Publicité

The Mauritian economy today is more a Dodo…

Par

Partager cet article

The Mauritian economy today is more a Dodo…

An Open Letter to the Governor of the Bank of Mauritius

Dear Governor The macro economic narrative changed considerably this year: from a transitory inflation shock to runaway inflation that is only now beginning to cool off, from supporting growth and unemployment to fighting inflation, from liquidity injections to central bank balance sheet reductions and the end of the era of easy money. As a result, financial markets have reacted sharply to this regime shift, affecting returns, correlations and dispersions across and within asset classes. Major economies are already in recession as central banks continue to tighten monetary policy in a belated attempt to regain lost credibility and re-anchor inflation expectations. The shift to a less rosy economic regime will be profound and will lead to shorter and more volatile business cycles. As global economic activity as measured by high frequency GDP growth nowcasts continues to slow at a worrying pace, inflation too is cooling off. From falling commodity prices to falling shipping costs, inflation is trending down and will provide some relief to central banks in the latter half of 2023.

However, there are various secular trends at play as the world rolls past peak globalization which will keep both inflation and rates high enough for longer. Large debt ratios of corporations, consumers and governments just in the western world are at close to 300% of global GDP. As rates rise and stay there and as debt servicing costs increase, many zombie companies, zombie households and zombie like economies will struggle. Mauritian policy makers like to sell Goldilocks scenarios to the people but the problem today is that we are beginning to be fooled by our own spin.

The Mauritian economy today is more a Dodo than what the Finance Minister described as some kind of rising phoenix. The Government continues to engage in unsustainable populist spending despite rising debt servicing costs and public debt amounting to more than 90% of GDP. Inflation remains in the double digits and will only cool off to a still too high 5% to 6% in late 2023 with upside risks to this outlook. Unemployment remains high and more than 32% of the labor force remains inactive, unemployed or underemployed. The economy is simply not creating enough high paying jobs. In a more competitive, digitized and uncertain global economic landscape, the quality of education locally has continued to decline and the outlook for a sea change in education outcomes remains dim.

One of the few rising pillars of the economy has sadly been that of the illicit economy with annual hard drug consumption likely now well above MUR 20 Billion. Mauritian exports may bounce back by MUR 80 Billion this year but imports have risen even more strongly. The current account deficit is expected to stand at a whopping 14% of GDP this year. Persistent current account deficits continue to point to a fundamental overvaluation of the Mauritian Rupee vis-à-vis the currencies of its major trading partners. The global business sector remains largely stuck in back office accounting land, large segments of the private sector remain rent seeking, foreign direct investment remains too real estate focused despite its very low multiplier effect on growth and the Government seems to be very allergic to engaging in meaningful and overdue structural reforms.

Unless the Government engages in a meaningful fiscal consolidation path and adopts a more sustainable debt strategy that relies much less on inflation and unless the economic competitiveness of the economy is enhanced, there is little that the central bank can do on the foreign exchange front over time.

Impossible trinity

Simply put, the current foreign exchange intervention strategy in the context of what has been highlighted above is not sustainable. The impossible trinity when it comes to monetary policy means that a central bank can only achieve any two of the three objectives: independent monetary policy, open capital flows and exchange rate targeting but not all three at the same time. This is why the Bank of Mauritius (BoM) has attempted to partly curtail demand by rationing access to foreign currency. Gross international reserves may currently stand at close to MUR 279.8 Billion but stood at more than MUR 372 Billion back in December 2021.

Furthermore, the MUR 279.8 Billion number includes more than MUR 52 Billion in central bank contracted foreign borrowings while another MUR 35 Billion belongs to commercial banks which park their funds at the BoM for liquidity management purposes. Subtract these funds and that leaves the BoM with less than MUR 193 Billion net. Out of the MUR 193 Billion of ammunition, the BoM has some MUR 111 Billion of investments accounted for at fair value through P&L which is where a fair share of the unrealized comprehensive losses are coming from. Unless the BoM plans to realize these losses which would be very bad market timing or sell or swap its gold holdings valued at MUR 29 Billion for USD cash, this leaves the central bank with less than MUR 82.5 Billion – MUR 29 Billion or merely some MUR 59 Billion in liquid dry powder which is not high when one considers the size of the trade deficit and a tough global context to come in 2023.

