Publicité

Analysis: A cynical and callous policy and practice akin to scorched earth (terre brûlée)

Par

Partager cet article

Analysis: A cynical and callous policy and practice akin to scorched earth (terre brûlée)

PART 1

Introductory remarks

Let us be frank. Ministers of Finance across the world always try to shine a better light on their budget by resorting to a few fiscal ruses and financial stratagems. On the day the budget is presented, very few people see and understand those artifices as the Minister speaks only about what he wants us to hear and to know. The less rosy parts are either relegated to technical supplements and appendices (such as the Rs 11 billion (billion) of public assets disposal) or simply ignored (the massive increase in FSC fees for global business companies). Then as the budget unravels, shrewd and informed observers start seeing into this craftiness and realise the extent to which we have been led down the garden path. Done in moderation and without threatening the fundamentals of the economy, such manoeuvre can be condoned. This is often life in the politics of the bud- get and it must be acknowledged even if many do not like it.

The difference with Pravind Jugnauth in his last budget for the current legislature is that he has broken all records by the sheer scale, scope and magnitude of these tricks and slyness. All carefully planned, thoroughly calculated and unscrupulously executed with little consideration for macroeconomic stability, sound public finances and the prudent management of the public sector debt. And oblivious of the disastrous consequences of his fiscal recklessness for the future of our economy. The only objective was to create a feel-good factor to enhance his chances when contesting the next elections by a helicopter-type distribution of some goodies to specific groups.

The best as the enemy of the good

Based on reactions to the Budget, he has clearly overstretched it and it has achieved exactly the opposite effect. The tricks have backfired. Pravind Jugnauth has been awfully counselled by his advisers and spin doctors to exaggerate on these subterfuges as it has allowed the perfect to be the enemy of the good. His good measures have thus been engulfed by the vortex of sustained recriminations unleashed by his overzealousness to hoodwink the system.

In King Lear, Shakespeare puts it aptly as ‘striving to better, oft we mar what’s well’.

Or the aphorism of Voltaire that ‘the best is the enemy of the good’ captures what has happened to the Prime Minister in the aftermath of the budget.

He has been sucked in the maelstrom. And as Warren Buffet famously averred ‘only when the tide goes out do you discover who has been swimming naked’.

Unfortunately, he is now running to seek cover and clothes and to justify the unacceptable. Only a reversal of some of the very controversial measures such as the confiscation of the reserves of the BOM could restore some calm. Judged by his excessively aggressive summing up last week, he is unlikely to tread the path of reason and responsibility. It is known that some political actors furiously dig when they are already in a hole.

The Budget 2019/20 is a toxic mix of a raid on the reserves of the Bank of Mauritius, a fire sale of some crown jewels of the nation, a brutal stripping of the surpluses of many public entities and some colourable accounting tricks to largely underestimate the size of the budget deficit and the level of public sector debt.

I shall use the very figures of the Minister and the contents of the various Supplements and Appendices to the budget to demonstrate each of these charges.

The Bank of Mauritius heist of Rs 18 billion

Most of us have been shocked by the dangerous and irresponsible transfer of Rs 18 billion representing 3.6% of GDP from the Bank of Mauritius to the Ministry of Finance for the early repayment (Rs 15,65 billion) and the scheduled repayment (Rs 2.35 billion) of some of the external debt of the country. The only purpose is to show a lower public sector debt from 65% at June 2019 to 61.6% at June 2020 and 59.8% by June 2021 by the use of an unprecedented measure. The BOM Act does not allow such illegal transfer from its Special Reserve Fund as per clause 47. Hence the necessity for the Minister to amend the Act to permit such unlawful appropriation. The proposed amendment of the BOM Act is broader than the early repayment of external debt as it goes beyond using the special reserve fund exceptionally for monetary policy to include fiscal policy too. This is no more than pure deficit financing. There are two transactions folded into one. First the transfer of Rs 18 billion from the Special Reserve Fund of the BOM to the Exchequer and second the use of the proceeds for the early repayment of some external debt. Never mind that these external debts represent a paltry 8% of the public sector debt, are very cheap at around 2.5% annual interest in US $ and with a meagre debt service ratio of 4.9% at June 2019.

