Publicité

Analysis: Bis repetita !

Par

Partager cet article

Analysis: Bis repetita !

In the foreword to the 2018 Edition of Top Hundred Companies, the author reviews the economic landscape and stresses the need for the government to take bold, hard and challenging decisions so that the country can progress to high income status.

Last year, our piece in this very publication was entitled «LIFT OFF… or TROUBLE». This year, the title could have been just the same in many ways.

After all, the world economic background is better and improving with the IMF assessing that global GDP picked up from 3.2% in 2016 to 3.8% in 2017, projecting rates of 3.9% for both 2018 and 2019. That is our level of growth this year, that is! Are we just average, then?

In particular, the emerging market and developing economy sub set of the world economy (sparked forward by the economies of India and China) will have seen growth rates of 4.4% in 2016, graduate to 4.8% in 2017 and they are expected to level off at 4.9% in both 2018 and 2019.

Meanwhile, our economy is still battling, undershooting targets and promises. The 5.3% growth rate dangled appetisingly in front of our eyes in this government’s first Budget is still nowhere to be seen and last year’s revised forecast of 4.1% growth for 2017/18 is now estimated to be 3.9%. (Budget Supplement 2018/19).

It is of great comfort to remind ourselves, though, that the last recession known to Mauritius, through an actual reduction of GDP, dates back to… 38 years ago! Amongst the other favourable metrics of our economy, one may cite a declining unemployment rate (though our total activity rate was still stuck at a lowish 59.6%), a satisfactory debt profile, in that 83% of our debt is actually denominated in rupees, whilst between December 2010 and now, the maturity profile thereof has actually lengthened by 1.9 year on average. Moreover, there is very little interest rate risk since more than 95% of our domestic debt is at a fixed rate. This implies that government is not overly exposed to any devaluations, especially as we still hold a healthy overall balance of payments of 6.2% of GDP in 2017.

