Publicité

Why there will be a slow recovery requiring a different business model

Par

Partager cet article

Why there will be a slow recovery requiring a different business model

The Covid-19 outbreak is a human tragedy, causing more than 280 000 deaths across the world. It also has a growing impact on the economy. And there is a rising consensus that the recovery will be slow, uneven and painful, according to Sameer Sharma, a chartered alternative investment analyst.

It took 12 years for the United States (US) to create 22 million jobs but just 4 weeks to lose it all. While we remain optimistic about scientists’ abilities to eventually find a vaccine in the coming months, the world economy will simply not be the same as it was before as secular trends such as rising sovereign and corporate debts, high fiscal deficits, further steps towards de-globalization, increased automation in the workplace, a digital cold war between the US and China and even greater levels of unemployment, wealth inequality and more populism all lead to a permanent negative supply-side shock. There is a rising consensus now that the economic recovery will be slow, uneven and painful and that the coming decade will be one with increased risks of stagflation given current trends.

In a world with lower growth and higher inflation, Governments seeking to maintain tax buoyancy will put more pressure on offshore jurisdictions like Mauritius. In a lower growth environment, capital structures of firms will need to rely more on patient capital rather than on leverage and more importantly business models will need to be re-assessed. Central banks be it in the West or in emerging markets all recognize that while deflationary pressures in the coming months remain strong given the extent of the demand side shock which is outweighing the supply side shock, this will not last for much longer. This is why both Governments and central banks are front-loading both unconventional fiscal and monetary policies geared towards the credit channel and wage support in the now before rising inflation in a post-Covid- 19 recovery world prevents central banks from maintaining such support at least on the wage support front via debt monetization.

reserves, increasing the monetary base, according to the author.

Constraints in Government borrowing capacity

There has been a spree of recommendations from all corners in recent weeks advising the Mauritian Government to take advantage of low rates locally and borrow extensively at the long end of the yield curve and also seek longer-term hard currency borrowing from the likes of the International Monetary Fund (IMF). Many have argued that unconventional monetary policy should only be tried after such measures are exhausted as liquidity injections without any structural increase in production would invariably lead to greater inflation.

While there is no doubt that Mauritius should follow a small bit of an all of the above approach, the long term debt sustainability metrics of the Mauritian Government when added to both unfunded liabilities and future contingent liabilities were already unsustainable in January 2020. This is after all why Mauritius had already made use of the helicopter in December in order to pay down foreign debt and will invariably amend the Bank of Mauritius (BoM) Act to do so again. While Government debt to GDP was anywhere between 65% and 70% of GDP in December 2019 depending on how one views creative debt accounting, the present value of future Basic Retirement Pension (BRP) payments (25Bn MUR cost this year) which will be fully born by Government currently stands at a whopping but low ball estimate of MUR 625 Billion assuming we do not even increase payments in coming years and given a significant drop in long term bond yields which pushes up the present value.

The BRT is like a perpetual bond and given the unfavourable demographics of the country, it will consume between 7% and 8% of GDP in terms of annual expenses by 2035 from the current 5% of GDP. Note that tax revenues and levies stand at between 18% and 20% of GDP at best in Mauritius. Pushing for indexation of BRT payments to life expectancy or moving to a more targeted payment approach is politically impossible albeit necessary. No one dares to talk about it, so much so that many are talking about adding more long term debt today that will all mature in 15 to 20 years when these problems will crop up with a bang.

The National Pension Fund is on its part going to become a contingent liability for the Government in two and a half decades or so as it will run out of money to meet its liabilities. The NPF needs to generate CPI + 3% returns over the long term to even last until 2083 but given its sub-optimal strategic asset allocation which is too heavy in low yielding local bonds and mispriced local corporate bonds and the lack of diversification and given the lack of a professional fund management company managing it more tactically, it cannot generate such returns with the way it invests now.

Given the drop in bond yields and their high likelihood of staying low for longer, no increases in contributions and no evolution in the way current funds are managed, 2045 to 2050 will likely be an interesting period for the Government. In plain English, we are constrained because we have too many liabilities and it is not responsible to push all debt cans down the road which is why we had already gone unconventional prior to the current crisis.

Constraints on Government taxation and revenue-generating capacity

As can be understood, the Mauritian Government will need to cut spending on low return capital projects and salaries which will be politically problematic to its base and gradually shift to a more progressive form of taxation in the coming years but this will not be enough. The liabilities are too high, we have ignored them for too long and besides if Mauritius pushes taxes up too much, it risks destroying its “low and stable taxes” marketing which brings much needed foreign exchange and jobs to the country.

