Publicité

Who’s afraid of debt?

Par

Partager cet article

Who’s afraid of debt?

Since the advent of the Covid pandemic, interest rates worldwide have dropped to rock-bottom, while government debt ratios have risen globally by an average of 15 percentage points. Major concerns have been expressed about the record level of public debt in Mauritius, currently around 100% of GDP, and the associated risks to financial stability and growth. This article reviews government’s and other assessments of our debt situation.

Moody’s Debt Rating

In March 2021, Moody’s downgraded the sovereign credit rating of Mauritius on account of the deterioration in its debt metrics, and warned that a stronger deterioration would lead to a further downgrade. Like most international debt comparisons, Moody’s focuses on government debt, not public sector debt.

Moody’s expected government debt to stabilize at the estimated level of 80% of GDP in June 2021, upon a growth recovery. However, the actual government debt to GDP ratio in June 2021 is already higher at 90%, based on the latest revised GDP and excluding a small debt consolidation item. Including the debt of public enterprises which accounts for 9% of GDP, the public sector debt ratio anticipated by Moody’s in June 2021 is 89%, against an actual figure of 99%.

For Moody’s, Mauritius’ debt burden is considered high relative to similarly rated peer countries. The median debt-to-GDP ratio for Baa-rated countries was only 54% in 2020 and is projected to reach 58% in 2022. Moody’s highlight government’s fiscal policy response to the Covid pandemic as one of the largest among its rated countries, and reckon that slower than expected growth, larger fiscal deficits and rising inflation would increase the likelihood of another credit rating downgrade.

Moody’s also underline the country’s external vulnerability owing to the large offshore financial sector which contributes to finance the relatively large current account deficit. A reversal of capital flows, as may arise from a tightening of global monetary policies, could threaten financial stability and raise fiscal risks.

IMF DSA

The recent IMF country report on Mauritius carried a Debt Sustainability Analysis (DSA), which concluded that public debt appears sustainable, but at an elevated level, and subject to notable vulnerabilities. Under the IMF baseline scenario, the public debt ratio will likely stabilize as the economy recovers, but will leave the country highly susceptible to potential future shocks.

Since there is little room to absorb additional shocks, public debt should therefore be put on a downward path in the medium term to reduce fiscal risks. In the IMF’s view, fiscal reforms to raise revenue and contain spending will therefore be necessary in the aftermath of the pandemic. A crucial element of fiscal adjustment, according to the IMF, is to reduce the gap between pension spending and revenue.

The IMF DSA was conducted prior to the 2021/22 budget, and the public debt ratio was projected to stabilize at around 93% after 2023/24. In a post-budget supplementary note, the IMF revised its projections for 2021/22, with a fiscal deficit ratio higher by 2.5 percentage points, and a public debt ratio higher by 7.4 percentage points in June 2022.

The IMF note states that “Given the substantial increase in the public debt level compared to the staff report and increased risk to debt sustainability, stabilizing the debt-to-GDP ratio in the medium term will require greater fiscal consolidation effort, and the stabilized public debt level will likely exceed 100 percent of GDP.”

Govt MTMF

Despite the sizeable increase in the debt to GDP ratio, government holds that ‘the current debt level is still at a manageable level’. In the 2021-22 budget estimates, government presented a medium-term macroeconomic framework (MTMF) and a fiscal and debt management strategy to bring down public debt to just over 80% in June 2024.

However, the MTMF’s three-year fiscal projections do not appear to be realistic and reflect a lack of adherence to fiscal accounting standards. Future budget revenue is artificially inflated, including by a transfer of some Rs8 bn from public corporations, including CEB, STC and MPA, in 2021/22.

Budget revenue in 2020-21 was similarly boosted by a BoM transfer of Rs60 bn, whereas IMF asserts that “Following the IMF’s GFS Manual 2014, Sections 5.111, 5.116, the transfers from the BOM to the Central government are considered as financing”. Statistics Mauritius has since corrected its fiscal data by treating the BoM transfer as an equity drawdown, not as revenue. The concocted fiction of a balanced 2020/21 budget has finally been laid to rest.

