Publicité

Government spending

Faster to disaster

Par

Partager cet article

Government spending

Faster to disaster

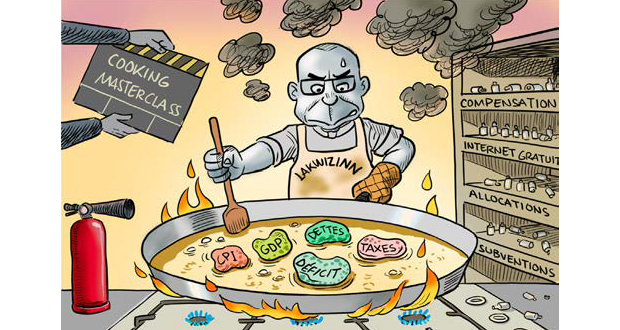

The latest publication of Govt deficit and debt data discloses new and worrying information on the lack of fiscal consolidation, which along with more post-budget social spending measures, spells a further worsening of economic prospects. Growing concerns about the country’s vulnerabilities call for another note of warning and for corrective action on excessive Govt spending.

Fake data

The recent budget, presented in June 24, provided an overly optimistic estimate of Govt revenue for the year 23-24, significantly higher than the actual figure released by Statistics Mauritius last week. The revenue shortfall amounts to Rs14 bn, mainly on taxes. This large margin of error in estimating revenue for 23-24, only one month before the fiscal year end, clearly points to data manipulation.

The budget also projected a decrease in the overall deficit to 3.9% of GDP in 23-24 from 4.8% in the previous year. However, the actual data now shows a wider budget deficit of 5.4% of GDP in 23-24, higher than in the previous year, and similar to two years ago (see Table). Inclusive of heavy net spending by special funds (SF), mainly on social housing, the budget deficit has risen sharply to around 8% of GDP in 23-24.

A larger fiscal deficit implies higher public debt. Public Sector Debt in June 24 stood at Rs546 bn, or Rs22 bn higher than the recent budget estimate of Rs524 bn. Public debt represented 78% of GDP in June 24, or 3 % points higher than the recent budget estimate of 75%. As with Govt revenue, debt data in the recent budget was fudged to artificially reduce the public debt ratio.

The budgeted amount of Govt revenue for the current fiscal year 24-25 is also grossly overestimated by inflating tax receipts. Tax revenue in 24-25 is budgeted at Rs182 bn, at a record high of 23% of GDP, whereas taxes in 23-24 stood at Rs141 bn, or only 20% of GDP. Allowing for the introduction of the CCR levy and improved tax collection, a realistic tax-to-GDP ratio would be around 21% in 24-25. Taxes in 24-25 would then amount to Rs168 bn, lower than budgeted by about Rs14 bn.

Adjusted revenue in 24-25 would also reflect a shortfall of Rs14 bn, as in 23-24. The adjusted deficit in 24-25 would be Rs 14 bn higher, reaching 5.2 % of GDP, about the same as in the previous year. It is assumed that Govt spending will not be affected by the impact of post-budget wage increases and other measures, due to offsetting expenditure savings.

The evolution of the fiscal balance does not reflect fiscal consolidation, i.e., a reduction of the budget deficit, at least relative to GDP. Instead, fiscal data was doctored in the recent budget to support a false claim of fiscal consolidation and debt reduction.

Fiscal consolidation

Fiscal consolidation is not realizable without a review of social spending policies. Pension and other social benefits have risen fourfold from Rs19 bn in 2014 to Rs77 bn in 24-25, increasing from one fifth to a third of total Govt expenditures, and almost doubling from 4.9% to 9.7% of GDP. Unaffordable social largesse over a decade has contributed significantly to the deterioration in fiscal deficits and debt, which are currently much higher than before the Covid pandemic, despite massive central bank money printing.

Moody’s downgraded Mauritius in July 22 to borderline investment grade, mainly because of elevated debt higher than peer countries. Moody’s affirmation of the country’s sovereign rating in July 2024 is notably based on its “expectations of a further reduction in the debt burden”. Moody’s also cautioned that “A reversal or slowdown of fiscal consolidation which results in Govt debt stabilizing at higher levels than currently anticipated would put downward pressure on the rating”.

Large budget deficits running above 5% of GDP, and higher than anticipated Govt debt ratios, contradict any pretence of ongoing fiscal consolidation and debt reduction. Consequently, there is a growing risk of an adverse assessment of the country’s creditworthiness, which could cause severe harm to banking and financial stability.

Fiscal deficit and debt ratios have not shown much improvement despite the allegedly high GDP growth rates recorded since 2022. Statistics Mauritius reports strong GDP growth rates, based however on a questionable inclusion of offshore primary income in domestic income.

Our medium-term growth potential is estimated at only around 3.5 % annually, equivalent to the average annual GDP growth rate from 2013 to 2019. Achieving high and sustained economic growth with an ageing and declining population requires more substantial productivity gains.

Conclusion

The country faces serious difficulties stemming from large fiscal deficits and high public debt, external imbalances and chronic forex scarcity, continued rupee depreciation, and looming inflationary pressures. The Mauritian ship is sailing faster towards Sri Lanka, sped forward by Govt’s reckless electoral spending spree.

The current fiscal stance is not sustainable and faking fiscal and GDP data will not get us out of troubled waters. A rating downgrade, or any other sudden and unexpected shocks, could precipitate large capital outflows and a forex crisis, sending the economy into a tailspin.

Publicité

Publicité

Les plus récents