The fire sale of Rs 11 billion of some of the crown jewels of the nation

At para 196 of the budget the Minister of Finance states that ‘We will also dispose of certain non-strategic assets to reduce the level of government debt’.

However there is complete opacity on which public assets will be sold, to whom, in what manner and for what amount. One has to dig into Appendix D titled ‘Loans and Equity’ to discover that Rs 11 billion of public assets will be disposed over two years. Rs 5 billion worth of public assets will be sold in 2019/20 and another Rs 6 billion in 2020/21. Nothing about which assets and whether there will be a transparent process for their alienation.

The conversion of the surplus of public companies of around Rs 11 billion into Treasury papers

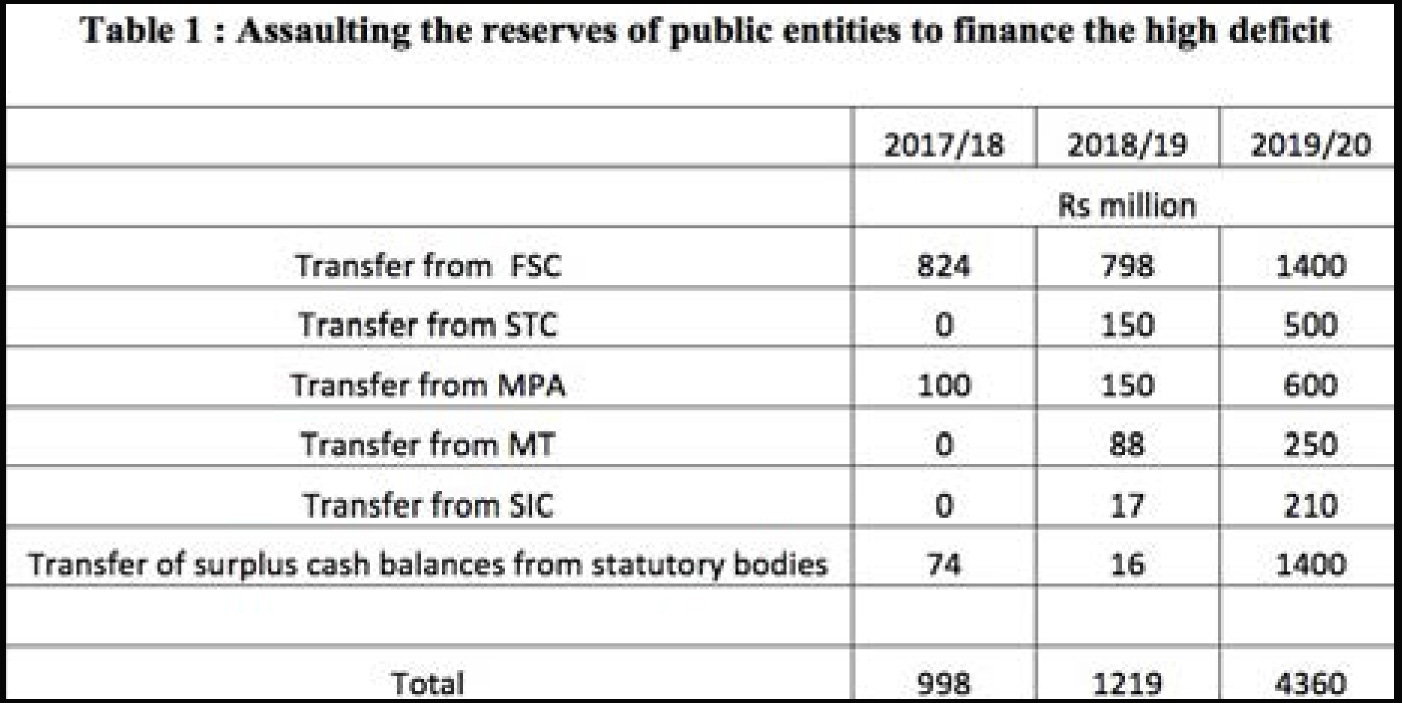

For some time Government has tried to underestimate the size of the public debt by resorting to a spurious definition of net public sector debt as opposed to the international standard for computing the gross public sector debt. The difference lies in the cash balances of non-financial public sector bodies such as the CEB, MPA, CHC and the STC. At December 2018, those cash balances represented Rs 32 billion or 6.7% of GDP. What Government has done is to compel these public sector bodies to convert their surpluses into Treasury papers to the tune of around Rs 11 billion