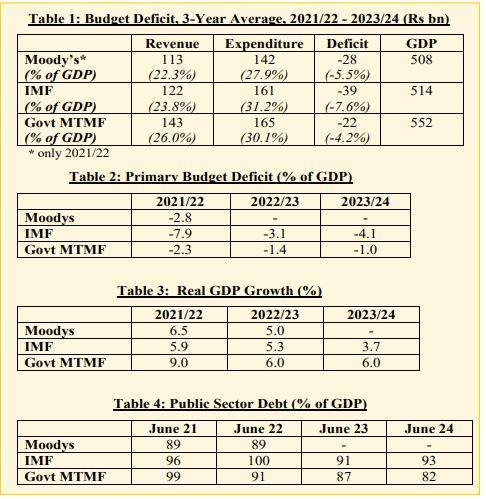

Compared with IMF projections, MTMF overestimates budget revenue and underestimates budget expenditure to end up with a lower budget deficit, as shown in Table 1. For the next three years, MTMF revenue averages 26% of GDP, or about 2 percentage points over the IMF forecast. MTMF expenditure averages 30% of GDP, or about 1 percentage point below the IMF. The MTMF overall and primary fiscal deficits (the latter excludes interest costs) are projected at an average of 4.2% and 1.6% of GDP respectively, lower than the corresponding IMF figures by over 3 percentage points.

Projected MTMF fiscal deficits are nevertheless higher than recorded in pre-Covid years. Expenditure is permanently higher, as the expected winding down of Covid- related wage and income support, estimated at over Rs13 bn by the MRA in 2020/21, will be more than offset by (i) rising social benefits from the planned pension increase in 2023/24, and (ii) greater employee compensation following the PRB award. These two items alone will account for over 60% of current spending in 2023/24.

Projected primary budget deficits, GDP growth and public debt ratios by government, IMF and Moody’s over the next three years are shown in Tables 2-4. MTMF aims at a reduction in the public debt ratio by 17 percentage points from 99% to 82% in June 2024. Compared with the IMF DSA forecast of a stable debt ratio, the projected lowering of the debt burden by MTMF partly results from a lower primary deficit, but derives primarily from stronger economic growth. MT- MF real annual GDP growth averages 7%, higher than the corresponding IMF figure of 5%.

Growing out of debt

The MTMF nominal GDP in 2023/24 is forecast at Rs606 bn, or about 8% higher than projected by the IMF in its latest World Economic Outlook of Oct 2021. GDP growth in the next 3 years is predicated on a major boost in public investment, which is however not borne out by Govt’s own data. The estimate of total public investment of Rs50bn in 2021/22 is similar to estimates of previous years, with actual investment invariably showing a shortfall.

Besides, greater public investment does not directly lead to significantly higher value-added growth, especially in the short run, due to the relatively high import content of public infrastructure works. In 2019, public investment reached a peak of 5.3% of GDP, while GDP growth slumped to 3%. Wasteful public spending and the costs of corruption can also have significantly adverse impact on overall growth.

The labour force is declining, and labour productivity gains are on a long-term downward trend. A sizeable part of the economy is stuck with low productivity activities in the informal and public sectors, as well as in industries dependent on cheap foreign labour. Capital productivity and the capital labour ratio have been stagnant for a decade. Investments are not sufficiently capital-deepening and are concentrated in the real estate sector which is not considered to be very productive.

In its latest review of the economy, even MCCI comments negatively on investments in real estate, noting that “the bulk of the FDI is directed towards schemes which do not generate much value addition to the economy and focus should be on attracting FDI in productive sectors that are growth driven and generating employment”. Without productivity-enhancing investments and structural reforms, the economy cannot hope to significantly raise its growth potential. The failure to address the productivity issue has been a critical shortcoming of our social and development policies.

In the likelihood of slower real GDP growth, the best outcome is that the public debt ratio can be stabilised at close to 100% of GDP. Both the IMF DSA and the MTMF do not reflect the recent sizeable rupee depreciation and its impact on foreign currency debt. Following a sharp recent acceleration in the year-to-year CPI increase, and the rise in global energy and other commodity prices, domestic inflation is also expected to be much higher than projected. These latest developments indicate greater financial instability ahead.