Of course, the BoM can pledge more of its investments as collateral and borrow more from abroad but this is not sustainable. On balance sheet foreign borrowings contracted by the central bank which barely existed just two years ago already accounted for 18.3% of gross international reserves as at the 11th of November 2022 and this percentage is likely to rise further in the near term given the pace of interventions. International reserves are meant to act as a tail risk insurance policy for the country and while we can all hope for the best when it comes to a soft landing of the global economy, this is not sound macro policy making especially when we consider the rising size of external debt, the size of GBC deposits and imports. There is no point in maintaining an artificial level of the Rupee where supply does not meet demand for long.

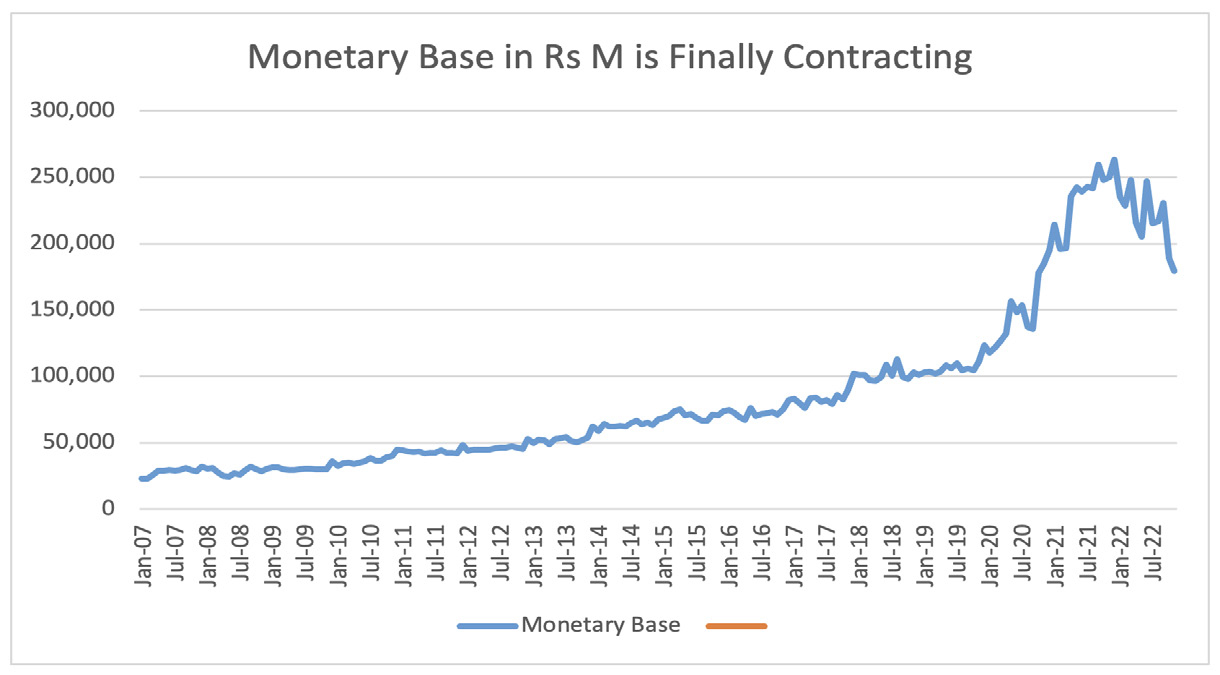

The BoM should only intervene to smooth foreign exchange volatility but not fight against the current of fundamentals. Foreign exchange sales may have allowed the central bank to contract its balance sheet along with the level of the monetary base which has helped to reduce the level of excess Rupee liquidity in the monetary system to MUR 12.8 Billion on the 17th of November 2022 compared to more than MUR 34 Billion in June, reduce the gap between the repo rate and short term treasury and interbank rates but this is unfortunately not sustainable. The diffrential between US 3 month T Bills currently yielding 4.29% and its Mauritian equivalent at 2.80% remains high.

The Government is not a spectator here and should fix the economy rather than being spun around by its own spin of a rising phoenix especially when the 6%-7% growth number is base effect driven.

