Publicité

September blues: chronicle of a pounded and wounded pound sterling

Par

Partager cet article

September blues: chronicle of a pounded and wounded pound sterling

Prologue

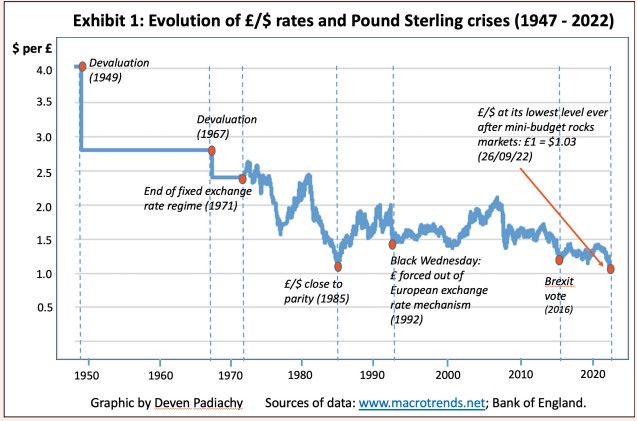

September 2022 has been an extraordinary month for the United Kingdom (UK), to say the least. The installation of a new government was followed by the sudden death of Queen Elizabeth II, after which a monetary catastrophe of epic proportions dubbed “The biggest UK bond & currency market sell-off in history” began to unfold. This article focuses on the main protagonist, namely, the ‘exchange rate of the British pound sterling against the U.S. dollar’ (GBP/USD) which has been on a roller coaster since the 22nd.

Actually, evidence shows that the UK economy is accustomed to September blues. Black Wednesday, for instance, was on 16th September 1992. The too-big-to-fail U.S. investment bank Lehman Brothers collapsed on 15th September 2008, sending shockwaves through the global financial system, with cataclysmic financial consequences in the UK.

Now, in September 2022, no sooner had the UK sworn in a new government and a new monarch than its national pride took an unexpected hit. The Pound was pounded heavily by international investors amidst a ferocious market panic on the 23rd and the 26th. GBP/USD fell to an all-time low (£1 = $1.033, see Exhibit 1) before gaining ground later on, while UK government borrowing costs (interest on bonds) skyrocketed to their highest levels in more than a decade (well above 4%, compared to less than 1% in January). The UK was like a rabbit caught in the headlights. The wounds to the pound were severe and humiliating, reminiscent of Black Wednesday (see further below) almost exactly 30 years ago. As we write these lines, there is no clear indication that the drama is over. The pound has improved in value but not in outlook. The whole story is still developing amidst global uncertainty, deteriorating economic outlook, and geopolitical tensions.

What went wrong? How did it all unfold?

Four key dates are to be retained: September 6th, 22nd, 23rd and 26th.

• Tuesday 6th: A new government was sworn in, with a new Prime Minister and a new economic team boasting they could fix the British economy and provide relief to the population. However, even though their bold reform agenda (now nicknamed Trussonomics, given its similarity with the Reaganomics approach of the 1980s) sounded hopeful and ambitious, no details were released apart from vague statements on tax-cuts, supply-side stimulus, and energy support packages for households and businesses. Impact effect: Markets were unimpressed but remained vigilant.

Two days later, news of the Queen’s demise took the country by storm. As a mark of respect, the UK economy operated at a go-slow pace till Tuesday 20th. Despite its urgency, the hike in key interest rate by the Bank of England (BOE) scheduled for the 15th was delayed to the 22nd. Markets remained patient throughout, exceptionally.

“The wounds to the pound were severe and humiliating, reminiscent of black wednesday almost exactly 30 years ago.”

Thursday 22nd: The BOE finally announced its key interest rate decision. It disappointed markets with a raise of ‘just’ 50 basis points (bp). Investors were desperately expecting the BOE to match the moves of the Federal Reserve System of the U.S. (the Fed) and the European Central Bank (ECB), which had raised rates by 75bp days earlier. Result: The pound lost 0.6% immediately after the hike, revealing growing signs of nervousness on financial markets.

