Publicité

Looking beyond the 2019/2020 Budget

Par

Partager cet article

Looking beyond the 2019/2020 Budget

Much has been said about the 2019/2020 budget of Mauritius. While a rosy picture of the economy was painted by the government, the reality is somewhat more nuanced. Growth over the past decade has gradually been slowing because both labour input growth and capital input growth have been consistently decelerating. Back in the 1980s, a major jump in female labour participation, a low base from which productivity growth could accelerate from and capital accumulation allowed gross domestic product (GDP) growth to shoot up. In the 1990s, the fruits of a higher quality education system (back then) coming from a lower base allowed labour input growth to continue to increase along with capital accumulation and total factor productivity growth. Mauritian policy makers embraced capitalism and openness to trade, and understood at least that a prudent wage growth and exchange rate policy would be key to maintaining growth momentum. The gradual increase in hand-outs and political largesse could be offset by preferential trade deals with the West. In the 2000s, the fruits of vision from local policy makers and a favourable tax treaty with India helped to offset the erosion in preferential trade with the West.

The International Monetary Fund, in its Selected Issues 2019 paper (“Unlocking Structural Transformation in Mauritius, Challenges and Opportunities”), reports that between 1980 and 2000, labour input growth’s weighted contribution to GDP was 3% while capital input growth’s contribution stood at 2.3% during the same period. From the 2000s till date, labour input contribution slowed to average 1.2% annually while capital input contribution to GDP growth fell down to 1.4%. The small residual between GDP growth and growth in the factors of production was led by productivity growth as the economy transitioned towards a services economy. While the purpose of this article is not to dwell into the well known reasons as to why Mauritian input growth slowed, it aims to tackle the future. The reality is that since 2010 at least, policy makers have failed to address the structural challenges which torment the economy.

For example, with an ageing population, stagnating women labour force participation, the lingering impact of the brain drain of the 1990s and 2000s and an education system which is simply not working anymore, labour input growth will not be accelerating anytime soon and admittedly, unless we are more open to immigration, it will not happen easily. On the capital input growth side, domestic private investment has been declining (it gets worse if you exclude real estate related activities) and this will not change unless the structure and the business ecosystem of the corporate sector change.

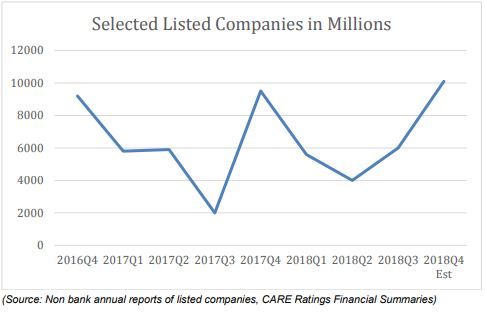

Mauritian companies, especially the larger non financial ones, tend to be asset rich and free cash flow poor (which should make any CFA student ponder about asset valuation standards). Just have a look at the Return on Capital Employed (ROCE) of non bank related listed companies, and it will not be hard to see that large non financial corporations cannot sustain ROCE levels above their cost of debt for a sustainable period. Just exclude the listed banks over the past two years, and you will find that there has been little profit growth when comparing similar quarters to each other. Over the past eight years, this chart would not look stellar either. In fact the last five years have seen a slew of corporate debt restructurings with many taking advantage of the mispricing of credit risk in the corporate bond market with a focus on optimising balance sheets and unlocking liquidity.

The theme has been more about getting one’s house in order and improving cash flows and return on capital versus actually investing on aggregate. The reality is that the investment capacity of the corporate sector is limited, and this situation is further complicated by an outlook wherein most business opportunities would not see returns on capital above the weighted average cost of capital, let alone the cost of debt. With the tourism sector facing obvious headwinds and with troubles within the sugar and manufacturing sectors, a meaningful break from the zigzag pattern of corporate profits looks unlikely in 2019. While the government has done all it can via middle class tax breaks and higher wages for those at the bottom of the wage scale, if the falling trend in core inflation is to be believed, there has been little left when it comes to accelerating consumer spending growth from current levels.