Special funds

Extra-budgetary Special Funds (SF) obfuscate the true extent of budget deficits, as these funds were mostly designed for use in relation to the electoral cycle. Transfers from the budget to SF in earlier years are accumulated to be spent later as general elections get closer. SF now extend wage and income subsidies as well as subsidies for housing construction, undertake major capital spending programs, and their revenue includes a petroleum levy.

Following massive budget transfers made in the last two years, SF surplus balances in June 2021 stood at Rs35 bn, or 8% of GDP, and will be used to fund SF expenditures in the coming years. In 2021/22, SF expenditures are estimated at close to Rs26 bn, or over 14% of total budget spending. SF represent a fiscal black box and it is unacceptable that interim statements of accounts of SF are not available to the National Assembly annually with other budget documents. Inclusive of SF spending averaging 2% of GDP, consolidated expenditure is projected to exceed 30% of GDP in the coming years. During the decade up to 2018/19, consolidated expenditure amounted to only 25% of GDP. The scaling-up of consolidated expenditure from 25% to 30% of GDP sums up the new post-Covid fiscal configuration, and points to the crucial need for fiscal correction to limit a range of fiscal risks.

Fiscal risks

Macro-fiscal risks stem from adverse and unexpected changes in macroeconomic indicators, such as a growth slowdown, rising interest rates, a wider current account balance, a disruption in capital flows, and a larger fiscal deficit. Fiscal shocks also originate from large financial outlays not accounted for in official budgeting. Official budget deficits under-estimate borrowing needs by not including loans extended and equity injected to public sector bodies. Govt equity and loans often serve to finance off-budget spending or meet contingent liabilities, such as bail-outs of failed financial institutions or companies.

“Muddling through with populist policies to win elections will inevitably reach a foregone conclusion, as inflation takes hold, reducing purchasing power and the real value of debt along with pensions, weakening growth, and increasing poverty, inequality and social instability.”

Recent examples include (i) equity injections into the National Property Fund, of close to Rs12 bn in 2020/21, to cover bail out costs of the BAI Group, with an additional Rs4 bn projected in 2021/22, (ii) equity investments in companies such as Cote d’Or Multisports complex, and Metro Express for off-budget spending, as well as (iii) loans, effectively subsidies, to non-performing public bodies such as the Wastewater Management Authority. An unbudgeted loan of Rs12.5 bn to bail out Air Mauritius has just been announced, with surely plenty more to come.

Loans, equity and the acquisition of other financial assets by Govt are estimated to reach a total of Rs15 bn in 2021/22, representing 3.6% of GDP. These financial expenses averaged about 1% of GDP in the last 3 years. Focusing solely on the official fiscal deficit, interest rates, and growth can be misleading. Other debt-creating financial flows also carry serious fiscal risks.

Govt is often forced to meet the uncovered losses and obligations of extra-budgetary agencies, state-owned companies and large private enterprises, and other politically significant institutions. Besides capital injections to deal with the financial troubles of Air Mauritius, a range of contingent liability risks will weigh heavily on the future course of public debt, including from quasi-equity investments of the MIC, the funding of huge deficits on the employee pension schemes of some public corporations, and the hidden and unforeseen costs of PPP arrangements.

Flexible debt policy

Despite the recent critical debt evaluations by the IMF, World Bank, and Moody’s, Govt dismisses any debt worries and carries on spending without restraint. The public debt limit of 60% of GDP under the Public Debt Management Act has been scrapped. The Minister of Finance responds to criticisms on the excessive debt burden by pointing to the low cost of debt, and keeps citing Olivier Blanchard, a former IMF chief economist, on the debt problematic.

According to this policy view, record low interest rates in advanced economies expand the scope for expansionary fiscal policy, and high public debt appears to be more sustainable. A situation where interest rates are lower than GDP growth, i.e., a favorable interest growth differential, puts less pressure on the ratio of public debt to GDP. A lesser emphasis on the debt ratio and debt sustainability is therefore considered appropriate.

A reduction in the debt ratio is normally achieved by a positive interest growth differential and by running a primary fiscal surplus. A key insight of this debt analysis is that if the interest growth differential remains favourable in future, then a country’s debt ratio can be stabilized at its current starting level, even if running a primary fiscal deficit.

However, even when a high public debt ratio is stabilised, the critical issue is whether it is sustainable, which depends on future outcomes on interest rates, growth rates and primary fiscal balances, as well as other debt-creating flows. A debt sustainability analysis does not depend only on the cost of debt.

