Publicité

GDP Overestimation

The June 2022 issue of the Economic and Social Indicators published by Statistics Mauritius (SM) made significant revisions to the National Accounts from 2018 to 2021. Annual Gross domestic product (GDP) at current market prices for the period 2018 to 2021 was revised upwards by an average of Rs17 bn, or 3.6%, reflected largely by an adjustment to increase exports of services.

The September 2023 issue of the same publication produced another major revision, raising forecast real GDP growth in 2023 to 6.8% from an expected figure of 5.3% three months earlier, mainly on account of higher public sector investment. A closer examination of these two GDP revisions suggests that GDP data is subject to overestimation by SM.

GDP revision - June 22

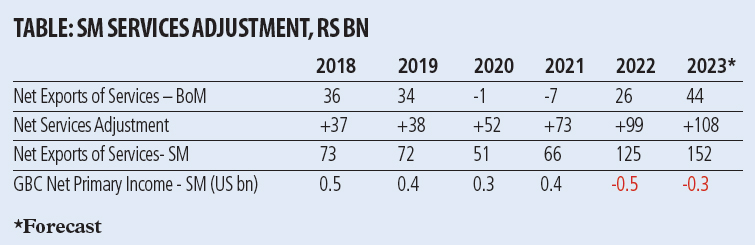

In the June 23 GDP revision, consumption, investments and net imports of goods, were the least affected among the main GDP components. The bulk of the GDP revision was reflected in an increase in net exports of services. For example, net exports of services in 2021 were reduced from a deficit of Rs7 bn to a surplus of Rs66 bn, by an addition of Rs73 bn to the services account. As stated by SM, net exports of goods and services are revised by “the inclusion of Global Business Company (GBC) services in exports of services”, owing to a reallocation from primary income of GBCs to services exports.

Primary income is an item in the balance of payments which mainly consists of income earned by GBCs on their external investments. Balance of payments statistics on exports of goods and services, and on primary income, are produced by the Bank of Mauritius (BoM). Since the GDP revision last year, SM reduces the BoM’s net primary income data on account of certain GBC activities, and the excluded primary income is instead added to net exports of services in the presentation of the national accounts.

SM also makes a much smaller adjustment from primary income to services in order to account for Fisim, or financial intermediation services indirectly measured. The Fisim adjustment relates to the financial margin earned by banks on their external business activities, and amounted to only about Rs4 bn in 2021.

The SM services adjustment for GBCs is entirely justified when domestic companies, like asset management and insurance companies, hold their foreign investments through GBCs. It has also helped to address the substantial discrepancies between the production and expenditure measures of GDP. Some GBC activities can indeed be considered as part of the domestic economy, but the scale of the adjustment from primary income to services appears excessive, especially in the last few years.

As shown in the table below, the services adjustment rises to reach close to Rs100 bn in 2022. Net exports of services, including the services adjustment, double in 2022 and are forecast to increase further in 2023. Net primary income of GBCs, excluding the services adjustment and expressed in USD to eliminate the valuation effect of rupee depreciation, remained stable and positive until 2021. But, then reversed into outflows of USD0.5 bn in 2022, and of USD0.3 bn in the 2023 forecast.

The negative primary income performance by GBCs is at variance with SM’s own real growth estimates for the global business sector, of 3.3% in 2022, and a 4.4% forecast for 2023. This inconsistency raises serious doubts regarding the reliability of the SM services adjustment in boosting GDP data for 2022 and 2023.

If SM is right in its revised quantification of GBC activities, then BoM balance of payments statistics must be deficient. The likelihood of official GDP overstatement by adjusting services exports warrants due consideration.

GDP revision - Sept 23

SM is overestimating GDP for 2023 by an unrealistic forecast of public sector investment. In its June 23 forecast, SM stated that GDP would grow by 5.3% in 2023 “on the basis of policy measures announced in the Budget Speech 2023/2024, particularly those relating to public sector investment projects”. SM also forecast that public investment would expand by 11.9% in real terms compared to 1.1% in 2022, based on “latest available information on ongoing and new projects, including those announced in the Public Sector Investment Programme 2023/2024”.

Not more than three months later, in Sept 2023, SM revised its GDP and public investment growth projections for 2023 markedly upwards. SM forecast that GDP would now grow by 6.8% instead of 5.3% in 2023, “based on new information gathered on key sectors of the economy”, and that public sector investment would grow by 40.9% in real terms instead of 11.9%. Following a revised and improved forecast of Rs6 bn, public investment would reach Rs33 bn in 2023, up from an actual figure of Rs23 bn in 2022.

The rationale provided by SM for a substantial increase of Rs10 bn in public investment between 2022 and 2023 rests solely on the words “new information”. Public investment in the first half of 2023 is estimated at13 bn, and SM is expecting higher public investment of Rs20 bn in the second half of 2023. Such a massive investment boost in just 6 months, almost as much as the entire year 2022, is fanciful, given the usual project implementation challenges. While social housing projects are progressing fairly well, the Metro Express extension is bogged down in legal troubles in India.

On the strength of magnified investments, SM anticipates the construction sector to grow at a faster rate of 28.6% in real terms in 2023, compared to the earlier estimate of 9.8%, contributing an additional one percentage point to GDP growth. The expected surge in investment and construction activities in 2023 is evidently excessive, and GDP growth in 2023 is likely to turn out closer to the previous forecast of 5.3% than 6.8%.

SM Status

SM is recognized for its track record of high integrity in the production of national statistics. However, recent events have raised some apprehensions about maintaining SM’s reputation for reliability. In July 2021, SM released two different GDP forecasts within the span of a few days, which led to the resignation of the Chairman of the Statistical Board, followed by the departure of the Director of Statistics. And, it is unbecoming for an important institution like SM that its current Director should remain in an acting capacity for more than two years.

The latest IMF Report on Mauritius also observed that “Continued efforts are necessary to safeguard independence of Statistics Mauritius in its estimations of economic developments and outlook”. On a positive note, however, SM maintained its GDP forecast for fiscal year 2022-23, even after Govt fabricated a higher GDP estimate to show an artificial decrease in the debt to GDP ratio at June 2022 to below 80%.

There is hope that SM’s independence and credibility can be fully restored, without any lingering doubts about cooking of numbers in the Government kitchen. SM should dispel any uncertainty about GDP estimation for 2023, by clarifying the issues relating to services adjustment and public investment.

Conclusion

It is well established that the manipulation of official statistics is common to authoritarian regimes. In an article dated 29 Sep 22, the Economist magazine showed that average reported economic growth in autocracies between 2002 and 2021 has been twice as fast as in democracies. Dictatorial and unpopular Governments have a strong incentive to show healthy growth to stay in power.

Evidence of GDP manipulation reflects a weakening independence of political and economic institutions and a growing bias in the separation of powers towards the Executive. In a strong democracy, those who fiddle with official figures would be subject to investigation and prosecution.

Publicité

Publicité

Les plus récents