Now if we go down to smaller non listed companies, almost 60% of small and medium enterprises are subsistence corporations with limited growth capacity. The bulk of the rest are not doing that well or are unable to scale up to the next level given the market size, oligopolistic tendencies of some larger peers, the lack of fair opportunities from the public sector, sub-optimal capital structures, corporate governance issues and capacity constraints. What sustains Mauritius’ private investment to GDP ratio is actually not real investment but increasingly luxury villa purchases by foreigners.

There are two economies in Mauritius

Given the current set of policy parameters, it is very hard to see how productive private investment will materially increase. What is left then to be able to grow at 5% plus is our ability to triple our 40-year total factor productivity growth track record of 1% annual contribution. For Mauritius to achieve 5% plus levels of growth, it needs significant structural reforms. The budget may forecast all the 4% plus growth it wishes to, but it is unlikely to happen unless we change a great many things.

To make matters worse, policy makers since 2010 have been increasingly reliant on the Value Added Tax as the major source of revenue leading to an increasingly imbalanced tax structure. Thomas Piketty, who seems to inspire some policy makers, would certainly not argue that a tax system which is so dependent on the VAT could genuinely help to fight increasing wealth inequality. The current set of fiscal policies has essentially pushed the majority of middle class and below Mauritians to consume. Wage increases and tax breaks should be viewed in this light. Such an approach cannot possibly result in effectively tackling rising wealth inequality.

The current government has been engaged in a policy to stimulate consumption growth, but in a country that imports most of what it consumes, such policies can only lead to wider trade imbalances which cannot be sustained. In its last Article IV consultation, the IMF warned that the external balance of Mauritius had worsened and that the rupee itself was overvalued by more than 15%! In layman terms, consumption growth which has been part and parcel of policy making and tax revenue accumulation has pushed import growth upwards which has pushed the authorities to encourage more luxury villa sales to plug the rising external deficit (to finance the imports) to keep the party going. This, when coupled with income from the offshore sector, has brought such large flows (although recent trends are reversing on the flow side) that the rupee has not depreciated as it would have in any market where the trade balance is as weak as that of Mauritius.

An unsustainable wage rate policy above productivity growth by various governments over the past decade has almost killed the manufacturing and export oriented sectors in general, making us even more dependent on the “foreign direct investment” which is really mostly villa sales to keep everyone happy (except for the exporters of course). It has been a nightmarish and vicious cycle of an unsustainable wage rate policy and consumption growth focus resulting in weakening trade imbalances leading to the further encouragement of flows resulting in a currency that does not adjust. There are two economies in Mauritius, and the real effective exchange rate seems to reflect that of real estate developers and the services sector to the detriment of the sugar, manufacturing and tourism sectors.

Public investment has tried to make up for the lack of domestic private investment, but beyond efficiency issues, it too has, in the short term at least, not helped on the import side given the imports associated with the metro project. The deteriorating terms of trade is not sustainable and remains by far the biggest risk to the Mauritian economy given our dependence on the stability and continuation of these flows. The recent weakening trend in our balance of payments then should be viewed very seriously. The purpose of this article then is to precisely address the challenge of how Mauritius can get back on the right track. However all solutions will require significant structural reforms and arguably a change in the political system of patronage itself. We have allowed the unsustainable party to continue for so long that the next dispensation will make it, or the economy will run out of its spree of good luck.

In its latest selected issues research on Mauritius, the IMF developed a financial conditions index for Mauritius. What is clear from this paper is that financial conditions and GDP growth are related with obvious lag effects, and that the main drivers of financial conditions are exogenous (emerging market equities and debt performance), which essentially showcases our increasing dependence on capital flows and positive global investor sentiment. Worryingly, the fact that local factors appeared to be less important in determining the degree of loosening or tightening of financial conditions should be analysed and introspected upon.