over a four year period. The Boards of the public entities have been instructed to comply with this directive from the Ministry of Finance. As they belong to Government, this translation has the effect of lowering the debt by an equivalent amount over four years as Government cannot be indebted to itself. This transaction is concealed in the new item specially created in the debt profile of the country. It is characterised as ‘Consolidation Adjustment’ in Appendix F on public sector debt. The relevant section is shown at Table 1.

That item simply did not exist in prior years. It was zero in June 2015, 2016, 2017 and 2018. In the estimates of 2018/19 it was again zero. Now it suddenly shows up as a revised estimate of Rs 4 billion in June 2019. And a projection of Rs 6 billion in June 2020, Rs 8 billion in June 2021 and Rs 4.5 billion in June 2022. A staggering aggregate amount of Rs 22.5 billion over four years while it was inexistent since 2015. It is sheer magical incantation to hide the true size of the public sector debt.

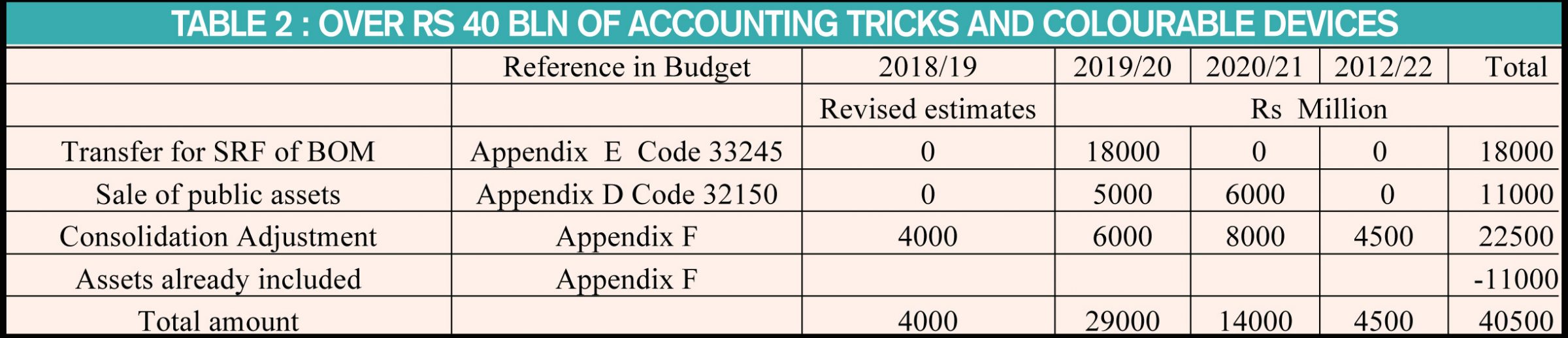

Over Rs 40 billion in creative and voodoo accounting

Table 2 illustrates how the Minister of Finance has doctored the budget deficit and the debt figures in a deliberate strategy to outwit the nation and to embark on a policy close to ‘terre brûlée’ with respect to these two key macroeconomic indicators.