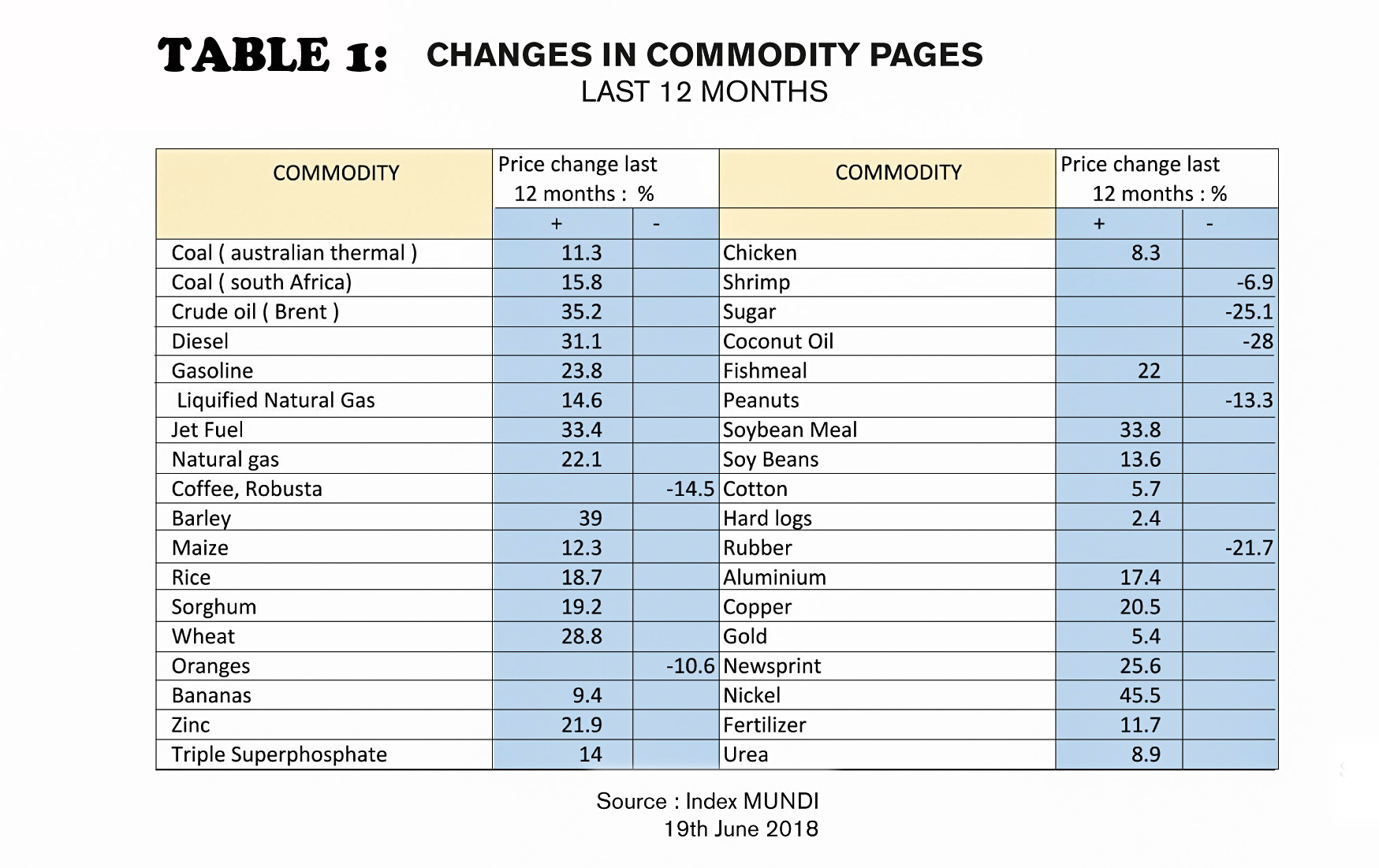

And that is precisely where we start to worry again, in that this balance of payments surplus (which fuels the foreign exchange reserves we are so proud of, as well as the surplus liquidity within the system, which is surely more problematic…) is largely fed by GBC net capital inflows of about Rs 69 Bn and FDI into property which totalled Rs 8.8 Bn in 2017, thus countervailing the horribly high and worsening balance of trade deficit that we keep posting from one year to the next (Rs 100 Bn + by now), with little action being taken (namely on productivity) to emerge from the situation. Indeed, the trade deficit outcome, at 21.6% of GDP, is a full 1% more than forecasted last year. It may now worsen yet further with commodity prices increasing strongly in general over the last 12 months, except for some lightweights like coffee beans, oranges, coconut oil, groundnuts, copra, rubber and… sugar ! (Table I). Topping the charts of our worries: fuel prices, of course, and these recently hiked prices will now impact 2018 for a full year, the price of a barrel of crude climbing inexorably from some 50 dollars to the current 75 dollars (+50%), with no solace in view on the horizon…

At current account level, services and invisibles do not find it possible to claw the just-toolarge trade deficit of over Rs 100 Bn back, thus leaving a severe 6.6% deficit to GDP. Let us also note that the current account deficit of Rs 30 Bn in 2017 is arrived at after benefiting from further GBC inflows of 22 Bn…

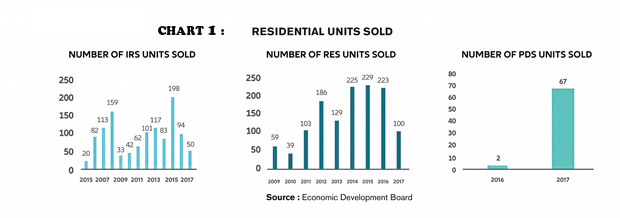

Our challenge does not quite resemble that faced during the Asian crisis of 1997-98, for there is far less short-term ‘hot’ foreign money sloshing around in the Stock Exchange or in short-term government paper and most of the FDI that comes in is for real, tangible investment. Our cause for worry lies essentially in the mechanics of our global business unravelling because of unfavourable local conditions, like the changes coming in the Finance Act, for example, and/or, perhaps more pressing, the main component of current FDI, i.e. property, faltering without being replaced (see chart I). In the first case, we would be risking the billions accruing yearly to the country’s balance of payments through the Global sector’s portfolio investment income and, in the second, we certainly need to nurture and sustain the close to Rs 9 Bn moving in on PDS dreams. Or find ways to replace the latter… Both are at risk if we keep deteriorating the image of the country with a messy soup of politically unsavoury “affairs”, too many economic compromises (like SPVs for parking debt), an unpredictable future and a systematic lack of political courage in sorting out the more difficult issues facing the country (Pension Fund reform, 24/7 water and how to finance that objective, productivity enhancing measures including strict meritocracy, a more targeted welfare state, a reformed Landlord & Tenant Act, etc.) especially when all smothered in a degraded socio-cultural concoction made up of, in no particular order of importance, stray dogs, drug consumption, littering – both petty and gross –, law & order issues, unprotected and therefore unrwedeemed lagoons, aesthetically unpleasant architecture, an uncouth capital city (except at night), dangerous driving and the like.