The world economy is slowing and even the US Federal Reserve appears to be shifting to a more dovish stance. We may of course ignore all the signs that our good luck may soon run against a brick wall at our own peril.

How do we handle the national debt?

There are essentially two schools of thought making the rounds in Mauritius. One school says that the debt to GDP ratio is high and unsustainable and that Mauritius will go broke, while another smaller school of thought as was written in Business Magazine by a high ranking policy maker warned against abrupt fiscal consolidation and alarmists. The latter gentleman’s argument was that as long as nominal GDP growth could be kept higher than the average cost of debt of government, the level of debt could be sustainable. In my last article, I spoke about a still hotly debated theory known as Modern Monetary Theory. MMT theorists argue that a country that has a strong degree of sovereignty over its currency cannot run out of its currency to pay local debt or any local liability as it has a monopoly over its currency. The reality is that states are not households.

The cost of running fiscal deficits is not measured by interest rates but by inflation which needs to be clearly defined and quantified. The fiscal deficit is simply how much more money you put into the system in a given year versus how much money you took out of the system in the form of taxes. The level of domestic debt is simply an accumulation of deficits which works out to accumulated private savings. When a government chooses to borrow, or when the state pushes liquidity into a system, this goes to the private sector. Taxation then exists to tackle wealth concentrations if private savings becomes concentrated.

Admittedly MMT is intuitive if one understands monetary operations and holds a lot of promise, but if misunderstood, it can create more harm than good especially when there is no official inflation target. Given the recent debate on government borrowing and central bank operations, let me try to explain how this would work in an MMT setting.

Let us assume that the government of country X wishes to constrain or reduce borrowings from the bond market: it can for example approach the central bank and offer it a special bond. This bond would not be traded and the interest rate charged on this long term bond would actually be at a discount to equivalent maturity yields but higher than a central banks’ cost of conducting monetary policy.

So let’s say that the government of that country wants to borrow Currency X 20 billion from its central bank: it would give a bond which the central bank would hold as an asset on its balance sheet and, yes, the government would pay interest at a discount every 6 months until maturity. In return for this asset, the central bank would literally credit the account of government held at that same central bank with the money. In this setup, the central bank gains an interest earning asset, it allows it to improve its margin and asset liability mix because the coupon rate is higher than the cost of monetary operations, its holdings of domestic asset reduces foreign currency risk, and the borrowed money stays at the central bank as a liability.

The government has just created a special strategic fund (or any name you wish) to either finance capital expenditure, investment vehicles, re-skilling or pay down debt in the domestic bond market. In this case, the government has a liability to pay its central bank while the central bank has an asset. At the state level, and this includes the central bank and government, this cancels out, i.e. this is not considered as debt by the likes of the IMF. Of course if country X borrows money from the central bank, the independent central bank must agree to the rate and must have the power to control the flow of money into the system from the account. This is also not a one time operation but can be repeated, and coordination is key.

It is not like the government can redeem all the money at once and distort monetary policy making. You will note here that there is no reduction of the level of capital of the central bank. This is an example of what MMT theorists have been arguing as a way for governments and central banks to coordinate with each other and not engage in severe fiscal consolidation which in the current context can hurt growth.

Another approach would be for the central bank of a country to simply purchase bonds in the secondary bond market which would de facto reduce the outstanding value of domestic debt. By the way, quantitative easing in the West does just this. Such a policy has its limits given where one wishes interest rates to be. The impact on liquidity in the secondary bond market can in turn be reduced by targeting the purchase of smaller issues which can help reduce bond market fragmentation.

Obviously when it comes to Mauritius, this is not what was announced. There is however one big caveat to a proper implementation of Modern Monetary Theory (not to be confused with what was announced) and this revolves around what you can and cannot do with the money. If we raise money in the way I described but end up giving away freebies to everyone so that they can consume more, we will end up worsening the current account deficit, and this will make a bad problem worse. In this case, domestic monetary operations can be disastrous. MMT is only useful when it is limited to policies that aim to increase the factors of production of the economy over time.