The predicament is as follows:

- The expropriation from the BOM represents Rs 18 billion or 3.6% of GDP;

- The fire sale of public assets accounts for Rs 11 billion or 2.2% of GDP;

- The forced conversion of the surplus of some public entities stands at around Rs 11 billion or 2.2% of GDP over four years;

- The total is around Rs 40 billion representing a staggering 8% of GDP.

PART 2

1. Scraping the bottom of the barrel of public entities’ surpluses and reserves

Table 1 shows how the Minister of Finance has raided the surpluses and reserves of some public entities to finance his excessively high public expenditures. The transfers are abnormally high by historical standards.

The projected revenue of Government in the Budget shows that

i) the FSC which transferred around Rs 800 m in the previous two years will this year contribute Rs 1.4 b, representing a substantial 75 % increase to the consolidated fund. Its reserves have been depleted and it has had no choice to replenish it by immediately raising the fees for global business companies in a range of 25% to 150%;

ii) the contribution of the STC climbs up from zero in 2017/18 to Rs 150 m in 2018/19 and to Rs 500 m in the current budget. A sizeable 233% rise in the transfer;

iii) the MPA is transfering Rs 600 m in the budget compared to Rs 150 m last year. A marked growth of 300%;

iv) MT will contribute Rs 250 m this year compared to Rs 88 m last year and nothing in 2017/18. A huge escalation of 184%;

v) the SIC will transfer Rs 210 m compared to Rs 17 m last year and nothing two years ago. An astonishing increase of 1100%;

vi) transfers of surpluses and statutory reserves from some public bodies will go up to Rs 1.4 b from Rs 16 m last year. A frightening multiple of 87 times;

vii) the combined transfers from these public entities grew by 22% from 2017/2018 to 2018/19; it will skyrocket by 258% in the current budget to Rs 4.36 b from Rs 1.22 b last year.

If this is not ‘après moi le deluge’, it very much has a similar appearance to it! Never has a Minister of Finance raided the reserves and surpluses of public entities with such unquenchable rapacity.

2. The size of the budget deficit as per the statement of Government operations

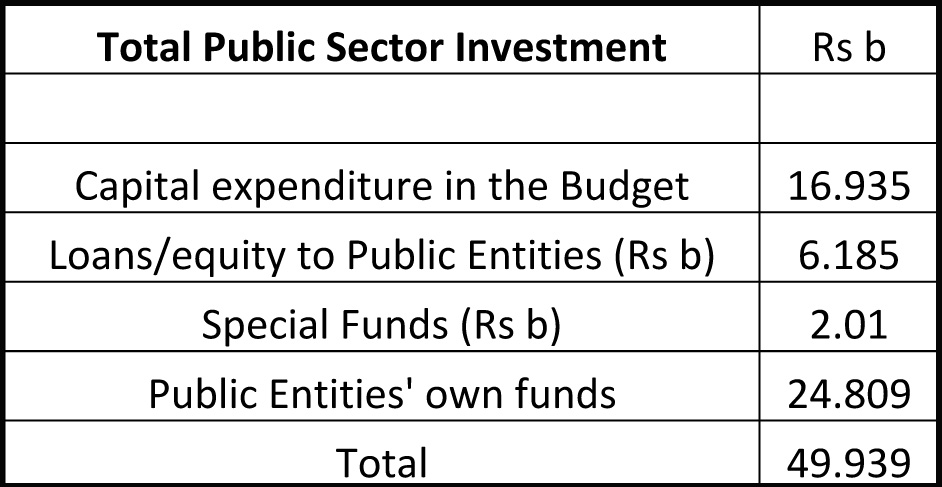

The statement of Government operations contained in the 2019-20 budget reveals a higher budget deficit than the 3.2% indicated by the Minister of Finance. As shown at Table 2, the document submitted to the National Assembly clearly indicates that total public sector investment will amount to Rs 49.939 b in 2019/20. Only Rs 16.935 b are included in the budget while Rs 24.809 b will be financed by the own funds of these public entities. The Rs 6.185 b of loans/equity to public entities and the special funds of Rs 2.01 b are missing in the computation of the budget deficit. The total of Rs 8.195 b represents around 1.6% of GDP. If this is added to the official budget deficit of 3.2% of GDP, the real deficit rises to 4.8% of GDP. Even this higher figure does not include some recurrent expenditures kept outside the budget such as the Rs 1.7 b (0.34% of GDP) for the subsidy on rice, flour and cooking gas announced at para 425 of his speech, but hidden in the STC accounts.