These just simply do NOT match the image of “paradise”… and must be therefore put right! Fast! Otherwise, we may shoo away the foreigners we need to woo both as tourists, as investors and as residents, be they nationals or not. We are so very dependent on them, now!

As to government’s Budget, the situation looks under control at a 3.5% deficit, but one should not underestimate the fact that the recurrent budget deficit fuelled by accelerated social spending is on an upward trend, moving from 0.4% in 2014/15 to 1.9% in 2016/17, thus crucially crowding out capital budget needs. Indeed, the satisfactory budget deficits of the past years have largely been due to capital budget underspending. Should our capacity to spend our capital budget according to targets actually improve (and the stated ambitions are indeed huge!), our overall budget deficit will face the hit, especially if we stop evading reality by using SPVs to go “off balance sheet”.

Investment to GDP, which was to be massaged upwards to 25% in 2018, is still stolidly stuck at 17.3% in 2017. Not a pretty sight!

Amongst the other challenges of the country: the fate o f productive industry and more especially exporting components thereof. Sugar faces a real cliff hanger with international market prices covering just below 60% of total production costs and sugar acreage fast reducing. Choices need to be made fast: no change and the industry goes over the cliff, which is, of course, a kind of choice, but of the slipshod kind! Manufacturing, in spite of the expressed wishes of the Vision 2030 plan, is on a sliding slope as a percentage of GDP (from 15.5% in 2007 to 11.7% in 2017), even though output per employee improved by close to 60% in nominal terms over the same period. This must mean our competitors are doing even better?! Textile production has regressed since 2014 and 2,000 jobs have been lost therein. Fortunately, while coastal fish catch decreased further by 2.6%, total fish production, mostly driven by tuna exports, grew by a full 36% year on year. Let us hope that fish stocks remain plentiful, though, for this is basically a plucking industry… and in open seas, we are not the only ones plucking!

Tourism registered a good year with 1.4 million tourists expected in 2018, though we are now seeing the first signs of local resistance to further growth and profitability still trails the glorious 1990 years (also, see below). The financial services sector is surmised to maintain a growth rate of 5.5% going forward, leading all the growing sectors, bar construction (+7.5%) whose output per man hour, however, remains challenging, especially when set against foreign competition. The so-called Ocean Economy, now credited with a gross value added of Rs 44 Bn (Three-Year Strategic Plan, page 41) reaches this staggering contribution, not by doing much that is new, but by simply laying claim to and roping in… Hotels & Restaurants, Port activities, Seafood, Leisure boat activities, Freeport, Bunkering and Ship building! Now only do we realise why minister Koonjoo does not look at all deflated and why minister Lutchmeenaraidoo even recently partook into his pride and joy! Not Gayan, though…

Nevertheless, one of the most important achievements of this government must surely be the reduction of the percentage of households living in relative poverty, from 9.4% in 2012 to 5.5% in 2017, improving the GINI coefficient, if marginally, along the way. The reduction of the income tax rate for middle-income taxpayers will further help galvanise this trend. However, there is a cost to all this generosity, especially if GDP targets keep not being met: for as social costs progress too fast, they do crowd out capital expenditure and/or will fuel the growing budget deficit of future years! Rude awakenings ahead?

Against this background, the Top 100 figures look quite good with consolidated turnover progressing to close to Rs 400 Bn, a jump of 6.5%, year on year. Leading the way in this meaningful surge ahead were a revived Mammouth (+149% to Rs 1.524 Bn), Cargo Handling Corporation (+52% to Rs 3.25 Bn) Rehm-Grinaker (+42% to Rs 1.963 Bn), Engen (+42% also to Rs 7.25 Bn) and CFAO Motors (+36% to Rs 2.298 Bn), which, like Mammouth, reactivated businesses last possessed by BAI group.