The financing of recurrent expenditure and consumption-led growth can not only be very inflationary, especially when a country does not quantify an inflation target as a checks and balances, but it can also have a dangerous impact on the external balance and on the currency. Given the high degree of import content of exporters, stimulating consumption spending via the printing press can indeed be dangerous. This is certainly not what I am proposing to do when arguing for a more MMT driven approach. Those who wish for fiscal consolidation have yet to clearly explain how they will help to increase GDP growth given the realities of the local private sector and structural challenges.

Domestic debt and foreign debt are not the same thing. Mauritius will not run out of rupees to pay or print although inflation is the cost there, but it can certainly default on foreign liabilities. Given the low level of foreign public debt to GDP however, this is not a major concern (unlike our trade imbalance). We should not obsess about our current level of debt to GDP but really obsess about how we make use of the money we borrow (and our external imbalance).

Take Singapore for example. It has a debt to GDP ratio of more than 106% but yet has one of the highest credit ratings in the world. There is one little difference, however, which is the crux of my argument. Singapore does not mostly issue debt to fund recurrent expenditure but largely engages in debt issuance to keep a vibrant secondary bond market (and pension funds happy) and channels domestic borrowings to the Monetary Authority of Singapore which gradually converts these funds into foreign currency (actually it is a swap) and transfers this to the GIC. Despite the debt level of Singapore, the ratings are high because Singapore has positive net assets. The issue is not about the level of the debt but about how you use it.

Singapore GIC

<p style="text-align: justify;">The GIC, which was originally funded by a part transfer of the international reserves of Singapore managed by the Monetary Authority of Singapore (MAS) in exchange for a bond (again it is always double sided) as part of a swap in the early 1980s, is Singapore’s sovereign wealth fund. Singapore only had six months worth of imports as international reserves at that time, but the Singaporeans had the vision with a transfer of around 2-3 months worth of imports to the GIC. It was a small start for a still small country but over time, things changed.</p>

<p style="text-align: justify;">You can imagine that the IMF was not too happy despite the fact that the GIC could still provide foreign exchange liquidity to the MAS, but this was a very visionary leader occupying the top job in Singapore! The GIC has gradually evolved into a major global investor, it hires the best in the world based on merit (no favouritism and nepotism like in Mauritius), good governance and focuses on generating returns that are higher than the cost of getting that money in the first place. The GIC also has a dual purpose beyond being a key catalyst to the development of a modern and vibrant asset management industry in Singapore.</p>

<p style="text-align: justify;">You see way back in the early 1980s, Singapore’s policy makers recognized the fact that Asia would take off, and that if they could be a seed investor in multiple ventures along with major global investors across the region and gain access to networks (part of the portfolio invested in public and private equity early on), they would become the go to value added platform for Asia. The GIC knows what is happening across Asia because they invest in the continent and sit directly or indirectly on multiple corporate boards. By being a large investor in multiple countries, they gain geopolitical clout in Asia. Asian countries in which Singapore invests have a symbiotic relationship. Contrast this with what is happening with Mauritius and Senegal right now. We have a one way street.</p>

<p style="text-align: justify;">When the world wants to go to Asia, it makes sense to go through Singapore. The Goldman Sachs, the JP Morgans, the CITI, the Morgan Stanleys of the world are all there with genuine investment banking operations. The GIC has a dividend distribution policy when it generates excess returns over a certain time period and over a threshold, and this money is paid back to government which then uses this money to help fund expenses. It allows Singapore to diversify its sources of revenues from a budget perspective. The GIC is a long term investor and its backers understand very well that short termism when market volatility picks up is an opportunity, not something to be scared about especially given the team at its disposal and the degree of sophistication of the GIC board and advisory committees.</p>

In Mauritius, we talk about being this amazing platform for Africa but we do not put a lot of money into it ourselves and nor do we really have any grand strategic influence and knowledge about what is going on in the continent. Mauritius has simply never built the right ecosystem as a platform where capital can be raised or seeded from.