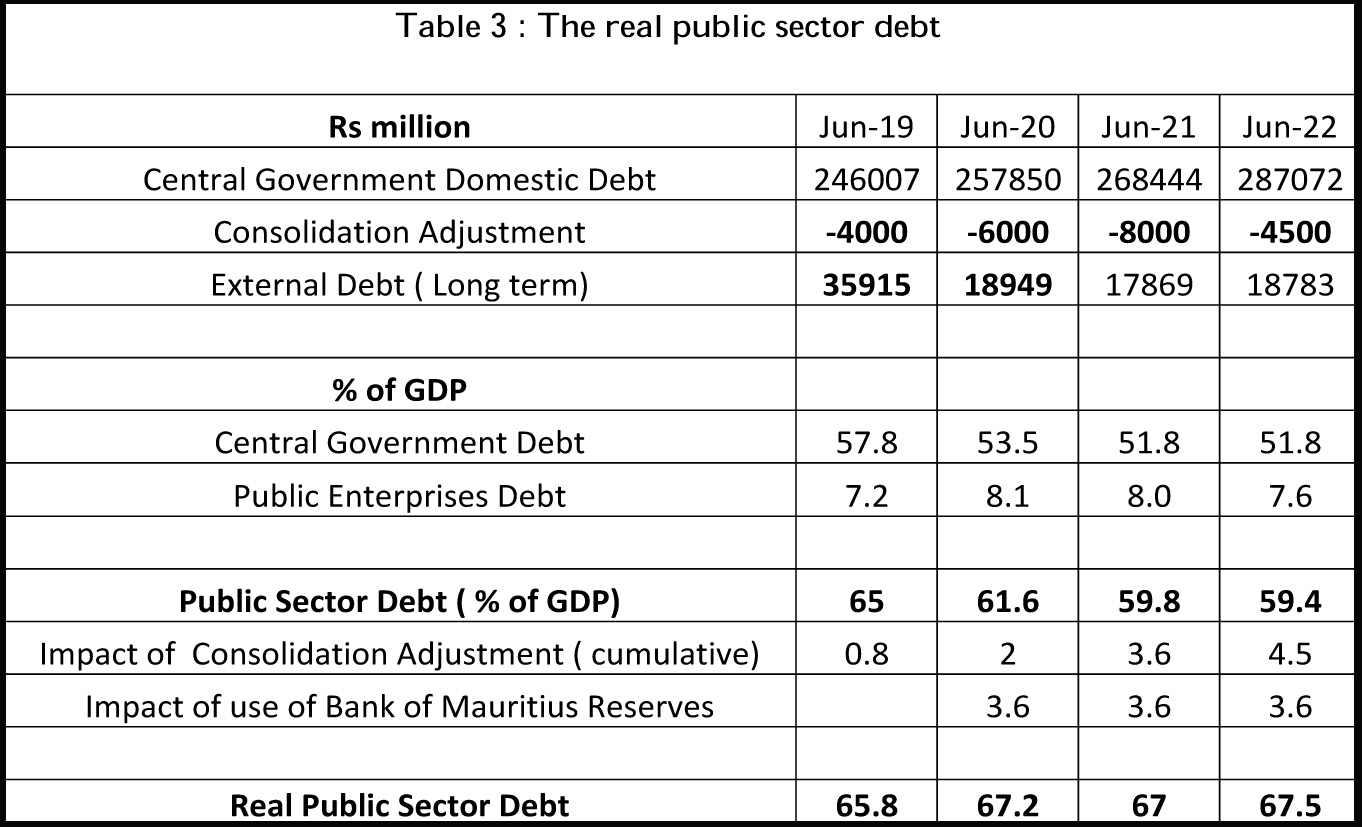

3. The real level of the public sector debt

Table 3 summarises the public sector debt as it appears at Appendix F of the Budget .