Friday 23rd: This was the day when the straw broke the camel’s back. Yet, it was sup- posed to be the new Chancellor of Exchequer Kwasi Kwarteng’s big economic moment. He was tasked to present a mini-budget to unveil the new government’s ‘Growth Plan 2022,’ designed to “make growth the government’s central economic mission.” Unfortunately, the whole exercise turned out to be a fiasco. First, the mini-budget was anything but “mini.” It was actually the biggest shake-up to the British tax system in 50 years, with a £45 billion package of sweeping tax-cuts, expected to be largely unfunded (i.e., financed via borrowing). Then it was revealed that the Office for Budget Responsibility (OBR), UK’s independent fiscal watchdog, was not invited to scrutinise the mini-budget prior to its presentation.

• The other key announcement which created an uproar was the Energy Price Guarantee scheme, estimated to cost some £60 billion over next six months to limit the impact of higher energy prices on consumption. Cri- tics argued that the design of the scheme was flawed not only because it would favour those who consume more but also because it would be “pegged” to wholesale prices, implying its cost could skyrocket if energy prices spiralled internationally.

• These two flagship measures failed the credibility test on the same day, the minibudget being qualified as ill-designed, costly, inflationary, skewed disproportionately in favour of the better-off, and self-defeating. Investors questioned government’s strategy to embark on a binge of extra borrowing exceeding £400 billion at increasingly ex- pensive rates, fearing it could cause a deterioration in public finances, higher inflation, and a threat to UK’s long-term growth prospects.

• Outcome of the day: market reaction was seismic as investors slammed the British government’s bet on a risky economic strategy, triggering massive sell-offs of the pound and bonds. GBP/USD crashed to its lowest level in 37 years at $1.085 (down 3.6%).

Monday 26th: Adding insult to injury on Sunday 25th, perhaps out of naivety, Kwarteng doubled down and announced that additional tax-cuts were on the agenda. This caused more panic selling as soon as markets opened on the 26th, investors pounding the Pound further, dragging it to its lowest level ever against the dollar (close to $1.03). By then, it was clear something was rotten and that, should the Treasury continue to ignore market sentiments, the UK would run the risk of being in serious trouble.

Since the 26th, the Treasury and the BOE have been treading carefully. The pound has recovered slowly to its pre-crisis level. However, the fear that the worst could yet materialise in the coming weeks is palpable. The possibility of a situation of GBP:USD parity before end of 2022 (or even below-parity) has begun to haunt the Treasury.

“The office for budget responsibility, UK’s independent fiscal watchdog, was not invited to scrutinise the mini-budget prior to its presentation.”

Lessons learned: four gaffes which could have been avoided

Many analysts believe the September blues afflicting the UK are largely self-inflicting, some even pinpointing one man for that matter. Could it have been otherwise? With 20/20 hindsight, we can now identify at least four ‘gaffes’ which could have been avoided by the fiscal and monetary authorities during the past week. These are:

- Magnitude of the rate hike on the 22nd: It is widely acknowledged that BOE’s move (50bp) was timid and well below market expectations. Besides, and strangely enough, BOE was lagging behind on the monetary calendar. The Fed had already hiked interest rates five times since March 2022. BOE also feigned not to realise that its next Monetary Policy Committee (MPC) meeting would only be on November 3rd. By that time, both the Fed and ECB would have had the possibility to shift gear again, thus strengthening their currencies against the pound.

- Proof of fiscal prudence and costing of the growth plan: Investors fail to understand how such a bold Growth Plan, which would exceed £400 billion of additional borrowing over the next five years, could be devoid of any fiscal strategy and economic projections. That the OBR was intentionally ignored, probably to avoid an independent scrutiny of the mini-budget, dented the credibility of the Treasury. It was only after investors had massively rejected the plan that Kwarteng finally acknowledged that a properly costed plan should have been published to shed light on his long-term spending plans.

- Lack of synergy between Treasury and the BOE

Both institutions were perceived to be operating in silos, with conflicting objectives. Whilst the BOE’s immediate focus was to tighten monetary policy to contain inflation (which has reached nearly 10%), Kwarteng’s budgetary measures were feared to be highly inflationary, impacting negatively on interest rates, and posing a threat to consumer confidence. Intense pressures from investors did compel the BOE to issue a statement on the 28th to calm markets but this fell short of expectations as its credibility had already been undermined.

- Lack of sensitivity and effective communication, undermining credibility

Both Prime Minister Truss and Kwarteng have been accused of lacking sensitivity in their approach and treating in a cavalier manner the institutions set up to safeguard the economy against political influences. It was only after being punished severely by investors and getting a rebuke from institutions such as the IMF, Moody’s and even the US Treasury that Kwarteng finally accepted the idea of bringing the independent OBR on board. Investors had to rely on outside sources and think-tanks in order to properly understand and evaluate the implications of the mini-budget. An effective communication strategy would have gone a long way towards preventing panic on a global scale.