We can look at mild forms of progressive income taxation, at public disinvestments and land value or property taxation on the rentier economy in particular and some more bank levies but if we push too hard in a low growth environment on any of these fronts, we risk causing more harm than good. At a time when the world is de-globalizing, a small open economy like Mauritius should do the reverse and be encouraging young Africans, Europeans and Indian entrepreneurs to set up light industries and their fintech companies out of Mauritius. For this to happen, we need to build a modern ecosystem where capital can be raised out of. Easier said than done yes, but we must try.

Painting all unconventional monetary policies with the same brush is wrong

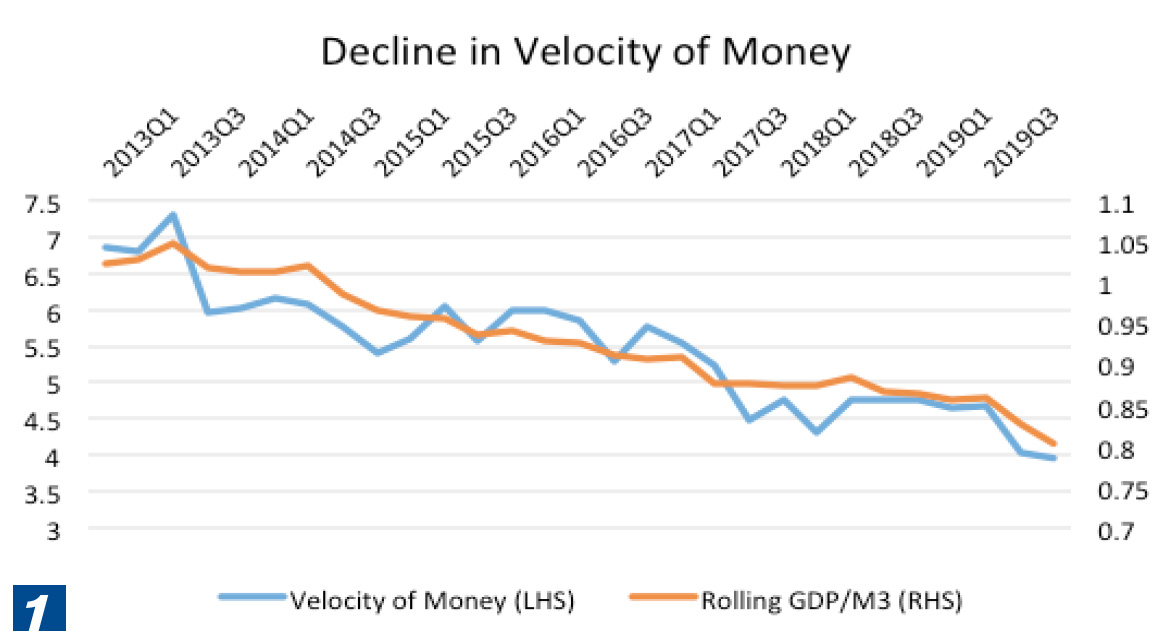

Over the last decade, the velocity of money (proxied by Nominal GDP/Monetary Base) in Mauritius has been declining because the monetary base has been expanding much faster than nominal GDP has been. Since mid-2012, when the BoM engaged in operation reserve reconstitution, it has accumulated billions in foreign exchange reserves. When a central bank buys foreign exchange from the domestic market, it creates rupees out of thin air and injects it into the system to buy the foreign currency. This increases the monetary base.

The central bank can limit or counter this expansion of the monetary base by issuing BoM monetary policy instruments such as BoM Bills but given the costs involved, the statistics which are available in various monthly statistical bulletins and IMF Article 4s, show that not all of this created liquidity was sterilized. In recent months, the BoM in fact has been reducing the total amount of BoM instruments outstanding.