If we believed in the future of East Africa (let alone Africa), we should have put our money where our mouth is unless we do not really believe in the continent’s future. In South Africa, its public pension fund has a dedicated Africa allocation. Do we have a pragmatic view of asset allocation given our liabilities made worse with falling local bond yields?

I would also argue that GIC-type setups require a very different meritocratic mentality which is not always very obvious in Mauritius. Good governance is about having the right people at the right places along with greater transparency and accountability. As long as Mauritius does not create the proper ecosystem for onward investments into Africa, it will remain a lower value added platform on aggregate. Incidentally this notion that we would be able to compete with Singapore since we have a slightly more favourable fiscal agreement with India has obviously been proven wrong. We have always needed a large gap in our favour. Policy makers never got the point that Singapore offers more value than we do. Mauritian policy makers have also failed to develop the kind of ecosystem we need for Indian corporates to raise capital on the island from global investors.

Inflation in Mauritius is currently low, private investment is not doing well (domestic) and abrupt fiscal consolidation will have a strong impact on growth. However, if we want to put MMT into practice, policy makers must learn to appreciate its many limits and downsides too especially as it relates to a small and open economy with a large trade imbalance to boot. A little knowledge can indeed be quite dangerous.

The tax system needs to be reformed

Beyond GIC-like ideas where an important source of dividend income can come to diversify the government revenue base, Mauritius’ high dependence on the VAT (which accounts for more than 57% of total revenues) must invariably be reviewed. While GIC- and MMT-like ideas should only focus on increasing the factors of production and strategic investments, taxation needs to meet recurrent expenditure. Mauritius should essentially never borrow to fund recurrent expenditure. The likes of Piketty essentially tell us that as long as the return on capital is higher than nominal GDP growth, wealth inequality will continue to worsen given the fact that capital ownership tends to be concentrated in fewer hands. Policies such as negative taxation pension increases, and the minimum wage will not make a meaningful dent in inequality if the overriding policy is to push them to consume and take the money back in the form of consumption taxation. Inequality goes beyond income and is about total wealth.

In the case of Mauritius where large scale land ownership is quite concentrated in a few hands, policies that aim to monetise land assets for real estate development and sales to foreigners must strike the right balance. Beyond rising inequality, a VAT focused revenue stream may do wonders for tax buoyancy, but it also distorts government policy making towards stimulating import-led consumption which invariably worsens trade imbalances.

A small wealth tax and the conversions of developed villages such as Tamarin into towns making them eligible to pay municipal/property taxes remains important drivers of tax base diversification. The reality is that most of the rich in Mauritius live along the coast and in villages, the same areas whose district councils lack adequate funds, and these are the same areas with large pockets of poverty. On the spending front, the government has a few limited choices. It can increase taxes which, beyond some moderate forms of wealth taxation, may hurt the economy too, cut spending on everyone or review its spending priorities and move towards a more targeted approach when it comes to re-distillation. Obviously the biggest hurdle will be the system of political patronage itself.

There is also a need to engage in a meaningful reform of the civil service with a focus on ridding the country from the cancer of nepotism and favouritism. It is high time to implement a fair structure of fast promotions for those who add value and performance based bonuses linked to clearly defined key performance indicators. It is high time to professionalise the way human resources are managed and reduce the influence of politicians and occult forces in pushing their men at key posts which more often than not they are under-qualified to hold.

In a system where the civil servant feels that there is nepotism, favouritism and a lack of a career path, he/she will invariably push for maintaining a salary ratio system within regularly set and increasingly unaffordable salary increases. The example must also come from the top. Given the pace of wage increases within the civil service and growing pension fund liabilities for those who are still in defined benefit schemes, there is an urgent need of reform and evolution in the way the civil service is managed.