The companies having made the greatest headway profitability- wise were Airports of Mauritius (+Rs 1.48 Bn), New Mauritius Hotels (+Rs 918 million), Standard Chartered Bank (+Rs 612 million), Alteo group (+ Rs 548 million) and IBL (+Rs 477 million) and the Top 5 in terms of profitability as a percentage of turnover (banks excepted) were the Mauritius Civil Service Mutual Aid Association with an astounding 49.30% followed by Airports of Mauritius (30.76%), Mauritius Freeport Development (30.47%), CIM group (25.16%) and Ajanta Pharma (22.09%), the top 4 being very capital-intensive operations.

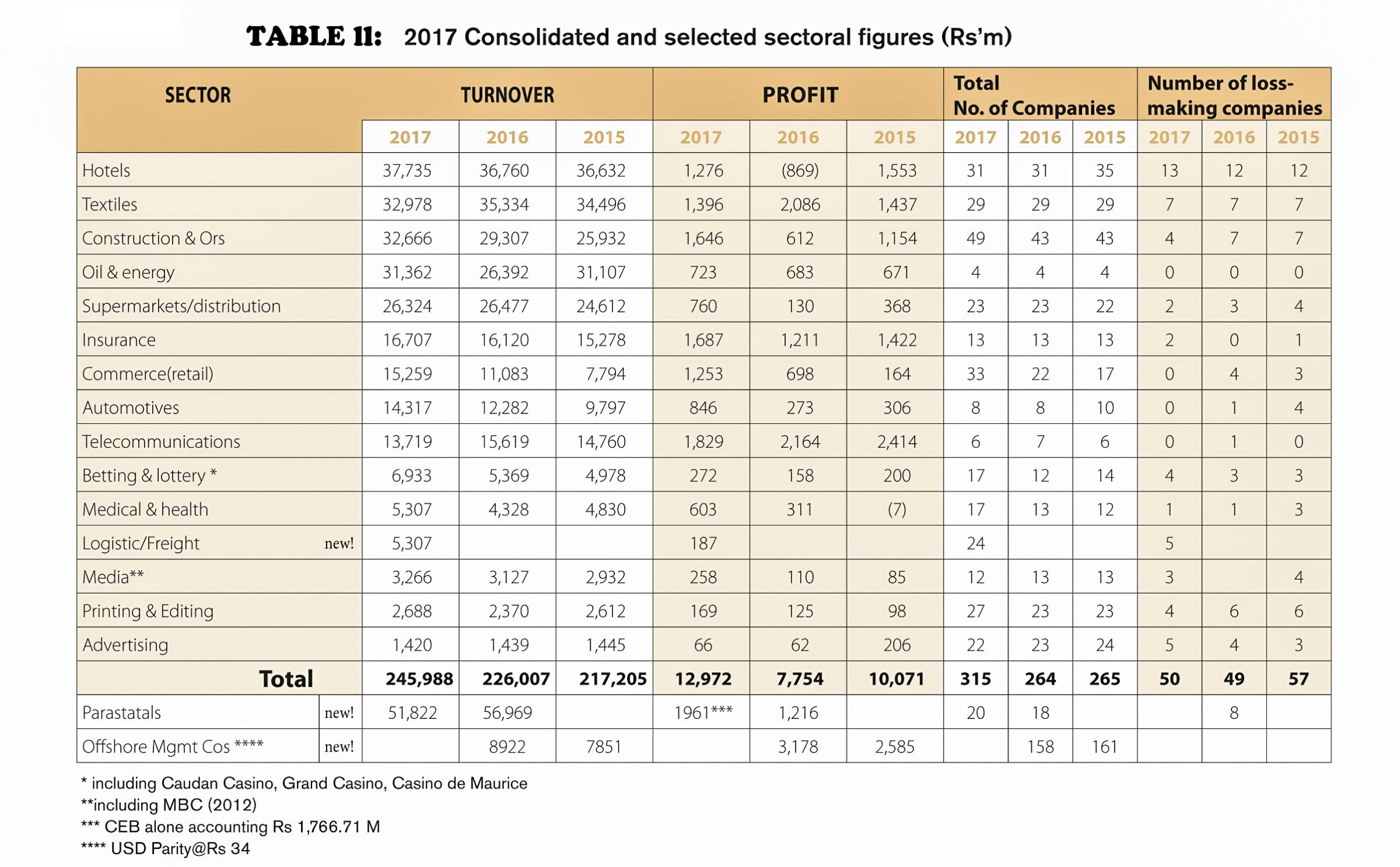

Table II, illustrating sectoral trends through a wider set of local companies, 315 of them all told, net of corporates, Air Mauritius and banks, tells the same story of growth in turwnover (+ 9.8%) and profitability (+68% off the back of a particularly weak 2017 set of results). Consolidated Profit as a percentage of turnover thus matures from 4.6% in 2016 and 3.4 % in 2017 to 5.3% this year, fed by the Automotive sector (profit up by 3 times), supermarkets & distribution (profits up by almost 6 times), hotels (a positive swing of over Rs 2 Bn) and construction (Profits up by almost 3 times). It is noteworthy that these 4 sectors had a particularly poor 2017 record, profitability wise.

What may be particularly worrying, short of detailed forensics, is to see a major drop in the textiles sector profit, by almost a third, with fully a quarter of the sample surveyed showing losses. Maybe even more worrying in a context where the settled impression locally is that the hotel sector is “doing well” is that 13 out of the 31 strong sample (i.e. 41%) are still making losses and not always because of major refurbishment and close-downs!

In a context of the Double Taxation Avoidance Agreement with India coming to a fundamental turning point, the latest figures from FSC still, unfortunately, only date back to calendar year 2016 or the 18-months period to 30th June 2017, which is a pity, but these figures nevertheless show that the issue of GBC1 and GBC2 licences still continued unabated at the rate of some 1,300 and 1,100 annually.

The figures presented in Table II relate to the Management Companies operating within the offshore sector and still look healthy enough. The crunch however will come in March 2019 when even the 50% benefit from capital gains tax exemption will be terminated. By then, GBC2 companies will be off our product menu, replaced by passports!