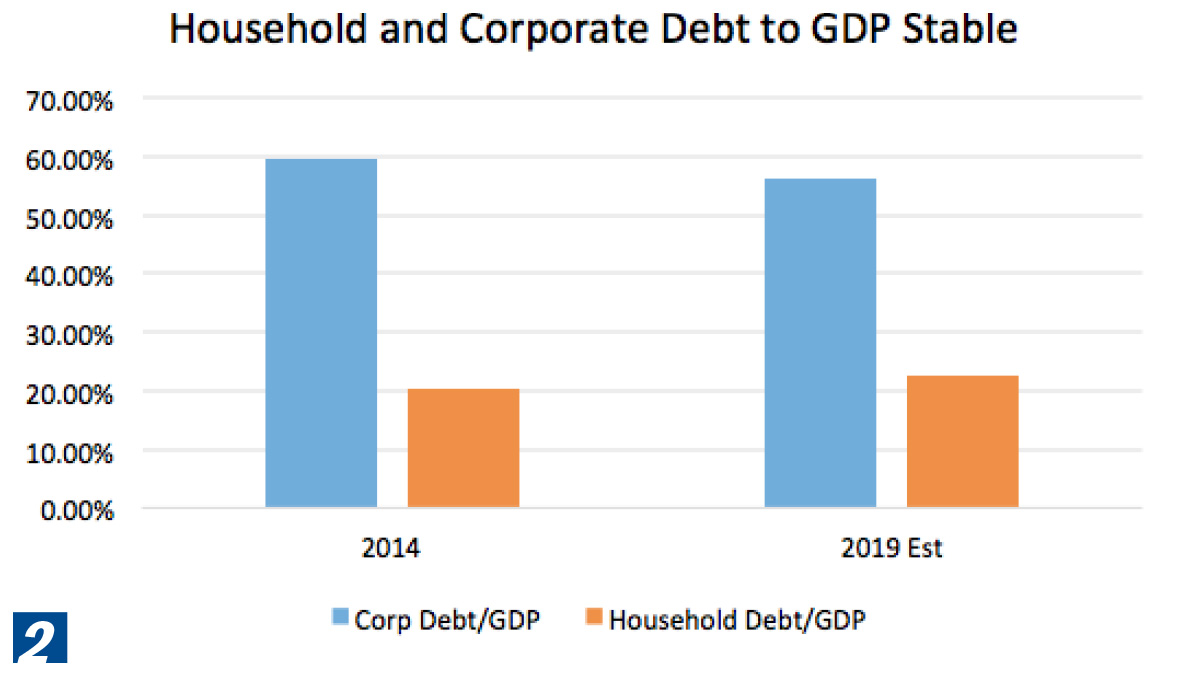

QE in the west was about buying bonds and in Mauritius, it was perhaps an unintended result of foreign exchange buying. Globally inflationary pressures remained low during the past decade and the drop in velocity was not inflationary on the CPI side. Where did all of this Mauritian QE money go and what distortions did it create you may ask? Beyond what the BoM sterilized from banks, the Government which went on a borrowing spree over the past 8 years was the main recipient and partially prevented the money multiplier from falling. Both household and local corporate debt to GDP rose marginally over the past 6 years as a free cash flow to debt metrics remained poor and restructuring was more the priority of the latter while already high levels of homeownership meant a more stable ratio for the former.

Government borrowing to finance populist measures boosted consumption yes but given the high import content in these goods, GDP growth did not really increase as much as some hoped. We can also note that banks were relatively conservative when it came to local lending and only relaxed in about 2018 when macro-prudential measures were eased. In an environment characterized by too much money chasing too few viable deals, excess liquidity meant that rates remained low, the Government borrowed heavily and large corporates engaging in debt restructurings benefited from credit mispricing and amazing CARE ratings in an environment of excess liquidity. Corporate bond issuance allowed some financial institutions to engage in partial risk transfers and focus more on regional projects. All the big cats were happy!

Whatever new borrowing which occurred in the corporate sector did not really fuel productive capital expenditure. Bricks and mortar type investments like villa construction do not do wonders to GDP growth after all but this bricks and mortar focus since 2008 when added to excess liquidity certainly created land price inflation rather than CPI inflation but little in terms of growth. It is indeed a paradox that while many small and medium enterprises complain about having access to credit and the need to guaranty everything to get a loan, the system has been flooded with excess liquidity for years.

Many Mauritian firms face liquidity problems in the form of working capital challenges and sub-optimal debt to equity metrics given the return on the capital they can generate. Unlike in more developed markets where private credit and equity markets exist to offer alternative and more flexible forms of financing, Mauritius relies heavily on traditional bank financing. This means that money cannot transmit to businesses effectively. Water everywhere but not a single drop to drink for the poor.

