Publicité

Magical wand or fiscal skullduggery

Par

Partager cet article

Magical wand or fiscal skullduggery

- Introductory remarks

Surging inflation, unprecedented rises in the prices of oil, gas, food, and medicines have devastated the pur- chasing power of people, leading to a spike in poverty level and a sharp rise in cost of living. Government had to embrace measures to restore purchasing power. Expectations were very high from salary increases to a higher minimum wage, from raising old aged pensions to lower energy prices, from income support to food vouchers, higher food subsidies to lower income tax. On facts and evidence, the minister has met some of the expectations of the population. Some would argue too late and not enough. Fair debate.

The three flagship measures are:

- the Rs 1,000 monthly increase in wages to all employees and self-employed earning less than Rs 50,000 per month.

- ii) the rise in old aged pensions of Rs 1,000 and Rs 2,000 per month for those between 60 and 65 years and those above 65 years respectively;

- the subsidy of some Rs 4.2 b annually to keep the prices of some products such as ‘pain maison’, cooking gas, rice, flour, milk and few others unchanged.

He has also abolished municipal tax for town dwellers, increased by more than inflation social aid for the vulnerable groups and lowered income tax for the middle income group. To be candid, these are broad based measures that impact almost everybody and everywhere in the country. Many are asking how such ‘populist’ measures can be funded when the Minister clearly told the population that his fiscal space is tight, the war in Ukraine is having severe economic effects and the post Covid recovery is fragile with downside risks. More importantly how has been able to deliver on such a ‘social budget’ while also lowering the bud- get deficit and the debt while increasing expenditures elsewhere?

- Three major funding tools and one big war chest

The Minister has not attempted to contain expenditure elsewhere to help finance his budget. Recurrent expenditure is up by 11.7 % to Rs 154 b. On paper the capital expenditure is lower at Rs 18.4 b from Rs 23.3 b last year. But this is a budgetary illusion as the Rs 23. 3 b includes a massive transfer (not actually spent) of Rs 11.5 b to the Special Funds.

So what has he done? An act of prestidigitation or an underhand manipulation?

Or a bit of both.

- he is overestimating economic growth at 8.5 % for 2022/23 when most expert institutions have a lower figure at around 6 to 6.5 %, especially if the war in Ukraine intensifies and lasts and the risks of slow growth with high inflation affect our main trading partners. Last year he predicted a 9 % growth and he has disclosed an actual lower figure of 6.9 %. He forecast inflation at 4 % and we will end up with 8.5 %. He projected a tourism arrival of 650,000 for the year ended June 2022. At best it will be 550,000. As a result of his very optimistic growth forecasts, taxes are projected to rise by a significant Rs 22 b in 2022/23 to Rs 129.5 b. Rs 15 b more in VAT and Rs 6.5 b more for taxes on in- come and profit. He will also collect Rs 10 b of CSG from employers and employees;

- ii) the Minister has a deficit of Rs 22.9 b to finance. He usually funds it by a combination of domestic and external borrowing. Both domestic and external debts have risen sharply since 2014. If all debts including those in SPV’s are recognized, the debt to GDP ratio is very high at close to 100 %. However, it is declining in relative terms. 49 % of the equity of Government in Airports of Mauritius has been sold for Rs 13 b to the MIC, thus lowering the recourse to debt finance. Even if the absolute level of debt remains very high, its share to GDP will fall as GDP rises in nominal terms ( not in real terms) by around 30 % in the two years ending June 2023 ;

- iii) there is an exceptional financing of the 2022/23 budget deficit of Rs 23 b representing 4 % of GDP. In his two previous budgets, the minister abundantly used the Special Reserves Fund of the Bank of Mauritius, a special transfer of Rs 60 b from the BOM, the MIC fund, the reserves of many enterprises and domestic and external debt to finance the high deficit. In the current year, Government has sold 49 % of Airport of Mauritius to the MIC for Rs 13 b.