Seeking productivity enhancements

The government along with parastatal bodies are by far the largest employers of Mauritius and have significant influence on the current state of the economy. If the country wishes to triple total factor productivity growth then quite clearly, all government related bodies need to be de-politicized and reformed. A healthy democracy also requires a competent pool of technocrats but over the years, favouritism and nepotism have ensured that the wrong people are put at the wrong places. Public institutions lack clearly defined key performance indicators and objectives, governance structures are laughable and senior employees too have increasingly been able to move up the ladder by the politics they play versus merit. Many parastatals do not even publish proper annual reports, and political nominees are more often than not clueless about what they need to do hold these institutions back.

Politicians often like to copy Singapore in areas where it may be convenient, but one should not forget that, be it ministers, senior officers or board members, Singapore ensures that base salaries are adequate but that the upside is mostly made up of performance base bonuses set on clearly defined Key Performance Indicators. I understand that the ethnic and exotic political setup in Mauritius is complex, but it would be good to have a system that ensures that interests are aligned. Politicians and board members in the public service are free to appoint who they wish, but just like in Singapore, it would be good that the vast majority of their pay be linked to performance too within a 40% base salary and 60% performance bonus split. In order to avoid short termism, can we imagine a system where the bulk of performance based bonuses would be invested in the Mauritian stock market via passive index funds as a proxy for the economy with the Prime Minister allowed to only redeem 1/5 of paid bonuses each year?

Similar to how the private equity markets align interests, there would also be claw back provisions in case short term moves led to longer term losses. Perhaps this kind of setup would also reduce the number of yes men who swarm around politicians all the time in order to obtain key posts post electoral victory if they know that they actually have to deliver to make decent money.

A nominee of a public bank or airline company would have the bulk of his salary paid in bonuses via share options. There are many schemes which can be created also for non listed companies driven by clearly defined KPIs. I would argue that politicians’ behaviour towards putting any Tom, Dick and Harry at key posts would see quite the change if the system ensured an alignment of interest. Suffice to say that this setup would apply to all senior officers as well.

Rather than receiving fixed per diems on expensive and frequent foreign trips and in the spirit of good governance and cost savings, corporate credit cards would also bring decent cost savings across public institutions. All officials travelling less than six hours, from minister down to the average officer, should also travel economy class and be treated equally. One cannot tell a civil servant or an officer of a parastatal to tighten his belt when he sees obvious abuse at the top. Politicians and their men must indeed lead by example if we truly wish to have fruitful negotiations with trade unions.

Clearly defined KPIs and a system that is more independent and meritocratic would do wonders to the way public setups are run and would certainly increase their weighted contribution to the economy. The bottom line is that we can throw stones at the way the local private sector functions in Mauritius, but there will be no 5% plus growth in Mauritius unless there are significant reforms in the way government related bodies are run and managed.

Focusing on measures to stimulate private investment

Politicians often wonder why so many Mauritians wish to become civil servants rather than entrepreneurs. The reason why the democratisation of the economy has failed is quite simple. Between the increasing trend of vertical integration of larger and more well established corporations, the lack of alternatives to traditional bank funding for capital structure optimisation and favouritism in obtaining government contracts (which seem to always land on in laws and nephews of ministers and leaders), what did we expect? Mauritius is a country where all the power is centralised towards the Prime Minister of the day, which is certainly not a sign of a healthy democracy where checks and balances exist. In this environment, corporatism rather than capitalism thrives.

In a country where the government and public bodies account for a large share of GDP, a fairer distribution of contracts across districts could do wonders in stimulating revenue growth of small and medium enterprises across communities. Secondly, public owned pension funds are major local equity investors but are extremely passive shareholders given the lack of independent and professionalised setups. In Europe, Asia or in the United States, if CEOs do not perform as expected, shareholders throw a fuss. In Mauritius, the minority shareholders are extremely passive and even brokers never put out a SELL recommendation (a HOLD is actually a SELL in Mauritius).

The tax and incentives system of government also needs to be reviewed because many large private setups have made it a habit of depending on government money. Mauritius simply does not currently have a system where those who do not perform perish. At the end of the day, corporations need to generate decent free cash flow yields, and over time, shareholder bases need to evolve towards one that is less concentrated, but in between large minority institutional investors need to push for greater performance and accountability. When it comes to vertical integration, while we cannot blame large corporations that seek to optimise their business models in a small country, the Competition Commission of Mauritius clearly has a larger role to play than it has.