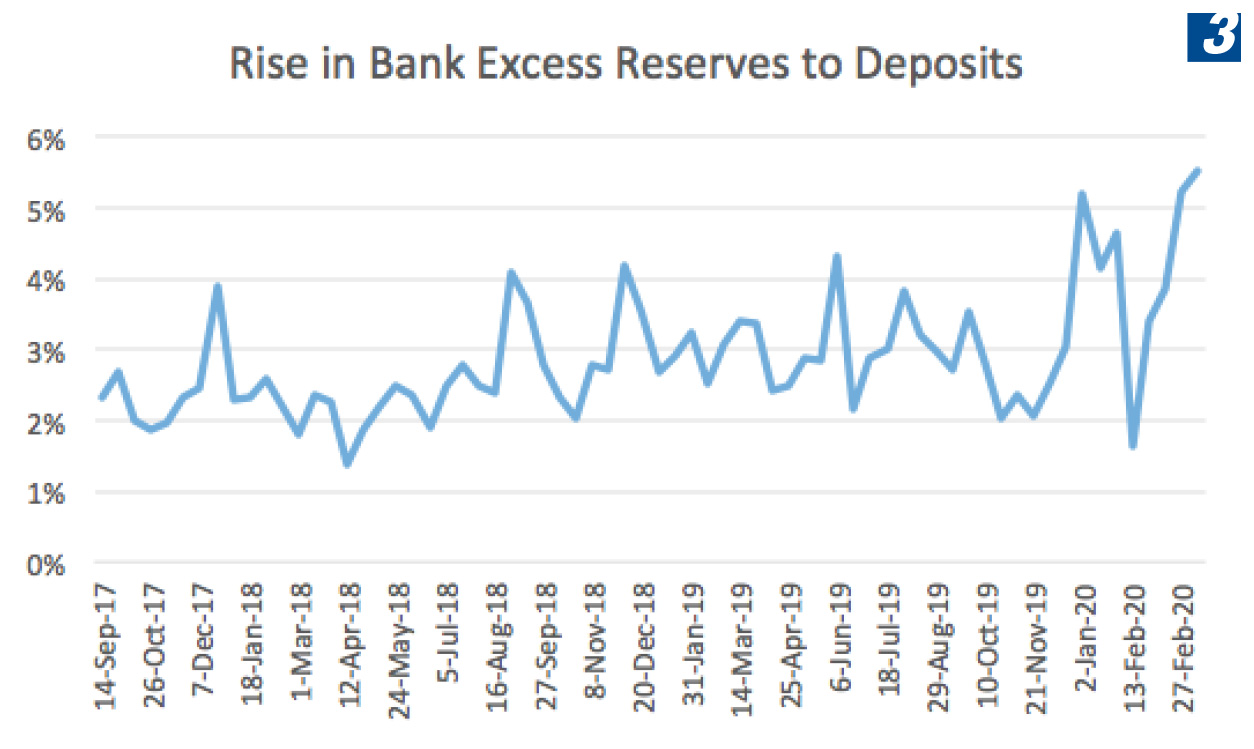

In coming weeks, the velocity of money will trend lower and the output gap will rise ever still as GDP growth slows further while increased risk aversion from banks when it comes to private sector lending will continue to push the money multiplier down as well as the level of excess reserves to deposit ratio increases. There are always pros and cons when it comes to the conduct of monetary policy and it is not as simple to generalize. On top of what I highlighted earlier on unfunded and contingent liabilities, in an environment where banks are more risk-averse, significant increases in locally financed Government borrowing will only serve to crowd out private credit even more during recovery while increasing foreign borrowing will increase austerity demands and credit rating reviews in the medium term.

It is indeed in that context that I proposed that we also think out of the box when it comes to the unconventional monetary policy via the credit channel. The BoM printing, for example, another 5 Billion MUR ideally with parliamentary oversight and BoM Board accountability to transfer to the Government which can then bring equity to an independent and fully accountable SPV which will aim to plug balance sheet holes does not have the same impact on CPI inflation than say printing the money and giving it directly to consumers. The SPV can leverage itself by a factor of 5x by the BoM doing two things.

Firstly, the BoM can issue short term BoM Bills in the market given the level of excess liquidity and then lend long term (10 years) at a higher rate to the SPV and earn the carry. This does not create new money in the system. For the rest, it can overtime on a deal by deal basis do some limited QE and lend to the SPV. The SPV, in turn, will focus on bringing patient capital and flexible financing to viable but currently distressed firms in a credible manner, it will negotiate haircuts with banks and aim to generate decent returns for a cash strapped nation over the investment horizon. This leveraged special situations fund, however, can only be managed by competent people, be accountable to parliament and good governance must be at the core of its operations including Environmental, Social and Governance considerations. If managed badly, a 5x leveraged fund would spell disaster for the country and to the lender, the BoM.

Source: Bank of Mauritius Monthly Statistical Bulletin.

Publicité

Publicité

Les plus récents