Next year he will fund the bud- get deficit of Rs 23 b by disposing of Rs 22 b of public assets. He did not even bother to disclose it in his speech. No mention of which assets will be sold, when, to whom and what valuation. And what happens if the transaction takes longer to materialize or the price is lower than expected. Will he have recourse to more debt? He should be transparent with this huge disposal of some jewels of the crown.

- A parallel budget within the budget : the war chest of Appendix C

The ‘Special and other extra budgetary funds’ constitute a massive war chest for the minister. It has always existed but never on the scale, size and scope used by minister Padayachy.

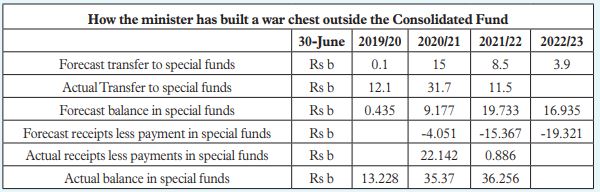

This Special Fund is at Appendix C of the budget. When the Prime Minister presented the budget in 2019, it forecast there would be a small transfer of Rs 100 m to the fund and a very minor sum of Rs 435 m as balance at the end of June 2020. However, even before presenting his first budget in 2020, Minister Padayachy transferred a massive amount of Rs 12.1 b to this special fund and the actual balance at 30th June 2020 shot up from a meagre provision of Rs 435 m to a staggering actual of Rs 13.2 b net of payments as shown in table below.

In his first budget in 2020/21, he intended to transfer another Rs 15 b to that fund, giving a total of Rs 28.2 b available for projects. He projected to spend Rs 19.1 b during that year, thus leaving a forecast balance of Rs 9.1 at end June 2021. However he actually transferred a massive Rs 31.7 b and spent far less than Rs 19.1 b to leave an actual balance of Rs 35.37 b at end of June 2021. A staggering difference of Rs 26.3 b.

In his second budget 2021/22, he forecast to transfer Rs 8.5 b to the Special Fund. However he ended up transferring Rs 11.5 b, thus raising the total amount available to a very high amount representing around 10 % of GDP. He had projected an expenditure of Rs 25.9 b for that year, thus leaving a forecast balance of Rs 19.8 b at end of June 2022.

Same phenomenon again. He actually transferred more and spent less during the year. Instead of a projected balance of Rs 19.8 b at June 2022, he is showing a massive balance of Rs 36.3 b at June 2022 in his budget for 2022/23. He will now transfer Rs 3.9 b to the fund this year. The total sum available to be spent next year is an astronomical Rs 40.2 b. He is expected to utilize Rs 23.3 b to leave a balance at end June 2023 of Rs 16.9 b. Of course, the same higher transfer and lower spendings will take place and the balance at end of June 2023 will be much higher than Rs 16.9 b.

Over three years, the minister has transferred a colossal sum of Rs 55.3 b to these special funds. In all three years he has systematically transferred much more than forecast and spent far less than earmarked.

These expenditures are not included in the Consolidated Fund except for transfer to and from the Special Funds. The minister can arbitrarily decide which expenditure is financed from the Consolidated Fund and which one by the Special Funds. There are six funds under this Special Fund. The two most important ones are the Covid-19 projects development fund with Rs 26.7 b and the National Resilience Fund with Rs 6 b.

As a result of the existence of these two ‘parallel’ budgets, the fiscal deficit has become meaningless as he shuffles the money in these special funds to decide on the exact size of the budget deficit he wants to present. When the deficit in the consolidated fund is low, he simply transfers underutilized fund to the special fund. This does two things. It artificially raises the budget deficit of the consolidated fund for the year while it increases the availability of funds in the special funds for subsequent years. This is exactly what he has done this year to reach a deficit of 5 % of GDP. He has transferred Rs 11.5 b to the special funds. It is not an expenditure. Had he not transferred this massive amount the deficit would be Rs 13.6 b instead of Rs 25.1 b. A deficit of 2.7 % instead of 5 % of GDP.