The good news is that these lessons seem to have been well understood. The bad news is the Treasury’s resistance to review and downsize the tax-cuts plan and moderate its appetite for excessive borrowing. It might not do so until another brutal wake-up call from the markets…

“The bad news is the treasury’s resistance to review and downsize the tax-cuts plan and moderate its appetite for excessive borrowing.”

Come October, can the UK beat the blues? Events and indicators to follow:

So, now that the cat is out of the bag, what could we expect next for GBP/ USD in the next quarter? Murphy’s Law at its loftiest (leading to an episode of GBP:USD parity) or the UK beating the blues (with a review of the Growth Plan to provide comfort to all stakeholders?) All bets are off. However, the be- low events and indicators could be used as guide to monitor and track the GDP:USD trajectory.

- In October 2022 Key events to watch:

• ECB’s Monetary Policy meeting in Frankfurt (27th October), when a major interest rate hike is anticipated;

• Release by Kwarteng of the full economic forecast issued by the OBR, UK’s fiscal watchdog, by the end of October;

• Possibility of an emergency unscheduled BOE intervention to (i) Hike interest rates before 3rd November (low- to medium-probability); and (ii) Buy back government bonds (medium probability); and

• Release of UK GDP and Housing figures (providing a snapshot of growth and consumer confidence).

- In November 2022

November is expected to be an eventful month, which could determine the trajectory of GBP/USD in 2023. Key events include:

• Fed’s FOMC meeting on 2nd November (whereby a hike in interest rate is almost certain);

• BOE meeting on 3rd November (which will bring about a major raise in its key interest rate); and

• Kwarteng’s full budget presentation on 23rd November, which is expected to improve the bombshell version released on 23rd September. It could be a make or break situation for the Truss government and the value of the pound in 2023.

Historical review: Black Wednesday and other pound sterling crises It is probably true to say that last Monday (26th September) was a watershed moment in the pound’s history. However, it is certainly not the worst crisis in terms of media sensationalism, global impact and, above all, humiliation, not only for the pound but for the Bank of England as well. That one occurred thirty years ago on 16th September 1992, a day infamously known as Black Wednesday. GBP:USD didn’t reach its lowest level (see Exhibit 1) but the pound was brutally forced out of the then European Exchange Rate Mechanism (ERM) following a massive speculative onslaught by currency traders, notably the notorious George Soros.

The BOE was unable to defend the pound for an extended period and ultimately gave up. Soros, who had amassed a short position of more than £10 billion, ended up making a profit of over £1 billion. He has since then earned the title “The Man who broke the Bank of England.”

Other notable crises of the pound include (see also Exhibit 1): The Brexit Vote in 2016 (8% drop in value following the vote to leave EU); The Strong Dollar Policy of the U.S. in the 1980s (crushing the pound to a record low of $1.05 in 1985, down from $2.30 in 1980); The Sterling Crisis in 1976 (prompting the UK to borrow $3.9 billion from the IMF to stabilise the value of the pound, which represented the largest loan ever provided by the IMF. It was also a humiliating experience for the UK as a lea- ding developed country to knock at the doors of the IMF); The 1967 Devaluation (14%); and the Sterling Crises of the late forties (after the pound became convertible to dollars.)

Conclusion

Far from being out of the woods, the British pound sterling’s fate has yet to be decided. So far, since Kwarteng released his cluster bomb on 23rd September, the pound has improved in prices but by no means in outlook. Interestingly, the Treasury and the BOE have, by now, seen the writings on the wall and have suffered enough rebukes to hopefully align views and adopt a concerted approach for UK inc. As days pass by, and as we await the BOE’s MPC meeting on November 3rd and Kwarteng’s budget on November 23rd, it will also be critical to track the strength of the USD, which, amidst the deteriorating global economic outlook, has consolidated its reputation as a ‘safe haven’ asset (largest reserve currency in the world) and attracting investors back. In regard to Mauritius, even though the country is less dependent on or exposed to the pound (imports from, and exports to, the UK representing only 1% and 9% of the total respectively in the ‘normal year’ 2019), the danger could come from a strengthened US dollar, not from a weakened pound. As goes the saying, ‘the pound’s weakness is a dollar-strength story.’

Publicité

Publicité

Les plus récents