The following is plain from the table.

i) The public sector debt is estimated at 65% of GDP at June 2019. If the consolidating adjustment were set aside, it would rise to 65.8% of GDP;

ii) Government is siphoning Rs 18 b from the Bank of Mauritius special reserve fund to prepay and repay some external debt in 2019/20. This is clearly shown at the item ‘External Debt’ in the Table as it decreases from Rs 36 b in June 2019 to Rs 18.9 b in June 2020. There is also Rs 6 b from the consolidation adjustment in 2019/20. These two combine to bring down the public sector debt artificially to 61.6% of GDP in June 2020 compared to 65% in June 2019. Exclude these two items and the public sector debt continues its rising trend at 67.2% of GDP;

iii) Using the same rationale, the real public sector debt would rise from 59.4% of GDP as announced by the Minister to 67.5% of GDP in June 2022;

iv) The figures do match. The difference between the official level of debt at June 2022 and what it should be is around 8% of GDP (59.4% published by Government and 67.5% of GDP as derived from Appendix F). It represents around Rs 40 b which is very close to the total amount appropriated by the Minister as shown yesterday.

v) The Appendix F on debt does not consolidate the totality of the debt amount (dressed up as equity) injected by Government in some public entities. A simple example will highlight this subterfuge. Govt has borrowed US$ 500 m from India for some public sector investments that it has camouflaged into a SPV operated and ma- naged by the SBM. The amount of debt committed is US$ 500 m or Rs 18 m. However the loan will be disbursed over few years. Government is only including the sum disbursed in the definition of public sector debt as opposed to the loan amount contracted. Assume a hotel takes a loan of Rs 500 m from a bank to build a new property. The said amount is disbursed over 5 years in equal tranche of Rs 100 m. Government is including only Rs 100 m as debt as opposed to the contracted loan of Rs 500 m. If the full amount of these debts were consolidated together with the loan taken from China to build the Côte d’Or complex, the public sector debt would soar to above 70% of GDP.