The Banking sector, in the spitting image of its top 4 banks, did not see its results progress by much (Total assets: +5% and Profit: +4.2%). AfrAsia perked up after a bad year (+23% on profit) and Standard Chartered almost quadrupled its profit even though it logged reduced end-of-year assets. Amongst insurers, Mauritius Union clawed back its way after a poor 2016 and SICOM remained the most profitable operation as a percentage of turnover. The accounts of the company currently housing the ex-BAI’s portfolio, the National Insurance Corporation, though licensed since 2015, are still not available and are still being debated about, which is beginning to cause real concern. In the Automotive sector, the figures for Toyota were particularly impressive. In a supermarket category which largely improved its results, only Shoprite posted a loss, which is no surprise, and Seven Seven Co Ltd still had the lowest profitability ratio as the least mature of the group. Sectoral profitability as a percentage of turnover is highest for the telecommunications sector (+13.3%), Medical & Health (+11.4%, largely powered by Ajanta Pharma and Proximed) and insurance (+10.1%).

The 2017/2018 Budget had a long list of social and economic initiatives that will probably create some measure of a feel-good factor and indeed some results for some time. The real medium-term and long-term challenges, however, remain and are not being dealt with. For how long this exercise of kicking the can down the road is possible is anybody’s guess, but the lack of political courage to tackle the fundamentals will, before long, be put to the test and either generate a Macron… or, God forbid, a Trump! Hopefully before we end up in financial trouble.

It remains the firm conviction of the author that this country will only progress further, including to high income status, if it indeed takes the bold, hard, painstaking, culturally challenging, habit changing decisions called for. This will require promoting meritocracy and reason all round whilst cherishing the discipline, quality and respect for the environment that will mean we no longer quantify “progress” as being exclusively a function of the number of cubic metres of cement being consumed or of the GDP growth rate achieved. Indeed, added GDP or consumption if we keep losing our soul and feeling growingly worried or shameful about the country is meaningless. We therefore clearly need a country that values and celebrates ethics, morals, courtesy, honesty, good governance, creativity and the urge to share and lift others far more than sleazy, tawdry power for its own sake, eye popping shopping trips nourished by per diems and platinum cards or heaps of cash piled up high and useless (and sometimes even smelly), rather than being judiciously spread around, fertilising one’s country’s dreams.

Now, where did I read all this before?

(Written on 26/06/18)

Publicité

Publicité

Les plus récents