That being said, when we speak of small and medium enterprises and even select larger ones, there is a dominant argument that there is no lack of financing in Mauritius. This is not accurate. There are certainly excess funds in the form of traditional plain vanilla bank debt ready for financing, but that may not always correspond to an optimal capital structure, and the type of financing also depends on the development stage of the firm in question.

Mauritius lacks a vibrant venture capital ecosystem and a private market which offers flexible capital funding to those who have good ideas and who are willing to accept certain conditions such as improvements in governance structures and accountability. Local pension funds, especially those run by the government and policy makers need to encourage identified companies which have the potential to scale up and provide flexible capital funding (from equity, not just some limited funds in the form of preference shares). Such policies would be ideal for export-oriented enterprises that showcase promise as regional exporters. Clustering too is needed.

On the pension fund side, the reality is that 3% plus real returns (returns above inflation) cannot be achieved by investing in fixed deposits and low yielding government bond yields alone. There is a need to professionalise setups and encourage the development of private markets as an asset class, as is done elsewhere. I am convinced that there is a lot of value which can be unlocked by local entrepreneurs if we create a vibrant private market in a low yield environment, bringing investors seeking higher returns and those seeking capital together. However, the running of such setups needs to be apolitical but accountable. Remember, the side providing the funding needs to make decent returns on investments.

We should also not be against funding larger corporations (rather than giving out inefficient tax breaks), especially companies seeking regional expansion that work in our national interest. Mauritius needs scope and scale in East Africa, and while we will not achieve this in the short term, we need to start somewhere and leverage the scale that co-investing and seed funding provide. Mauritian policy makers need to quickly setup a task force to stabilise the export sector. Otherwise, in the not so distant future, the growing trade imbalances and our dependence on foreign capital flows, which are invariably volatile, will hurt the economy economy in ways most Mauritians cannot begin to imagine.

Be it the quality of education system, the lack of research and development funding versus comparable upper middle income peers, the need for greater funding to transition job guarantee (combined with reskilling programmes) schemes or the setup of strategic investment vehicles which will help to not only create a better funding ecosystem but also bring about efficiency gains, a form of Modern Monetary Theory will invariably need to be considered by Mauritian policy makers in the coming years. Mauritius needs better ports and has to invest a great amount of money in the blue economy and in green technologies, and this will not happen unless the fiscal stance is supplemented in some form.

Before dreaming about Artificial Intelligence, we need to get the basics on the level of math in our education system right, we need to fix up our local public run universities. We have yet to find adequate resources for our Information and Communication Technology sector, and we are already dreaming about AI. As someone who works in the AI field and has lived in Mauritius for some time, there is a lot that needs to be done before we can move towards AI. This in itself deserves its own article.

On the recurrent expenditure front, Mauritius needs to review its tax policy and seek a system that is more balanced and one that genuinely attempts at least to slow rising wealth inequality. Mauritius needs to focus on schemes which will stimulate private investment and efficiency. Finally, no 5% growth target will be achieved unless total factor productivity growth triples. In turn, this will not happen unless there are significant reforms in the way the government and related corporations are run.

Be it this national budget or the previous ones, policy makers are either unwilling or unable to bring about such changes. At the end of the day, it will be about what the people wish for. I have often argued that Mauritius is too old (ageing population) and too far away from the happenings of the world to change and break out to the next level. I certainly hope that I am wrong. At the core of what I have said is a realisation that the current political system, key to where we as a nation have reached now, holds us back. Either we accept to change it and change it well, or we accept our fate. There is no middle path to break out to the next level. Bold decisions and vision are clearly the order of the day.

Sameer Sharma

(Chartered Alternative Investment Analyst and a Certified Financial Risk Manager)

Source : Conjonture/PluriConseil

Publicité

Publicité

Les plus récents