When the deficit of the consolidated fund is high, he does the reverse transaction. He transfers money from the special fund to the consolidated fund to lower the budget deficit. To avoid such large-scale deceptive tac- tics, the IMF and other institutions have called for a consolidation of all revenues and all expenditures in the consolidated fund. No doubt the minister will refuse. And strongly so. For obvious reasons.

- The minister shuffles and shuttles expenditures between the two funds

It has become so anomalous that the capital expenditure in the consolidated fund is far lower than the monies in the special funds. For 2022/23, the acquisition of non-financial assets is estimated at Rs 12 b while the special funds has Rs 40 b to spend. The tail is wagging the dog. The minister decides which expenditure will be in the Consolidated Fund and which one in the Special Fund. At times, the same type of project is financed from both funds. The ministry of Housing has a budget of Rs 1.4 b for social housing development. In order not to post a high deficit, the 12,000 social housing units are however funded through the Special Fund. Equally the budget for tourism promotion which is clearly a recurrent expenditure does not feature in the budget of the Ministry of Tourism but in the special fund at Rs 525 m.

What this means is that the minister has currently Rs 40 b that he can choose what to do with because of the construct of the special funds and the fact that he can transfer between the consolidated fund and the special fund as and when he so wishes.

There is also heavy underperformance. There was a forecast expenditure of Rs 4 b in 2021-22 to construct social houses. Only Rs 100m has been spent and no houses built. The national flood management programme was to spend Rs 3.6 b. Only Rs 800 m has been used. He had earmarked Rs 1 b for the development of vaccines. Actual spending is only Rs 100m.

So, the same money is recycled year in, year out. Underspent amount from the capital budget is transferred to these special funds and these special funds in turn largely underperform. Then this accumulated sum is used to finance some recurrent expenditure. Such as the annual contribution to the MTPA (Rs 525 m next year), EDB schemes (Rs 500 m), support to planters and farmers (Rs 1.4 b). All these are recurrent expenditures that should feature in the Consolidated Fund but are not. It looks like an unsustainable scheme as the sys- tem only works when the capital budget and the special funds show huge underspending and some of these funds are used to finance recurrent expenditures.

- Funding the additional social costs of the budget

The overall costs of the Rs 1,000 and Rs 2,000 per month to pensioners would be around Rs 5.3 b per year while the expenditure for the Rs 1.000 per month wage support for employees and self-employed earning less than 50,000 would be around Rs 4.2 b.

The subsidy on flour, rice, coo- king gas and pain maison is likely to be almost fully funded by the special levy on petroleum products outside the budget. So the two key measures of higher pension and the wage support of Rs 1,000 would cost around Rs 9.5 b per annum.

While it does not make economic and financial sense to finance recurrent expenses with funds essentially ear- marked for capital projects, this is in fact what is taking place. With the unhindered transfer from the consolidated to the special fund and the inability of Government to implement capital projects in a timely and effective manner. The challenge will happen when funds ear- marked for projects are actually spent. However, that will take a long time.

In the meantime the show will continue with massive underspending in both the capital budget and the special funds. The war chest has accumulated Rs 40 b representing the equivalent of over four years of funding the additional costs of pensions and the wage supplement.

With such war chest, the minister could easily have decreased the price of petroleum products by around 10 % as there are huge sums in the special funds.

Equally he could have easily funded a compassionate income support or food vouchers for 100,000 families worth Rs 2,000 per month per household. That would indeed have been a budget «for the people, with the people» and also «by the people»; and Stiglitz would have been enthralled about this «shared prosperity».

Especially as it would be almost impossible to spend Rs 10.5 b on social housing in the next two years as per Appendix C when only Rs 100 m has been used this year.

Equally, it is very unlikely that Rs 11.3 b will be actually spent on national flood management in the next two years when only Rs 800 m have been disbursed this year.

But he has two more budgets to deliver. He must keep his war chest flush with monies. Herein lies the answer to the question of financing the social measures.

For the Minister, not only is money fungible, it can also be easily shuttled and shuffled. So the financing of the social measures is certainly not a magical wand. More of a fiscal skullduggery.

Publicité

Publicité

Les plus récents