Publicité

Analysis: The Debt Delusion

Par

Partager cet article

Analysis: The Debt Delusion

The 2019/20 Budget is bent on creating the illusion that public debt is under control. Besides manipulating debt data, the budget is also being used to deceive the public about the true course of public debt.

The Minister of Finance, in paras 428 and 429 of the 2019/20 budget speech, states: “As regards public sector debt, the statutory requirement was to bring it down to 60 percent as a ratio of GDP by end of June 2021. However, we plan to reach this target much earlier. We will make early repayment of public sector debt by using part of the accumulated undistributed surplus held at the Bank of Mauritius.”

In other words, the Minister is stating that the statutory debt ratio of 60% of GDP will be reached much earlier than June 2021, by drawing on the capital reserves of the Bank of Mauritius (BOM), and prepaying external debt. However, his statement makes a false claim, as it is not supported by the data.

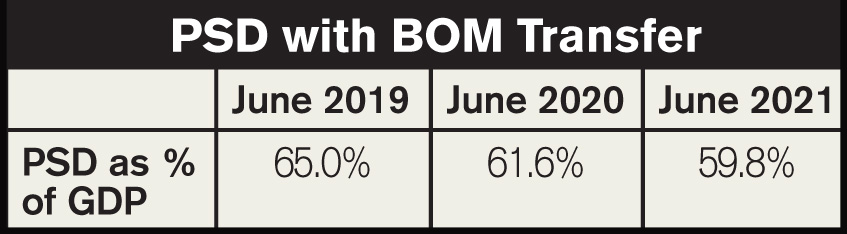

Appendix F on Debt, Budget Estimates 2019/20, shows a drawing from BOM capital reserves of Rs18 bn and an external debt pre-prepayment of Rs15.6 bn in 2019/20, with Public Sector Debt (PSD) ratios as follows:

These figures clearly demonstrate that the statutory debt target is reached at June 2021, and not “much earlier” as claimed. Much earlier is much wrong.

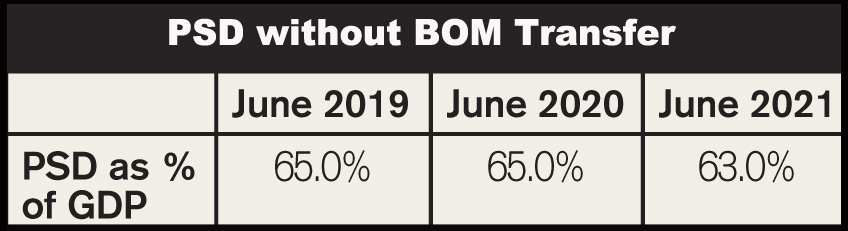

If PSD debt ratios are derived without the drawing of Rs18 bn from the BOM, and without external debt prepayment, the PSD ratio at June 2021 is then higher at 63% of GDP, as shown below:

A BOM transfer of Rs18bn, equivalent to 3.2% of GDP, thus enables Government to meet the statutory debt ceiling in June 2021. Without the BOM transfer, the debt ceiling is exceeded, as PSD at June 2021 would be 63% of GDP.

PSD is likely to reach even higher to 65.4% of GDP at June 2021 by (1) excluding an arbitrary debt “consolidation adjustment” amounting to Rs8 bn, or 1.4% of GDP, and (2) assuming a shortfall of 50% on the projected sale of Rs11 bn of unidentified state-owned assets by June 2021, representing Rs5.5 bn, or 1% of GDP.

Government is resorting to extreme measures to bring down PSD, including raiding central bank reserves, as it may be fearful of public apprehensions about national indebtedness, especially in view of the looming general elections.

Government should instead acknowledge its inability to meet the debt ceiling by June 2021, and extend the public debt deadline by another 2 years to June 2023. The loss of fiscal credibility caused by a further extension of the debt deadline is far less damaging to the image, reputation and financial stability of Mauritius than turning the BOM into a free ATM for Government’s cash needs.

Publicité

Publicité

Les plus récents