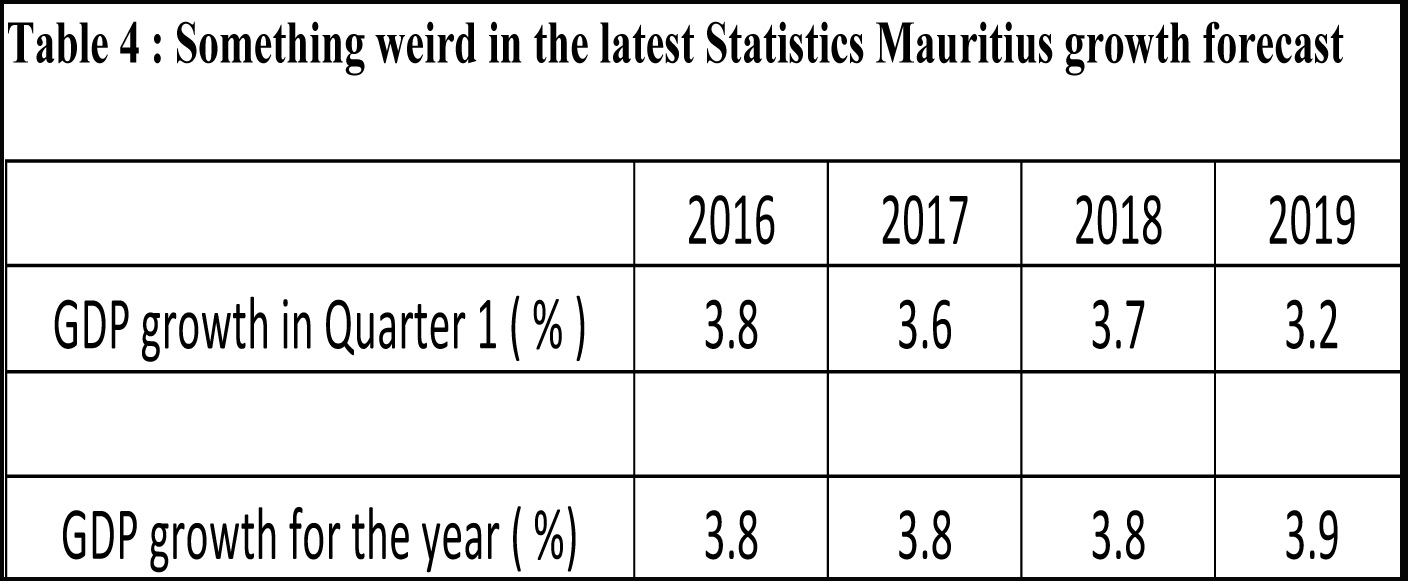

4. The mysterious forecast of GDP growth for 2019 by Statistics Mauritius

Statistics Mauritius (SM) released the GDP growth for the first quarter of 2019 last Friday. It stood at 3.2%. Yet it maintained its growth forecast for the year 2019 at 3.9%.

This is simply eerie.

Clearly, this growth forecast of 3.9% for 2019 is grossly exaggerated.

This is depicted at Table 4 which shows the trend in first quarter growth and that for the whole year for the period 2016 to 2019, including the SM forecast of 3.9% for 2019.

Even if there is seasonality among the four quarters, it required a first quarter expansion of around 3.6% to 3.8% to produce an overall growth of 3.8% in GDP in 2016, 2017 and 2018. Now with an actual growth of only 3.2% for the first quarter of 2019, SM is predicting a higher annual growth of 3.9% for 2019 compared to 3.8% for the three preceeding years.

This is not serious and the institution will lose its well earned credibility if it continues to be manipulated by the Ministry of Finance. There is no prize for guessing what will happen. SM will simply lower the growth forecasts in its last quarterly report for 2019.

The dependable MCB Focus has already shaved its growth prognosis to 3.8% for 2019 with some downside risks, signifying that it could be lower at 3.7%. And it is predicting only 3.5% growth in 2020. That is closer to reality. Last year, tourism contributed 0.4 percentage point to growth in the first quarter and around 0.3 percentage point during the year.

For the first quarter of 2019, its contribution is negative at minus 0.1 percentage point. As the number of tourist by air has contracted by 3% for the first five months of 2019 while earnings for the first four months are down by 9%.

SM is estimating a 2.5% growth in tourist arrivals this year to reach the 3.9% overall growth in 2019. As growth in arrivals by air is already negative 3% for the Jan-May 2019 period, the numbers will have to grow, on average, by around 6.5% for the remaining 7 months for SM to get it about right. Highly unlikely on current trend!

5. Concluding note

I could go on. The net worth of our country has shrivelled from Rs 126 b at June 2017 to Rs 105 b in June 2018 while our financial assets have shrunk from Rs 77 b to Rs 66 b over the same period. There is a significant bunching of the grant component of the capital revenue. Grant stood at Rs 2.2 b in 2017/18 and Rs 3.9 b in 2018/19. It will increase significantly this year to Rs 5.7 b (1.14% of GDP) before dropping sharply to Rs 2.4 b in 2020/21 and Rs 1.1 b in 2021/22.

When the tide of grant would have gone in 2022/23, we would be swimming naked. Naked because of the recklessness and irresponsibility of the Minister of Finance who tried to outwit all of us with a gamut of measures from the raid of the Bank of Mauritius reserves and the disposal of public assets to the appropriation of surpluses and reserves from many public entities and the accounting tricks to mask the true size of the budget deficit and the public sector debt.

Publicité

Publicité

Les plus récents