Publicité

About the New Income Tax Cure

Par

Partager cet article

About the New Income Tax Cure

The new income tax cure is confusing, regressive and lacks coherence

1. What the Minister of Finance unambiguously stated in his budget speech

At para 223, speaking about the solidarity levy, the Minister declared that ‘The levy of 5 per cent on the excess amount of chargeable income plus dividends of a resident Mauritian citizen will now be 25 per cent and applicable as from Rs 3 Million annually.’

It could not be clearer. First, the solidarity levy is increased from 5 % to 25 %, thus imposing a marginal tax of 40 % on chargeable income above Rs 3 m ( 15 % normal tax and 25 % solidarity tax). Second, the tax applies to resident Mauritian citizens only and not to foreign residents. Third, the threshold is lowered from the current Rs 3.5m to Rs 3 m which means that both the base (more taxpayers) and the depth ( higher rates) have changed. There is no mention whatsoever of the solidarity tax being capped at 10 % of taxpayers’ annual income.

Now the Minister has introduced two changes following a huge outcry from many quarters on both the high increase and the discriminatory nature of the new tax. He wants us to believe that it was never his intention to discriminate against Mauritians and to penalise some income earners with a 40 % tax. Let us be kind and give him both the benefit of the doubt and political expediency to make amends and retract from bad policy choices.

His statements are still not crystal clear. He now says that the solidarity tax of 25 % above Rs 3 m will apply indiscriminately to Mauritian and foreign residents. Which is good as taxation should be based on residency and not citizenship. He also states that there will be a cap on the amount of the solidarity tax payable by a taxpayer at 10 % of his annual income (some want it to be on chargeable income). He also affirms that nobody will pay more than 25 % tax.

2. Progressive tax always means higher marginal tax rates for those with higher income

The economics of public finance teaches us that progressive taxes mean that as income rises, the marginal rate of taxation increases. As a result, the marginal rate of taxation is always higher than the average rate.

Many are making a confusion between average, marginal and effective tax. And this confusion, intended or unintended has led to a distortion in the amended tax system of the Minister. In public finance, the effective rate of taxation is what an individual or a company actually pays compared to the statutory rates. The difference lies in various allowances, deductions and use of fiscal facilities available to bring down the prescribed rate. For instance in global business, a GBC company is liable at a rate of 3 % with the 80 % partial exemption on 15 %. However many pay far less than 3 % by availing of the benefits of the foreign tax credit. So the effective rate becomes lower than the statutory rate. The ‘niches fiscales’ achieve the same result.

A marginal tax rate is instrumental behind progressive income taxes. It is the amount of tax one pays for additional rupees of income. Progressive taxation increases someone's marginal taxes as they earn more money. Each rupee in a new income bracket is taxed at a higher rate than each rupee of the bracket below. In Mauritius, the shift from the 15 % income tax to a 20 % tax in 2017 with the introduction of the 5 % solidarity tax meant that income above Rs 3.5 m was charged at 20 % marginal tax while those below were taxed at 15 %. In the 2020/21 budget, the Minister of Finance has raised the marginal tax from 20 % above Rs 3.5 m to 40 % above Rs 3 m. After the outcry, he is limiting the payment of the solidarity tax of 25 % to a maximum of 10 % of annual income. The average tax is not as important as the marginal tax in a progressive system. All countries look at the brackets of income and the marginal rates to determine the fairness, efficiency, simplicity and competitiveness of a tax system.

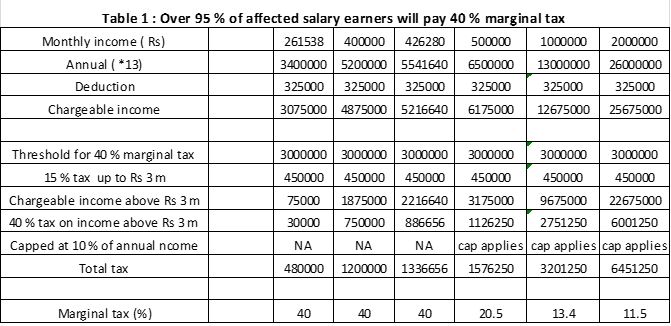

The new proposal of the Minister to cap the solidarity tax payment at 10 % of annual income is unfair to around 95 % of the high-income earners who draw a salary of between Rs 3 m and Rs 5 .5 m per annum ( the analysis is different for dividends). It is perverse as it lowers the marginal rate of taxation to 13 % for someone earning Rs 1m per month while taxing an employee with Rs 425000 per month at a marginal rate of 40 %. This is very regressive.

I have used the putative examples from the Ministry of Finance that appeared in l’Express of yesterday to illustrate this anomaly.