While many observers have claimed that the central bank would go broke in recent days following the publication of the October central bank balance sheet, a central bank cannot default on its domestic liabilities. The rise in foreign borrowings is however a growing risk factor. The key focus for the BoM should be to bring about price and financial stability over the medium term. There are a handful of central banks such as the Bank of Israel, the Central Bank of Chile and the Czech National Bank which have operated with negative equity for years and have achieved their clearly defined monetary policy objectives. The challenge for a central bank with negative equity is that it may face significant credibility challenges in meeting its monetary policy objectives if a growing share of the monetary base is accounted for by money printing to fund liabilities.

Central banks are only able to achieve their objectives by properly anchoring market expectations and perceptions. This is why the vast majority of central banks prefer to ensure that they have a level of economic capital that is adequate in order to cover all their balance sheet risks. The Reserve Bank of India has an economic capital to total assets ratio of more than 22% in order to absorb all tail risks measured at the 99.9% confidence level. The RBI also has a clearly defined flexible inflation target, a less fragmented bond market and short term money market rates are very closely aligned to its policy rate unlike with the BoM. The Reserve Bank of India can effectively align short term market rates to its policy rate precisely because it has a strong balance sheet, something the Bank of Mauritius does not have. The RBI had also instituted the Bimal Jalan Committee in order to conduct a proper quantitative study on the required level of economic capital prior to the RBI Board making any transfers to the Government of India back in 2019. Central banks only ever transfer excess reserves to the Government.

In the case of the BoM, the Board transferred most of the economic capital of the BoM to the Government via the printing press given that these were unrealized FX valuation gains in two separate occasions including an initial MUR 18 Billion transfer well before the Covid-19 virus ever left Wuhan. Whether the Board conducted any quantitative study of its balance sheet prior to any transfer is a legitimate question especially when the market has a strong perception of fiscal dominance over the central bank.

Market volatility

When it comes to market volatility being one of the key causes of the current large MUR 11 Billion comprehensive loss, this is why central banks have such capital buffers for. Furthermore, while it is not unusual for central banks to outsource part of the management of their international assets to fund managers, these central banks still need to actively manage the entire portfolio and risk factors need to be measured and dynamically rebalanced via overlays according to a clearly defined risk budget/benchmark especially given the weak economic capital position of the BoM.

The BoM needs to urgently seek expertise from the IMF and the Bank for International Settlements and institute an independent expert committee in order to determine the required level of economic capital which takes all risks including MIC investment related credit, valuation and interest rate risks into account. This report should be made public just as was the case with the RBI’s Jalan report. The BoM should then formally request recapitalization spread over a 3-5 year period with the Government for example returning unspent special funds money to the central bank.

MIC assets should be independently revalued and a Government funded and leveraged special purpose vehicle should be created post revaluation in order to offload MIC assets. Local banks which largely indirectly benefited from generous MIC private sector bailouts should be called to share part of the risk as should have been the case initially. The BoM could purchase some of the SPV issued debt in the secondary bond market as well. The BoM should finally and formally establish a flexible inflation target regime with a target band of between 3% and 4.5% that it would be accountable for over an 18 month period using year on year inflation as the metric. Inflation in Mauritius is no longer just externally driven with core inflation which excludes such prices peaking at 7.5% and with 5 year ahead inflation expectations already at 5.9%.

There is a growing asset management industry in Mauritius and there is no need for the BoM to be issuing all types of savings bonds which negatively impact on its margins and duration profile of its liabilities. In order to reduce the cost of conducting open market operations in the form of monetary policy instruments, the central bank can consider to implement a reverse tiering framework on a new type of deposit facility which would only compensate banks on funds held at the BoM above a threshold. Finally, the BoM Act should be strengthened in order to ensure stronger central bank independence.

Governor, the Government and country need to realize that we must become more ant than grasshopper. We may be counting a lot on the Diego Garcia lease but the world is not out to help us. Modern monetary theory will not work well in a small economy that imports most of what it consumes and such theories are constrained by the current inflation regime. There is no long term trade off between low and stable prices and growth. This is what the central bank of the country should focus on.

Publicité

Publicité

Les plus récents