The Minister of Finance misread Blanchard when he stated in the National Assembly on 22 June 2021 that “Olivier Blanchard a expliqué de manière irréfutable qu’être obnubilé par la réduction de la dette publique est une erreur. Il a fait la démonstration qu’il est contre-productif de se focaliser sur le ratio de la dette par rapport au PIB, plutôt que sur sa soutenabilité, c’est-à-dire in fine, sur le cout de la dette.” In fine? Expressing debt sustainability simply as the cost of debt is plain wrong.

Because money is super cheap does not justify Govt spending without limit, especially in developing economies, as Blanchard himself makes clear in a recent paper – “There is no question that favourable interest-growth differentials make any public debt situation less worrisome, for both advanced economies and emerging markets. But there are still limits to how high debt can go, and these limits are tighter in emerging markets.” Debt sustainability limits still matter. Although low interest rates and high debt ratios may seem to reflect a new normal situation, the need for evaluating debt sustainability cannot be discarded.

Calling Blanchard to the rescue repeatedly to minimize debt concerns is a delusion. The comparison often made with the exceptionally high debt ratios of some advanced countries, like Singapore or Japan, is equally absurd. Singapore issues Govt debt to provide savings instruments for pension and other investment funds, not for fiscal purposes. Japan is one the world’s most indebted countries, struggling to emerge from a long period of low growth and deflation, but it has a reserve currency, runs current account surpluses, and holds massive foreign exchange reserves.

A sensible comparison should be made with emerging market countries, excluding oil producers, which show a Govt debt to GDP ratio of 65% in 2021, against 90% for Mauritius. Their debt ratio increased over the pre-Covid level by 10 percentage points, while the corresponding increase for Mauritius was 16 percentage points.

Fiscal credibility

While the post-pandemic norms of public spending and debt will likely be more flexible, the dangers arising from unchecked deficits and debt remain, due to our vulnerability to sudden domestic or global shocks. Mauritius needs to strengthen its debt sustainability through fiscal consolidation and create wider fiscal space to withstand future economic disturbances.

Another Moodys downgrade to a notch above investment grade would be highly destabilizing, especially for the banking sector. Public finances must therefore be put on a sounder footing, especially by reviewing our profligate spending. Pension and other structural reforms are essential to ensure a sustainable debt level, and to provide fiscal space for coping with future emergencies.

As previously recommended, the ideal strategy to deal with the high debt level would be to enter into an IMF-supported program, as a signal of firm commitment to fiscal sustainability and to secure our credit rating. Few would recall that the IMF helped to successfully engineer an economic recovery in Mauritius four decades ago, marking a crucial turning point in the country’s economic fortunes. Moreover, the IMF of current times is perceived as an institution less wedded to economic orthodoxy and more amenable to dialogue.

Pending a full growth recovery, Govt can initiate actions towards building up fiscal credibility, by providing a road map for fiscal adjustment, and the restoration of fiscal rules, with improvements to promote greater fiscal discipline and transparency. The setting up of an independent institution such as a Fiscal Council to ensure better compliance with fiscal rules and transparency standards may assist in fostering greater fiscal responsibility.

Addressing inefficiencies and corruption in public spending has become increasingly urgent, which requires a thorough review of its public investment management processes for greater transparency, effectiveness, and accountability. The drift towards a kleptocratic state is unmistakable, and better fiscal governance systems are sorely needed. Record debt, reckless spending and rampant corruption are the basic ingredients needed to spawn a debt crisis.

Conclusion

Growing out of debt without structural reforms is wishful thinking. There is no alternative to fiscal restraint for tackling the debt burden. Muddling through with populist policies to win elections will inevitably reach a foregone conclusion, as inflation takes hold, reducing purchasing power and the real value of debt along with pensions, weakening growth, and increasing poverty, inequality and social instability.

Government could still choose to default on its rupee debt through higher inflation fuelled by currency depreciation, rather than face the negative political impact of undertaking fiscal adjustments. In mortgaging our future for the present, the most likely outcome is default through inflation. A debt crisis scenario may be preparing to unfold.

Publicité

Publicité

Les plus récents