More than 95 % of employees who draw more than Rs 3 m per year are below the bracket of Rs 5.5 m. I give three examples where the 40 % marginal tax kicks in as the 10 % of income do not apply. And three examples where 10 % is applicable.

The anomalous outcomes are as follows

- A person earning Rs 261538 per month will end up paying Rs 480000 total tax. His marginal rate of taxation remains unchanged at 40 % as per the budget of the Minister;

- Someone on Rs 400000 per month will pay Rs 1.2m of the total tax. His marginal tax stays at 40 %;

- An employee drawing Rs 426280 per month will pay Rs 1.3 m of tax. His marginal tax is still at 40 %. This is the salary where the switchover from 40 % marginal tax to 10 % of annual income bites in;

- For salaries of Rs 500000, Rs 1m and Rs 2 m per month, the marginal rate of taxation declines considerably from 40 % to 20.5 %, 13.4 % and 11.5 % respectively because of the cap;

- We also have the anomaly of a marginal tax (20.5 %,13.4 % and 11.5 %) being lower than the average tax ( 25 %) . This can’t happen in a progressive taxation system. It must be the unique country in the world in that unenviable predicament.

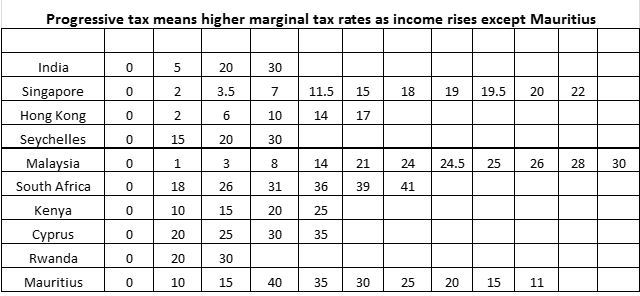

3. Only a country with a falling marginal tax in a progressive system

The Minister mentions India with a tax of 30 % while his tax is capped at 25 %. He is utterly wrong as he is confused between average and marginal taxes. And also with effective tax. As shown in table below, India does not have an average tax of 30 %. It is the marginal rate that is at 30 % which should compare with the 40 % levied on those earning between Rs 3m and Rs 5.5 m and not on someone with Rs 26 m per annum. This confusion leads to distortions in our taxation system.

The table compares the tax of the Minister with what exists in comparator countries.

Four striking features should be noted

i) Our serious competitors to attract investments such as Singapore and Hong Kong have mildly progressive taxation with many more tax brackets than Mauritius. 11 for Singapore and 6 for Hong Kong and it rises gradually. In Mauritius the increase from 15 % to 40 % is very abrupt;

ii) Countries such as Malaysia, Seychelles, Kenya, Rwanda and Cyprus have progressive taxes that are not as steep as the 166 % sudden rise from 15 % to 40 %. This excludes the additional CSG tax of 6 %;

iii) All the other countries have a rising marginal tax as income increases. This is the very definition of a progressive tax. Here it rises initially to 40 % for income in excess of Rs 3 m to Rs 5.5 m per annum than declines sharply to 11 % for those earning Rs 26 m per year. Simply outrageous;

iv) The system creates multiple marginal taxes after Rs 3 m of chargeable income. Over 30 marginal taxes depending on income.

4. The Minister should mitigate the emerging economic crisis and set his pride aside

The Minister is in a hole. And the country. He should stop digging furiously. He is bright to know that his taxation policy is not fair, efficient, simple and competitive. He should show maturity and responsibility and amend it in a very simple manner consistent with best international practices. He has already lowered the threshold of the 5 % solidarity tax from Rs 3.5 into Rs 3 m. Essentially a 20 % marginal tax that applies at a lower income that will bring more taxpayers in that tax bracket. He could keep this 5 % solidarity tax (20 % marginal tax) for chargeable income plus dividends from Rs 3 m to Rs 3.5 m . Then raise the next rate to 7.5 % (22.5 % marginal tax) for income between Rs 3.5 m to Rs 5 m and 10 % ( 25 % marginal tax) beyond Rs 5 m. The tax system will be progressive at 0 %, 10 %, 15 %, 20 % ,22.5 % and 25 %. Look at how Singapore and Malaysia do it above. If we add the CSR and the CSG, the burden rises.

The Minister seems to be fond of academics. Arthur Laffer predicted that too high a tax will lower tax revenue. Some will be discouraged and will not work hard, others will not invest, many will avoid taking risks while the favourite hobby will become tax planning, avoidance and even evasion. It is already in full gear. Let us hope that informed judgement and common sense will prevail over pride and prejudice.

Dr Rama Sithanen

Publicité

Publicité

Les plus récents