rate of inflation rate did not rise. This is quite a red herring. The contraction was not so much for goods falling in the CPI basket; it was mostly for semi-luxury and luxury goods and services.

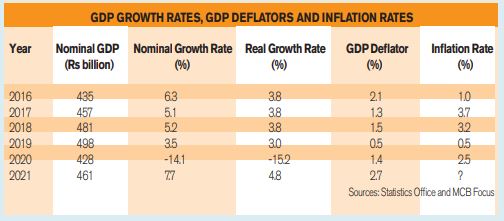

Against commons sense, as shown in the accompanying table, both the inflation rate and the GDP deflator did not behave abnormally; they remained surprisingly as low as in the previous years.

In the years prior to 2015, the rupee was strong. A sense of fiscal discipline prevailed. Monetary policies were not as loose as they have been since 2019. There were no supply shocks. Yet, both the rates of inflation and the GDP deflators were higher than in the years after 2014. Generally, the rates of inflation in Mauritius are between 2-2.5 percentage points higher than the trade-weighted inflation rates of its major trading partner countries. This is an established fact. Indeed, the rates of inflation in Mauritius were higher before 2014 but not thereafter.

My worksheets show that the rate of inflation for 2020 was at least 10 per cent; the 2.5 per cent official rate is grossly understated. The GDP deflator also was substantially higher at not less than 5 per cent. It goes to say that the economic contraction was substantially higher at 18 per cent. A smaller GDP deflator overstates the growth rate of the GDP. Conversely, a bigger GDP deflator yields a lower GDP growth rate. Since the rupee has continued to depreciate, one should expect the GDP deflator to be higher than 2.7 per cent for 2021. The growth rate for 2021 is, thus, most likely to be quite less than 4.8 per cent. By the first quarter of 2022, the growth rate will most likely be scaled down to below 4 per cent. A lower base for 2020-21 will give a higher growth rate for 2021-22. Isn’t it? The thinner surface of our macro-economic data looks glossy. Dig deeper into them. The scums pop out.

Question: Is the projection of 9 per cent growth rate for 2021-22 realistic? Of course, it is commendable to aim high. A week ago, I, too, had asked myself if it was realistic. One can only surmise how the 9 per cent growth rate may have been arrived at. Clearly, the Hon Minister of Finance is banking heavily on the tourism industry to prop up growth. A 9 per cent growth rate would require an additional aggregate amount of about Rs40 billion (in real terms, that is, appropriately adjusted by GDP deflator) in value-added in the economy. 1,300 million tourists bring in over Rs60 billion annually to the country. Half of the number, a phantasmagorical figure or rather an insufferable optical illusion, would generate Rs30 billion and more through income multiplier effect. Other sectors would bring in the balance. It sounds overly simplistic. Schoolboy arithmetic. No wonder all growth projections in recent years have been scaled down again and again in the course of the years. Frequent scaling down of projections and forecasts reflects poorly on the Government and the forecasters. My take: the 9 per cent growth projection for 2021-2022 is totally unrealistic, more so with a national carrier in a comatose state, airlines worldwide fraught with troubles and travel restrictions. All other sources of growth are unplugged. A realistic GDP deflator would depress growth to very far below 9 per cent.

In the years -1979 to 1986 - Mauritius has had stand-by Arrangements with the IMF. The BoM and the Ministry of Finance used to press the IMF for realistic quarterly performance criteria. Every quarter, we used to outperform and pleasantly surprise economists responsible for the Mauritian desk at the IMF. We were viewed as serious and fully committed people. Mauritius gained in terms of credibility and won the trusts of the IMF, World Bank and foreign investors. We subsequently attained international distinction. We won the respects in the marketplace. Wise people set goals that are realistic. There are lessons we learn from experience; we do not get them from the ATMs.

Publicité

Publicité

Les plus récents